US spending and inflation numbers boost the case for another rate hike

The US economy continues to confound the doubters, with strong spending keeping inflation far too high. The Fed hawks will increasingly move into the ascendancy, and if the debt ceiling drama is resolved favourably and next Friday's jobs numbers are hot, we have to accept a June interest rate hike would look more likely than not

Income, spending and inflation remain too strong for the Fed to ignore

The April US personal income and spending report is a fair bit stronger than expected across the board, which will fuel talk of another Federal Reserve rate hike at either the June or July meetings. Incomes rose 0.4% month-on-month as expected, with wages and salaries up by 0.5%MoM, but spending rose by 0.8%MoM versus the 0.5% consensus with March revised higher. Consequently, we find real consumer spending came in at 0.5%MoM versus the 0.3% expected. This will inevitably lead to upward revisions of second-quarter GDP expectations given consumer spending is two-thirds of economic activity as measured by GDP.

We then turn to inflation, and the core PCE deflator has come in at 0.4%/4.7% rather than the 0.3%/4.6% expected. This move higher will inevitably boost the case of the Fed hawks such as James Bullard and Neel Kashkari that policy needs to move tighter to ensure inflation returns to the 2% target in a timely manner. We still think it will slow sharply in the second half of the year, but we are increasingly doubtful the Fed will have the patience to hold back from hiking, especially if the spending side is holding up as well as it seems. So, if we get a positive conclusion to the debt ceiling drama and next Friday's jobs number comes in at around 200k, we would have to say the odds will favour a 25bp hike in June.

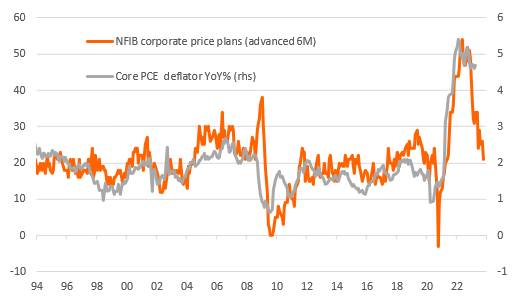

Weakening pricing power points to sharp inflation falls later in the year

But a turn is coming that will result in an eventual major reversal in Fed policy

The chart above shows how the rapid weakening of corporate pricing power (led by plummeting business sentiment) indicates we should expect inflation to slow sharply in the second half of the year – the problem is we aren't confident that the Fed will wait for it to happen. We fear that the likely result is we get over-tightening of monetary policy that, in combination with significantly tougher lending standards that will restrict the flow of credit, will tip the economy into what could be a painful recession. Our conclusion, therefore, is that this leads to an even greater interest rate cut story further down the line.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article