US Presidential election G10 FX scorecard

Our US election G10 FX scorecard is here to gauge the impact of various election scenarios on G10 FX. In our view, the 'Blue Wave' scenario would lead to weaker USD and outperformance of NOK and AUD. We're also giving you an augmented scorecard for those wishing to penalise European FX due to the Covid situation in the region

To gauge the impact of the US presidential elections on G10 FX immediately after the event, we have built a G10 FX scorecard, as you can see below. It consists of three factors:

- Currencies sensitivity to risk;

- The shape of the UST yield curve (2s10s); and

- The level of the short-term mis-valuation (based on our short-term financial fair value model).

In our view, these factors should be the key drivers of FX markets post US elections.

US Election G10 FX scorecard

Blue Wave

In the case of the most positive outcome for markets, the 'Blue Wave', the expectations of larger US fiscal stimulus delivered by the Democrats and the return to the rules-based system for international relations should be initially positive for global risk appetite and lead to a steeper UST yield curve. Hence, the focus on the correlation of G10 FX with global stock markets (MSCI World Index) and UST 2s10s – and the currencies that will benefit. Here NOK, AUD, NZD and CAD all stand out.

The third factor, the mis-valuation, shows to what extent the G10 currencies currently trade out of sync with their short-term fundamentals. This factor captures the scope for a justified correction based on fundamentals – ie, those higher beta currencies that are undervalued have more scope to rally vs those which are rich in the case of a market positive outcome. Here, both NOK and AUD stand out (we show the level of G10 FX short-term mis-valuation in the chart below) and score better than NZD, CAD or SEK.

G10 FX short-term mis-valuations

As the scorecard shows, higher beta, undervalued NOK and AUD should benefit the most from the Blue wave outcome, while USD and the safe-haven JPY should turn into the underperformers.

Biden wins, but Republicans retain the senate

A Biden victory, with Republicans retaining the Senate, would likely manifest itself into a weaker USD (largely due to the expectations of less unpredictable US international policies and the lower possibility of further trade wars) yet the reduced odds of a larger fiscal stimulus would be less positive for global risk sentiment and would reduce the extent to which the UST curve can steepen. Hence, the lower degree of outperformance of the likes of NOK and AUD vs the Blue wave scenario. But still, the conclusions from the G10 FX scorecard would hold, in terms of differentiation. USD would be the laggard and cyclical currencies would benefit.

Trump wins

A President Trump win would catch markets off-guard and likely put an end to expectations of USD weakness in 2021. The rebound in USD would be felt across the entire G10 FX segment, would see the reverse of the price action expected in the case of a Biden victory with activity currencies suffering from the extension of protectionism. The under-priced risk of the return of the trade war agenda for another four years would unlikely lead, at least initially, to materially higher global equity markets. The dollar would benefit, though with the Fed now targeting average inflation (and thus its stance should be skewed to the behind-the-curve approach) this should provide less support to USD than was the case during the first Trump mandate.

Contested result

The price action should be similar in terms of the direction to a Trump victory as it would likely disappoint current market expectations, though the hit to cyclical currencies would likely be larger given the dent to risk appetite. Any prolonged uncertainty about the US Presidential election outcome would be negative for risk assets, lead to lower equity markets, flatter UST and core global curves and benefit safe havens. JPY and USD would lead in gains, followed by CHF.

What about the Covid 19 situation in Europe?

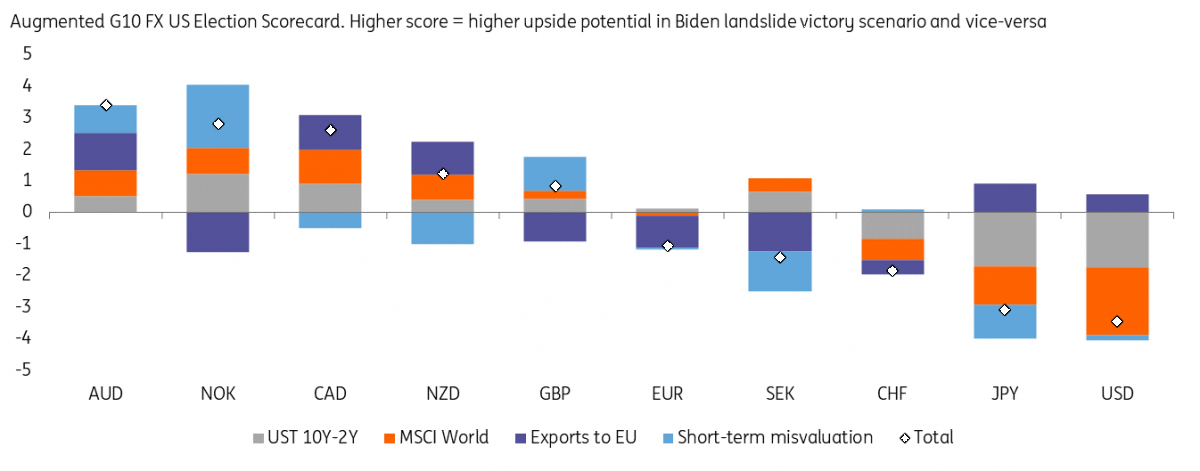

For investors concerned about the further deterioration in the Covid situation in Europe and even more eurozone economic underperformance vs the US and Asia, we also present an augmented version of the scorecard above, which penalises European currencies (given their exposure to the EZ economy – we use the export channel to the EU as % of total exports as the factor to differentiate). As evident in the augmented scorecard below, AUD looks like a better way to express a positive US election outcome market view when compared to NOK – as NOK (as well as other European FX) falls down the pecking order due to its exposure to the European economy.

Augmented US Election G10 FX scorecard

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

29 October 2020

From the ECB to yours: the outlook for banks This bundle contains 7 Articles