US payrolls fails to resolve the 25 or 50bp rate cut call

The US added fewer jobs than expected in August, but there was enough in the report to keep markets guessing on whether the Fed will cut by 25bp or 50bp on 18 September. Lead indicators suggest further weakness lies ahead, and we believe the Fed will go for a 50bp move, but it’s a close call

| 142K |

US Non-farm payrolls, August160K expected |

25bp or 50bp debate remains unresolved

The jobs report provides a real mix of numbers that does little to resolve the debate over whether the Fed will cut rates by 25bp or 50bp on 18 September. We have a 50bp in our forecast, but it is a low conviction call made on the basis that inflation fears have receded and the Fed will want to get ahead of labour market weakness, which we think will become increasingly apparent in the months ahead.

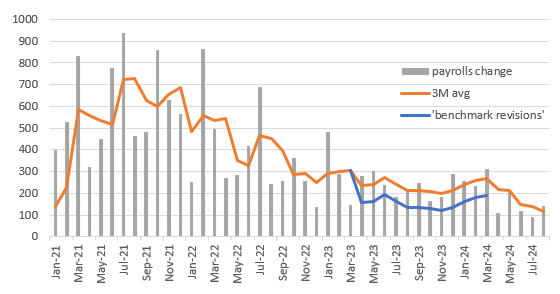

US non-farm payrolls change including provisional downward revision line (000s)

Payrolls continue to soften, but remain positive

In terms of the August numbers, headline non-farm payrolls rose 142k versus the 165k consensus, so a slight downside miss, but there were 86k of downward revisions to the past two months. We are seeing consistent downward revisions to the data now, and that doesn’t even include the provisional benchmark revisions released a few weeks back that showed the BLS overestimated payrolls growth by an average of 78k per month in the 12 months to March 2024. For example, June was initially reported at 206k, to be revised to 179k last month, and now is just 118k, while July was revised down to 89k to 114k.

Given that, can we really trust today’s number? Do we need to knock 78k off the headline figure to take account of the error in the BLS model? - that would give payrolls growth of just 64k.

The unemployment rate has dipped back to 4.2%

On the positive side, we see that the unemployment rate has dipped back to 4.2% after rising from 4.1 to 4.3% last month. Yet the underemployment rate rose to 7.8% from 7.9% so there are a growing number of people that are working part-time, but want to work full time. In this regard, the details show manufacturing looking very weak (-24k). Retail and temporary jobs have fallen for three straight months, and IT jobs have fallen or been flat for five months.

The strength continues to be government (+24k), leisure & hospitality (+46k) and private education and healthcare services (+47k). These are sectors that are typically lowered paid, less secure and more part-time. As such, I would argue that the details are weaker than suggested by the headline; the typical sectors I would associate with a strong, vibrant economy are not performing (business services, manufacturing, transport and logistics, tech, etc).

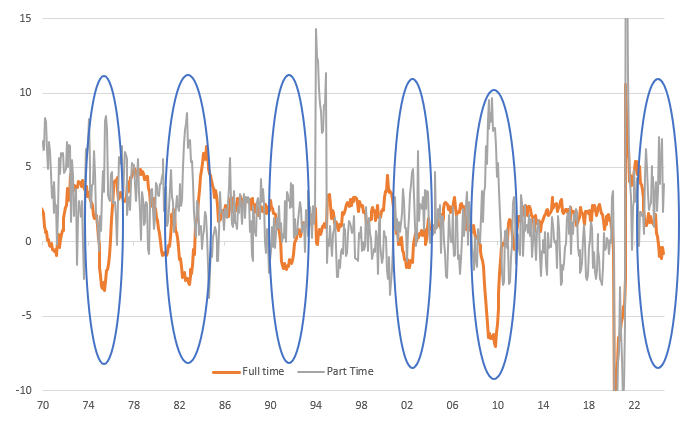

Are we losing the "good jobs"?

Moreover, the chart below does not look good. Full-time versus part-time employment is showing a big divergence, which tallies with the idea that the US is adding largely lower-paid, part-time jobs and is losing full-time, well-paid jobs, primarily through attrition - not replacing retiring or quitting workers. Every recession starts this way, unfortunately. The easiest way to cut costs is not to replace workers, but if everyone is doing that, then the economy slows, and companies start making actual cuts down the line.

Full time versus part time employment YoY%

With job weakness set to intensify we still hold onto a 50bp cut view

In terms of the Fed decision, today’s readings on balance suggest a 25bp cut looks marginally more likely than 50bp (50bp is our forecast), meaning there's no real urgency to go hard early. Still, the jobs market is always the last thing to turn in a cycle, and it is already clearly cooling. Given Fed Chair Powell’s warning that “we don’t seek or welcome further cooling in labor market conditions” there is a strong argument for getting out ahead of potential weakness and opting for 50bp.

He will certainly propose it but is likely to get some pushback from some regional presidents. I strongly suspect this won't be a unanimous decision – something we haven’t seen for a long time. The next stop is CPI, which, of course, could completely blow this out of the water should we get an upside surprise of 0.3%MoM on core inflation… the job of an economist is never dull.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article