US: The Fed looks set to pivot on inflation

- 10 June 2021

- United States

The US recovery is powering on, but there are worries that the supply capacity of the economy isn't keeping pace. We think the Federal Reserve will soon switch position and acknowledge that inflation may not be as transitory as first thought, paving the way for the first steps towards policy “normalisation” later in the year

Back in the green with 7% growth

The US activity story remains incredibly positive with the economy on course to have recovered all pandemic-related lost output in the current quarter – well ahead of all other major developed market economies. Even more remarkably, we believe that with so much stimulus still in the system (both fiscal and monetary), economic output will end the year higher than would have been the case had the pandemic not happened and the economy merely continued along its 2014-19 trend path.

The US economy is on track to end the year larger than if there were no pandemic

Growing nervousness

However, there is growing nervousness that the supply-side capacity of the economy has been scarred by the pandemic and may not be able to fully meet demand. Businesses have gone bust, millions of people remain out of work while lingering Covid containment measures are leading to production bottlenecks around the world. Supply capacity should eventually catch up, but this could take time with the risk that we see more elevated inflation readings for longer than we have experienced at any point in the past 20 years.

The desperate search for workers

The labour market is also experiencing supply and demand imbalances. Non-farm payrolls growth disappointed for the second month in a row despite firms looking to take advantage of the strong consumer demand environment by hiring and expanding. Instead, businesses are faced with a real battle to recruit staff as highlighted by the National Federation of Independent Businesses, which recently reported that 48% of businesses had job openings they have been unable to fill. This is the fourth new all-time high in as many months – and this survey goes back to 1975!

Four factors explain the lack of supply

This lack of supply is down to four factors. Firstly, many pupils are still remote learning so parents have to stay home too. Secondly, some workers are still nervous about returning given the pandemic is ongoing while, thirdly, some older workers who lost their jobs may have chosen to subsequently take early retirement and leave the workforce. Finally, there is the effect of extended and uprated unemployment benefits that may have diminished the attractiveness of seeking work in lower-paid sectors.

These strains should gradually ease in the coming months, but we think there is a window of three to four months where businesses will continue to struggle to find suitable staff.

Competition is heating up - Proportion of workers 'quitting' their jobs to move to a new employer

Therefore, if businesses want extra staff they are having to offer more attractive pay. The retaining of experienced and talented staff is just as crucial, with the quit rate, the proportion of workers leaving their current job to move to a new one, hitting a new all-time high last month. Employment costs grew at the fastest rate for 15 years in the first quarter and we will almost certainly see an acceleration in the second and into the third quarter.

Corporate pricing power is back

Rising wage costs, commodity costs, supply chain frictions and higher freight charges mean that businesses are feeling the financial strain. That said, there is more and more evidence that firms are able to pass higher costs onto their customers given the strong demand environment. This was reflected in both the latest Federal Reserve Beige Book and the Philadelphia Fed manufacturing index. Meanwhile, the NFIB survey showed a net 40% of small businesses plan to raise their selling prices in the next three months – the highest proportion since 1980.

In the service sector, people are desperate to experience things that they haven’t done for many, many months, such as travel, go to restaurants, see a sporting event, socialise in a pub. The strong desire to do these things means that companies faced with higher costs in the service sector are also in a strong position to pass the costs on through higher prices, particularly with so many restaurants, bars and entertainment venues having closed permanently.

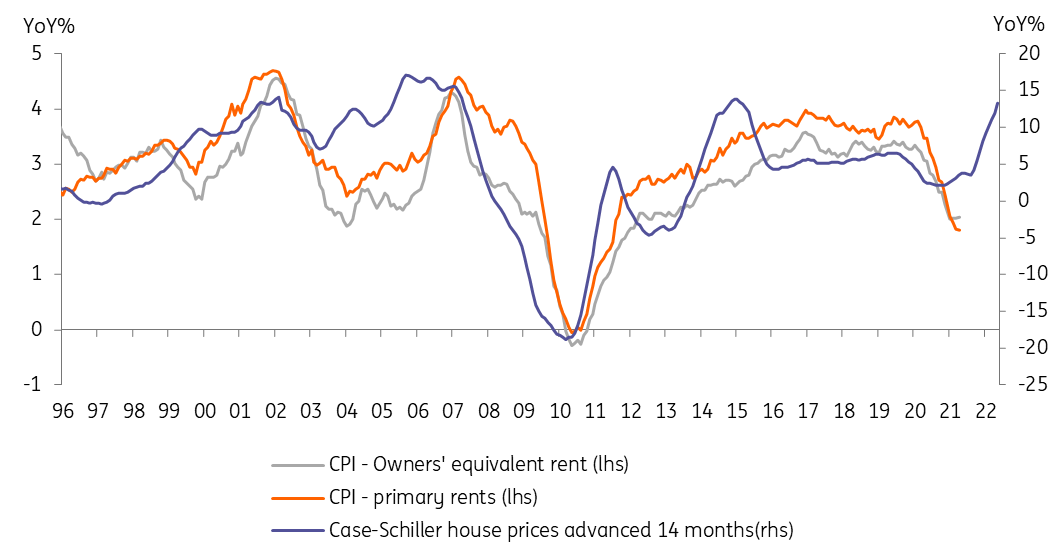

Inflation - higher for longer

Rising housing costs will be yet another factor that keeps inflation higher for longer. They account for around a third of the inflation basket with the chart below being suggesting it will keep headline inflation above 3% for the next 12 months in a lagged response to surging property prices.

Housing costs set to keep inflation elevated

Moreover, an oft-repeated argument from the Fed as to why inflation is likely to be “transitory” is that inflation expectations are “well-anchored”. However, even here we are seeing both market-based measures of inflation expectations and surveys of consumer price inflation expectations moving higher.

So, after a decade of inflation largely undershooting the Federal Reserve’s target we believe the ingredients are all here for a period where inflation pressures are more sustained.

A shift is coming

The Federal Reserve has already pre-empted this to some extent by moving to an average inflation target and indicating that it is prepared to let the economy run hotter than it would have done in the past before raising interest rates. It has also emphasised a shift in its priorities towards making sure more people in society feel the benefits of the recovery through jobs and income growth versus a focus on price stability that has always dominated in the past.

Nonetheless, we are already hearing some Fed officials sounding a little less relaxed about the situation with several suggesting that it may soon be time to start talking about tapering quantitative easing.

A couple more months of strong growth and inflation data plus ongoing job gains and evidence of wages picking up will, we suspect, prompt a change in language at the Federal Reserve Jackson Hole symposium in late August. A more formal warning of QE tapering is possible at the September FOMC meeting, with a slowing in the rate of actual asset purchases expected at the turn of the year. We continue to see the first actual interest rate rise coming in early 2023.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly Update: Looking for freedom

- This bundle contains 14 Articles