US: Look on the bright side

Despite the current market doom and gloom there are plenty of positives for the US economy

Greater headwinds for growth in 2019

2018 was a good year for the US economy, but the situation will undoubtedly get tougher in 2019. We have written at length about the intensifying headwinds – namely the lagged effects of higher borrowing costs, the stronger dollar, the fading support from the 2018 fiscal stimulus and weaker external demand at a time of rising trade protectionism.

Some of these factors can already be seen in the data. With 30-year fixed rate mortgage costs rising above 5%, mortgage applications are falling and slowing the housing market. Business surveys have also softened of late, as concerns about rising trade protectionism and what it might mean for costs and supply chains mount. We have consequently seen a moderation in investment spending on equipment, despite the fact that President Trump’s corporation tax cuts were supposedly introduced to stimulate domestic capital expenditure.

We believe the current market doom and gloom has been overplayed

Financial markets have been deeply troubled by these developments, with the S&P500 falling nearly 20% peak-to-trough since October. President Trump’s open criticism of Federal Reserve policy decisions and the current partial government shutdown, caused by an impasse over the proposed $5 billion security wall along the border with Mexico, is adding to the unease and could take a couple of tenths of a percentage point off 1Q GDP growth. It has resulted in billions of dollars being wiped off the value of investment and pension funds and has seen consumer confidence come under pressure.

As such, it should be no surprise that we doubt the economy will grow as fast as it did in 2018. However, we believe the current market doom and gloom over the US’s prospects has been overplayed and market expectations that the Federal Reserve will possibly cut interest rates this year are wide of the mark.

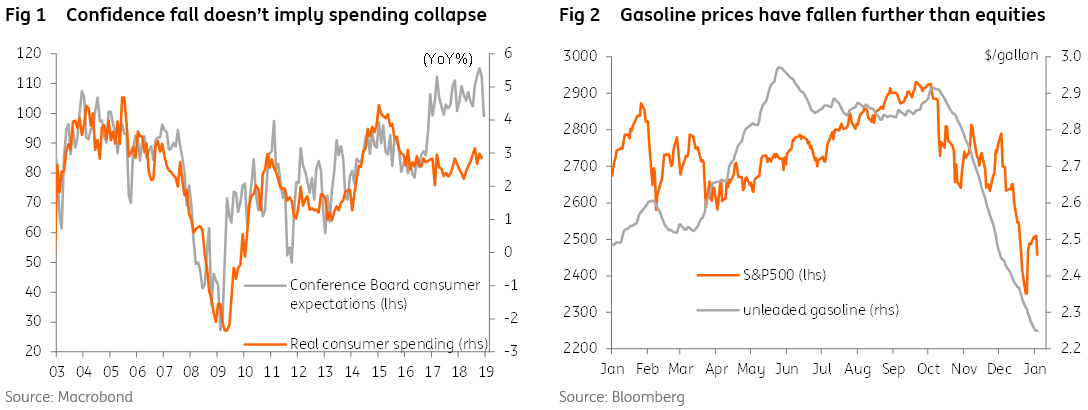

For starters, the fact that consumer confidence has only dropped back to the levels seen in the summer when equities were still riding high, underlines the fact that there are still clear positives for the household sector elsewhere in the economy.

Tight jobs market, faster wage growth and lower gasoline prices could help growth

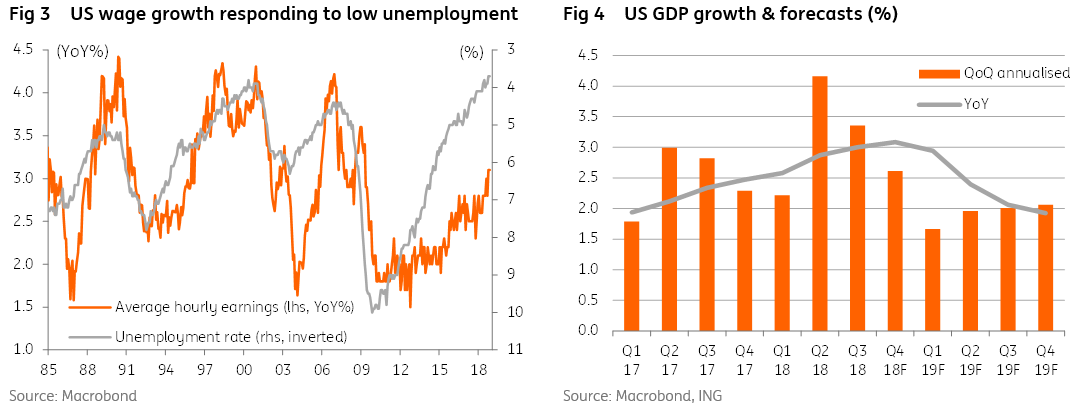

Indeed, the jobs market remains hot with demand for workers outstripping supply. The National Federation of Independent Businesses reported this week that the proportion of firms that can’t fill their current vacancies is at all-time highs (39%). This analysis was backed by the most recent Federal Reserve Beige Book, which suggested that “over half of the Districts cited firms for which employment, production, and sometimes capacity expansion had been constrained by an inability to attract and retain qualified workers”.

This means wages are being bid up and employees are feeling the benefits. Wage growth is now above 3% year-on-year, and we think it will rise further, given the competition for suitable workers at a time when the unemployment rate is at a 49-year low. The Beige Book stated that “in addition to raising wages, most Districts noted examples of firms enhancing nonwage benefits, including health benefits, profit-sharing, bonuses, and paid vacation days.”

We think the growth slowdown will be fairly modest, especially when considering that 2018 saw the fastest US growth for 13 years

We also have to remember that gasoline prices have been plunging at an even faster rate than equities – down 65 cents/gallon since October – leaving more cash in drivers’ wallets (close to $90 billion based on annual consumption). At the same time, house prices continue to rise despite the slowdown in demand for mortgages, so the household balance sheet remains in decent shape overall.

As for the corporate side, while business surveys have come off their highs, they remain at levels consistent with healthy growth rates. The current US-China trade ceasefire until March also provides some breathing room and if progress can be made (such as at the Jan7-8 US-China summit in Beijing) eventually resulting in some form of resolution, or at least an extension of the peace, this would clearly be positive for the economic outlook in the first half of the year. However, we certainly aren’t complacent on this issue and believe tensions will likely intensify before meaningful concessions are made and a longer-term truce is called.

Taking all these factors together we think the growth slowdown will be fairly modest, especially when considering that 2018 saw the fastest US growth for 13 years. We see the economy expanding around 2.3% in 2019 versus 2.9% in 2018 although the quarterly profile sees annualised growth rates running roughly two-thirds those seen in 2018.

Two hikes in 2019 now our base case

As for price pressures, the plunge in the oil price means headline inflation rates are looking less threatening for 2019. Further gasoline price falls are likely in the coming weeks, while airfare and transportation costs, in general, should move lower. The delay to the introduction of additional tariffs on Chinese imports also supports a lower forecast profile for inflation in the near term. However, given the lack of spare capacity in the US economy, we see core inflation continuing to rise through the first half of 2019.

Rising wages will be a major driver of this and therefore a key factor that will keep the Federal Reserve on course to raise interest rates further in 2019. However, we are likely to see a slower and more modest set of hikes versus 2018, as indicated by the more dovish narrative at the December FOMC meeting and the Fed’s acknowledgement that “financial developments” could weigh on the outlook. Having signalled back in September that three rate hikes in 2019 was the most likely scenario, five FOMC members lowered their projection in December, leaving the median forecast at just two 25 basis point moves in 2019.

We still look for tighter monetary policy over the summer

We also have to remember that the Federal Reserve is shrinking its balance sheet while there is growing talk – most notably from Lael Brainard – concerning raising the countercyclical buffers as a way of shoring up the financial system while also tightening monetary conditions. Consequently, we, like the Federal Reserve, see two hikes as being the most likely scenario for 2019 versus the four hikes experienced in 2018.

In terms of our profile for Federal Reserve interest rate hikes we now expect to see a pause in 1Q19, but in an environment of rising wage and core inflation pressure we still look for tighter monetary policy over the summer. Given financial markets are not anticipating any rate hikes this year, there is some scope for re-pricing in the Treasury market, particularly if equity markets can recover some of their losses over the early part of 2019. Add in the fact that US government borrowing continues to rise at the same time as the Federal Reserve is running down its balance sheet, we see the 10-year yield pushing back up to 3% in coming months.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

4 January 2019

January Economic Update: Overdoing the gloom This bundle contains 8 Articles