US jobs report suggests no pressing need for the Fed to cut rates

Solid employment gains, low unemployment and sticky wages suggest no immediate need for Federal Reserve rate cuts. Nonetheless, the jobs market is cooling and the concentration of employment gains in sectors viewed historically as being lower paid and more part-time raises some concerns. We think the Fed will wait until May before cutting rates

| 216,000 |

Number of US jobs added in December 2023 |

Solid job gains dampen talk of imminent rate cuts

Headline numbers are strong from the December US jobs report with non-farm payrolls up 216k versus 175k consensus while private payrolls increased 164k versus the 130k consensus forecast. The unemployment rate held at 3.7% rather than rising back to 3.8% as predicted while wages are hotter than forecast, rising 0.4% month-on-month/4.1% year-on-year versus 0.3/3.9% consensus. Unsurprisingly, Treasury yields and the dollar are on the rise as this report clearly helps to dampen talk of a potential March rate cut from the Federal Reserve.

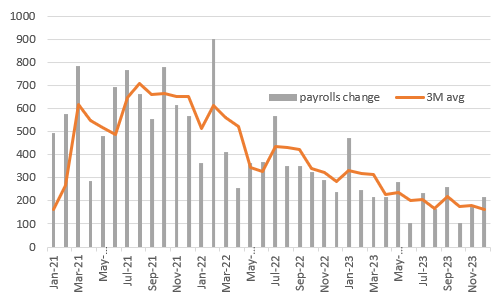

US non-farm payrolls monthly change (000s)

Nonetheless, not everything is rosy. The past two months of payrolls data has been revised lower by 71k and the 3-month moving average continues to moderate, as the chart above shows, to the lowest rate since January 2021. The average work week dropped to 34.3 hours from 34.4, while the participation rate declined to 62.5% from 62.8%. In fact, household employment fell 683k so the reason we saw the unemployment rate hold at 3.7% was down to the labour force falling similarly.

Not everything is rosy in the jobs market

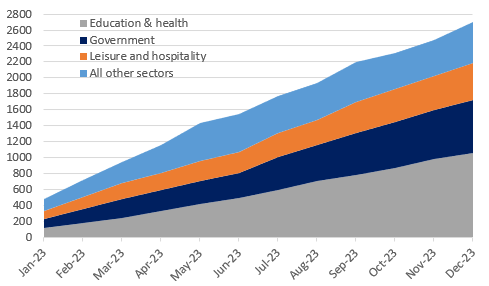

Once again job growth is concentrated in just three sectors – Government (+52k), education/healthcare (+74k) and leisure & hospitality (+40k) – so 77% of the jobs added in December were from sectors that are not at the forefront of what traditionally would be viewed as the growth engines of America – business services, transportation, logistics, technology, construction, etc. Looking at 2023 as a whole, of the 2.7mn jobs created 81.2% were in those three sectors.

Cumulative monthly payrolls increases in 2023 by sector (000s)

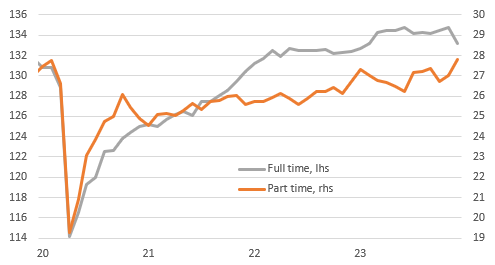

Historically government, education/healthcare and leisure & hospitality tend to be lower paid sectors and more part time in nature and indeed we have seen a huge jump in part-time employment, with a significant drop in full-time employment. It is a volatile series, but effectively the report is telling us that we have the fewest Americans employed full time for 11 months – see chart below.

Part-time employment levels versus full-time employment (millions)

We favour the Fed waiting until May before cutting interest rates

Despite this, the combination of low unemployment, sticky wages and ongoing job creation shows the jobs market remains tight. While we have predicted 150bp of rate cuts for a while for 2024, we didn't, and still don't, buy into the March start point priced by markets earlier this week. We still think May is the more likely start point. Next week's inflation report will still have core inflation close to 4% so the Fed is under no immediate pressure to act.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article