US jobs report hints at a gradual cooling despite a strong headline

US nonfarm payrolls rose 275k in February, but big downward revisions, weak wages and rising unemployment suggest things are not quite as robust as the headline indicates. Moreover, lead indicators are clearly weakening and a slowdown looks to be on the way. It's not enough for the Fed to relax just yet, but we think things will be in place for a June rate cut

| 275,000 |

February increase in nonfarm payrolls |

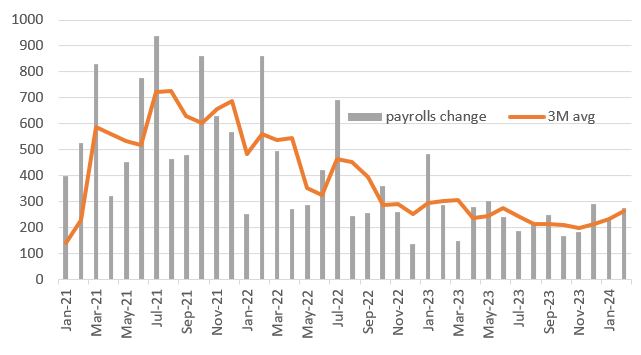

Big jobs number, but big downward revisions too

The US jobs report always throws up surprises and we have quite a lot in this report for February. Nonfarm payrolls rose 275k, above the 200k forecast, but there were 167k of downward revisions to the past two months so the net improvement was little more than 100k. The revisions recently have been huge – remember last month we got 126k of upward revisions. This highlights how unreliable the data collection is and why we should really focus on a range of labour market indicators rather than this single payrolls number alone.

In terms of where the jobs were created, it was yet again concentrated in government (52k), leisure & hospitality (58k) and private education & healthcare (85k) - not industries you would typically associate with a strong vibrant US economy. Indeed tech (2k), professional business services (9k), retail (19k), construction (23k) and manufacturing (-4k) remain pretty subdued.

Nonetheless, this is still better than the other labour data we have had this week. The ISM employment indices are both in contraction territory, indicating job shedding, while the ADP private payrolls series has been in a 104-158,000 range for the past seven months. Then both the JOLTS report and the Challenger lay-off series indicate that hiring rates are lackluster while layoffs are rising, albeit from low levels. Rounding out the numbers we had the National Federation for Independent Businesses report yesterday that the proportion of small businesses looking to hire new workers fell to just 12%, the lowest reading since May 2020 when pandemic controls were so strict. Given this backdrop, we have to expect payrolls to slow more meaningfully in the next few months

Change in US nonfarm payrolls (000s)

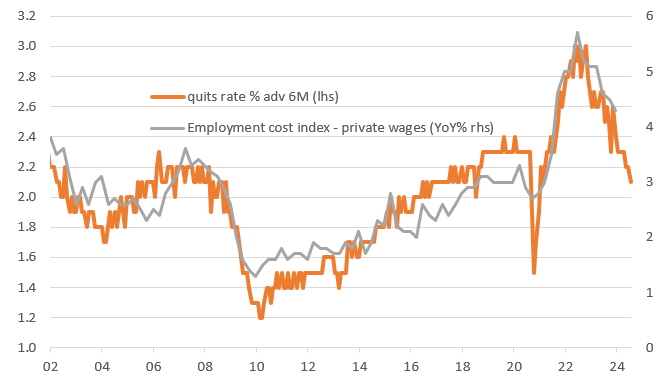

Rising unemployment and weak wages could be a spreading theme

The household survey, used to calculate the unemployment rate, suggested employment actually fell 184k while the labour force increased 150k, hence the rise in unemployment to 3.9% from 3.7%. Meanwhile, average hourly earnings slowed to just 0.1% month-on-month from a downwardly revised 0.5%, but this more reflects a swing in the number of hours worked than anything dramatic in terms of pay. More significantly, the rapid slowing in the quit rate, suggests that while there are lots of vacancies out there, they aren't particularly attractive and fewer and fewer people are interested in taking them. This has a knock-on effect in that if there is less labour market churn there is less need for an employer to pay up to retain staff and suggests inflation pressures emanating from the jobs market will continue to ease.

Falling quit rate suggests weakening pay pressures

Too soon for a rate cut, but June is on the table

So on balance, we would have to say this is a weaker report than was expected, but not weak enough to change the Fed's mindset that there is no need to do anything imminently. Moreover, next week's core CPI is expected to remain too hot for comfort, suggesting little prospect of any policy change at the March or the May FOMC meetings. Nonetheless, with more cooling in the jobs market looking probable we continue to see a strong chance of a June cut with the Fed indicating a desire to gradually move policy back to more neutral levels later in the year. Note that this is now fully priced by markets.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article