US jobs report better than feared

A respectable outcome for January job creation with fewer than feared downward revisions to historical data have cemented expectations that the Fed will not be cutting rates imminently. There are still lingering concerns about the quality of jobs being added, but an improving trend in jobs creation since late summer means the Fed will hold rates until 3Q

| 143,000 |

US jobs added in January |

| Lower than expected | |

Downward revisions, but with stronger near-term momentum

There is a lot to unpack in today’s US jobs report. January non-farm payrolls came in at 143k, below the 175k consensus, but there were 100k of upward revisions to the past two months and the unemployment rate came in at 4% versus 4.1% previously and expected. Average hourly earning rose 0.5% month-on-month, but the average working week dropped to 34.1 hours – matching the lows of the pandemic period. That in itself looks a pretty solid report and would justify the Federal Reserve holding rates steady for now.

We also get a whole load of revisions – the payrolls series is being adjusted for updates to the births-deaths model and changes to seasonal adjustment factors, while the unemployment rate is adjusted to take account of new population estimates, although changes were small.

With regards to the non-farm payrolls, the benchmark revisions were not as severe as initially proposed. The provisional estimate from August was for 818k of downward revisions over the 12 months to March 2024, but this is now reported as 598,000. Revisions to subsequent data mean that for 2024 as a whole the average monthly payrolls gain is now 166,000 versus 186,000 previously reported. More significantly October, November and December jobs have been revised higher, so we have a stronger trend at the end of 2024 than previously thought. As such it doesn't support the case for any near-term Fed easing.

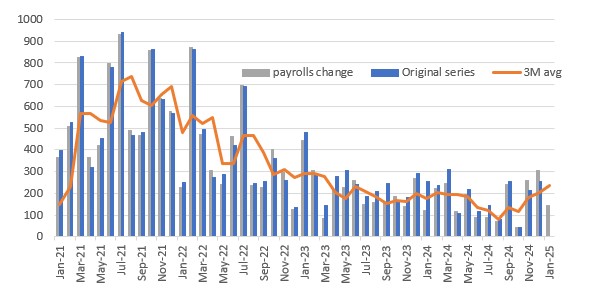

Monthly change in non-farm payrolls (000s)

This chart above the revisions. The blue bays were the original monthly change in non-farm payrolls and the grey bars are the new published series. The orange line is the new 3M moving average and you can clearly see the improvement over the latter part of 2024.

Job quality remains an issue

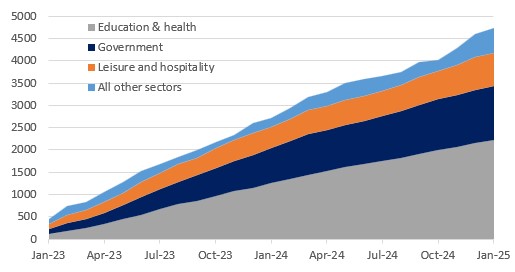

Once again we come to the issue of the quality of the jobs being added. Originally we had 78% of all jobs created in the US since December 2022 were in the three sectors of government, leisure & hospitality and private education & healthcare services. The revisions show it is now 88%! We believe those three sectors tend to be lower paid, less secure and more part-time. This also helps to explain the drop in the average working week to just 34.1 hours. Note that previously 5.2mn jobs had been added between December 2022 and December 2024. Now it is 4.7mn between December 2022 and January 2023.

Contribution to cumulative jobs gains since December 2022 (000s)

Solid jobs market and sticky inflation to keep the Fed on hold until the third quarter

Looking at the overall picture we see the downward revisions were not as deep as thought while the trend over recent months has been stronger non-farm payrolls growth than expected. With the unemployment rate at just 4% and with next week's core CPI MoM reading expected to come in at 0.3% MoM the Fed is very likely to be on hold for several more months – remember we need to be tracking at 0.17% MoM to deliver 2% year-on-year inflation. We remain cautious on the composition of jobs. We’d be much happier if it was tech, construction, business services, transport & logistics, manufacturing – the traditional growth engines of the US economy – that were driving employment growth, but we can’t have everything. Nonetheless, we think the Fed will be on hold until the third quarter of the year.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article