US inflation relief, but an extended Fed pause still looks likely

After four consecutive 0.3% MoM prints, December's core inflation figure posted an improved 0.2% outcome. Nonetheless, the trend remains too hot for comfort and the Fed is likely to extend its well telegraphed pause in rate cuts beyond March. The run-up in Treasury yields and the stronger dollar will provide headwinds to growth and we still look for three 25bp rate cuts in 2025

Core inflation undershoots expectations

US consumer price inflation has come in at 0.4% month-on-month/ 2.9% year-on-year for headline and at 0.2%/3.2% for the core (ex food and energy). The headline was in line with expectations, but the core rate was a touch better than the 0.3% MoM rate anticipated – the core rate, it turns out, was 0.225% to 3 decimal places.

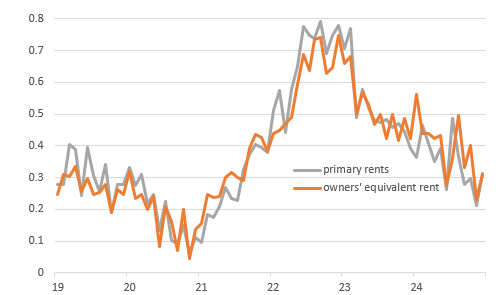

The details show food prices rising 0.3% MoM, which we had thought would be higher given egg and vegetable price moves in PPI in recent month, with energy prices rising 2.6% MoM. In terms of the core rate, vehicle prices were hot with new vehicles experiencing price increases of 0.5% MoM while used vehicle prices rose 1.2% MoM. Airline fares were also up strongly, as flagged in yesterday’s PPI report. However, offsetting this were some cooler medical care-related cost increases (0.2% MoM rather than the 0.4% run rate of recent months) while the all important housing rent components came in at 0.3% MoM, which is more in line with long run trends and suggests ongoing normalisation. This is a big story given their high weights within the CPI basket. Hotel fares were also a lot more subdued than we thought.

MoM changes in housing costs are converging on pre-pandemic norms

Three rate cuts in 2025 remains our call, but they may come later

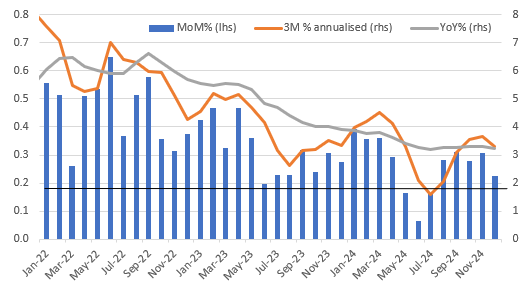

Market Federal Reserve interest rate cut expectations have moved modestly dovishly on this, pricing around 40bp of cuts this year, but 10Y Treasury yields are 10bp lower. We have been predicting three 25bp rate cuts for the year and are sticking to that view for now. However, it may be that rather than cutting in March as we had been suggesting the first move for 2025 is more likely to happen in June looking at the data right now. The chart below is core CPI under different metrics. Focus on the blue bars, which are the MoM. We need to see them averaging 0.17% MoM (the black line) in order to be confident the annual rate of core inflation is on the path to the 2% target. We are still running too hot for comfort – hence the likelihood the Fed pause is extended well beyond January unless we rapidly see those blue bars coming in below the black line.

US core inflation MoM%, 3M% annualised and YoY%

Nonetheless, the near 10% jump in the trade-weighted dollar since September and the surge in Treasury yields (still up more than 100bp since September despite today’s moves) will be headwinds to growth – note mortgage rates are back above 7% and credit card borrowing costs remain close to all-time highs – and will help to dampen inflation pressures too. This should give the Fed greater scope to respond with lower rates in the second half of 2025.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article