US inflation relief and consumer cooldown boosts chances of rate cuts

The Federal Reserve’s favoured measure of inflation came in at just 0.1% MoM, offering hope that the first quarter “hot” prints are firmly in the rear-view mirror. US consumer spending is also slowing with first quarter growth set to come in at less than half the rate recorded in second half 2023. This combination boosts the chances of Fed easing policy

| 0.1% |

MoM increase in core inflation |

Inflation relief with a "low" 0.1%

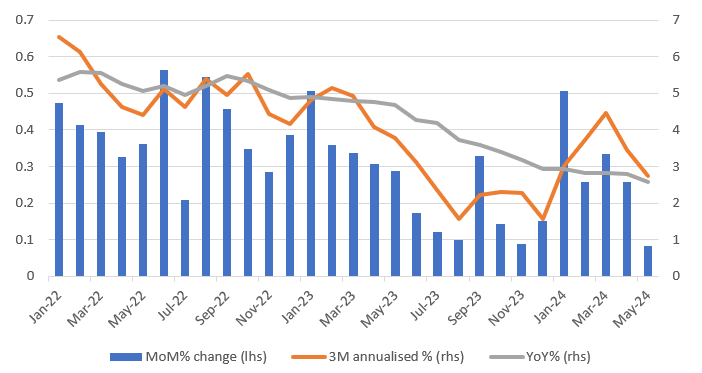

The May personal income and spending report has offered some encouragement that inflation pressures are easing once again after coming in far too hot in the first three months of the year. The core personal consumer expenditure deflator, a broader measure of inflation pressures than CPI that the Fed prefers to focus on, came in at 0.1%MoM/2.6%YoY. This was expected given the read through from components within the CPI and PPI reports, but after plenty of upside surprises this year, it is a relief. The headline measure (including food & energy) was 0.0%MoM/2.6%YoY, as expected.

Looking at the unrounded numbers, the month-on-month change in core inflation was actually a “low” 0.1%, coming in at 0.083% to 3 decimal places although April was revised up marginally to 0.259% from 0.249%, thereby making it a 0.3% MoM rounded, which is a tiny bit disappointing. Overall though, it helps the argument that inflation is looking better behaved, which may well open the door to interest rate cuts later in the year.

Core PCE deflator

Consumer cooldown continues

Household income was stronger than predicted, rising 0.5% MoM in nominal terms with real household disposable income also up 0.5%. Spending also recovered, rising 0.3% MoM in real terms, after April’s 0.1% drop and downward revisions to first quarter numbers. Nonetheless, the trend does appear to be slowing. Consumer spending averaged 3.2% real annualised growth in the second half of 2023, but assuming we get a 0.2% real MoM increase in spending in June, that will mean annualised consumer spending growth of just 1.5% in first half 2024. As such, both inflation and spending suggest tight monetary policy is cooling the economy and constraining price increases.

The Fed doesn’t want to cause an unnecessary downturn – rate cuts from September

The Fed believes monetary policy is restrictive at 5.25-5.50% in an environment where it views the neutral interest rate as being around 2.8%. The Fed doesn’t want to cause a recession if it doesn’t have to and if the data allows it to start making monetary policy slightly less restrictive, we think the Fed will take that opportunity, potentially as soon as September. For officials to be comfortable taking that course of action, we think the Fed need to see three things:

- More evidence of inflation pressures easing. If we can get another couple of 0.2% or below MoM core inflation prints in quick succession that will be a necessary, but not a sufficient factor that leads to a rate cut.

- More evidence of labour market slack. The unemployment rate has gone from 3.4% to 4.0%. If that moves convincingly above 4% with more evidence of a cooling of wages this too will help swing the argument in favour of rate cuts – jobless claims data and weak business hiring surveys suggests the jobs market is softening.

- Softening consumer spending. It has been the primary growth engine in the US, but as stated, the rate of growth has halved between the second half of 2023 and first half of 2024. The Fed needs to see that continue through into the third quarter. Weak real household disposable income growth, the exhaustion of pandemic-era accrued savings for millions of households and rising loan delinquencies suggest financial stress is materialising for many lower-income families, suggests this will indeed continue.

If we get all three of these, we believe the Fed will seek to move monetary policy from “restrictive” to “slightly less restrictive” with 25bp rate cuts at the September, November and December FOMC meetings.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article