US inflation heads higher, when will rates?

Headline inflation is being held down temporarily by energy price falls, but decent growth and a robust labour market suggest price pressures will strengthen. This will help build the case for a summer Federal Reserve rate hike

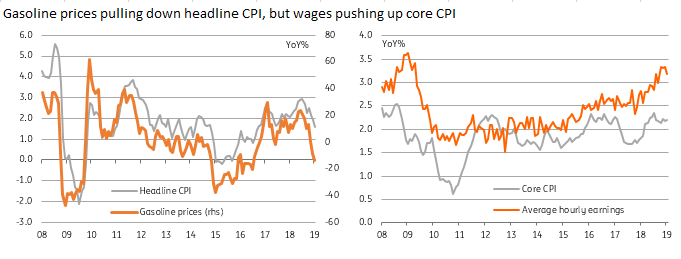

Core price pressures persist

US consumer price inflation for January has come in broadly in line with expectations. Lower fuel prices have helped slow the annual rate of headline inflation to 1.6%, the slowest rate since June 2017, but core (excluding food and energy) inflation has held at 2.2% rather than fall to 2.1% as the market was predicting

Looking at the details, gasoline prices have fallen from $2.92/gallon in early October to a low of $2.30 in January, contributing to a seasonally adjusted 3.1%MoM fall in energy prices in today’s report. These persistent price declines have contributed to sharp falls in airfares and other transportation costs (-1.3%MoM) with further price falls likely over the next couple of months.

Away from energy and transportation the situation looks fairly uniform with medical care, housing, education and food all experiencing a 0.2%MoM increase in prices. Recreation and tobacco saw prices rise 0.3%MoM while apparel, which is admittedly very volatile, rose 1.1%MoM after two or three very soft months.

US inflation measures (YoY%)

Higher inflation to support the case for interest rate hikes

In terms of the outlook, we suspect the US is at, or at least very close to, the bottom for headline inflation. For one thing, we suspect energy will start to make more of an upside contribution in March and April given the price of oil has risen $12/barrel since its mid-December trough.

More significantly, there is a shrinking amount of spare capacity in the economy and this is now clearly feeding through into higher worker pay. Given the US is predominantly a service-based economy these higher wages are adding to business costs and we expect to see more firms passing them onto consumers through higher prices. We, therefore, see headline inflation heading back to 2% in 2H19 with core inflation edging up to 2.5% this summer.

We believe that higher inflation in combination with strong economic fundamentals will convince the Federal Reserve to raise interest rates further. However this view critically depends on positive news from the US-China trade talks and a general de-escalation of the protectionist threat. If that can be achieved then we think we will see a June rate hike. If not then the risks to growth will be heightened and it may be that the Fed funds rate has already peaked.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more