US inflation cools, but tariffs threaten higher prints in coming months

Good news on inflation, but the fact it was overwhelming caused by falling airfares has muted the market reaction. Tariff fears are already seeing companies nudging prices higher and risk higher inflation readings over the summer

Inflation cools, primarily due to lower airfares

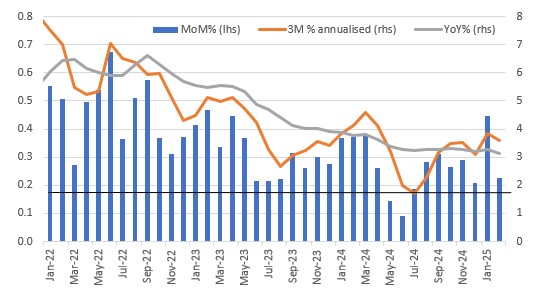

We've had a surprisingly cool set of February US consumer price inflation prints of 0.2% month-on-month for both headline and core versus consensus predictions of 0.3%. This pulls the annual rate of headline inflation down to 2.8% from 3% while core inflation dips to 3.1% from 3.3%. To three decimal places the MoM change in core inflation was 0.227%, which remains above the 0.17% (black line in the chart below) trend that we need to average to bring inflation down to the Fed's 2% year-on-year target, but this is encouraging news for the Federal Reserve.

US core inflation metrics

The details are less rosy though with a substantial 4% MoM drop in air fares the main factor driving the softer inflation readings. New car prices fell 0.1% while gasoline prices fell 1%, but everything else looks to be tracking neutral to hot. Services excluding energy continue to rise 0.3% while apparel increased 0.6% and used vehicles increased 0.9%.

Tariff threat could reinvigorate the inflation threat

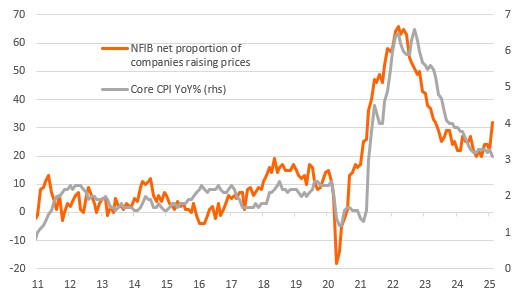

Moreover, we are wary of anecdotal evidence of firms pre-emptively raising prices ahead of potential tariffs – pricing of longer-term contracts have to take account of potential input cost increases right now. The Fed's Beige Book made this point last week, while yesterday's NFIB survey reported a 10 point jump in the proportion of companies raising prices. This chart below suggests the risk that core inflation starts to reverse and move higher again in coming months.

Businesses are increasingly inclined to hike prices on tariff fears

Tariff uncertainty and associated price increases will squeeze spending power and could prompt further weakness in consumer sentiment and spending. They may also mean that the lack of clarity on the trading environment and the threat of reciprocal tariffs weighs on corporate sentiment, holding back on investment and hiring until there is greater clarity – hence the growing talk of potential recession. But for now the economy is growing and is adding jobs and the potential for higher inflation means that we don’t expect the Fed to cut rates again before September.

Housing costs could slow dramatically later in the year

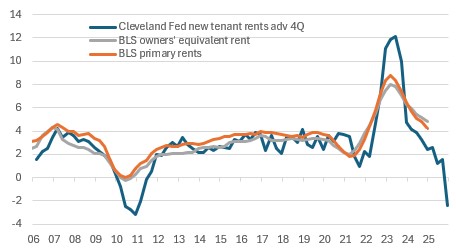

Nonetheless, one thing that we are keeping a close eye on is new tenant rents, which the Cleveland Federal Reserve bank reports are falling quite quickly now. If this translates into much cooler CPI housing measures later in the year, as the chart below suggests, then this can go a long way to mitigating inflation fears relating to tariffs. Remember housing accounts for over 40% of the core inflation basket and if we do indeed see signs of economic weakness this suggests the risks could be skewed towards the potential for more rapid Fed rate cuts at the turn of the year and into early 2026.

New tenant rents point to sharp slowdown in housing costs by year-end

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article