US housing market bounces with a capital “V”

As the debate goes on about the shape of the overall US economic recovery, in the housing market there is little doubt it is a “V”. This has positive consequences more broadly, but there are threats to its durability as key parts of the CARES Act expire and renewed shutdowns make work harder to come by

Covid-19 dealt a massive blow to the housing market

The housing market started the year in great shape thanks to record employment, rising wages and low mortgage rates, but the Covid-19 pandemic soon sent the sector crashing. As the gravity of the situation became apparent, the fear for health and jobs and the turbulence in financial markets saw even seasoned buyers take flight with transactions pulled in significant numbers.

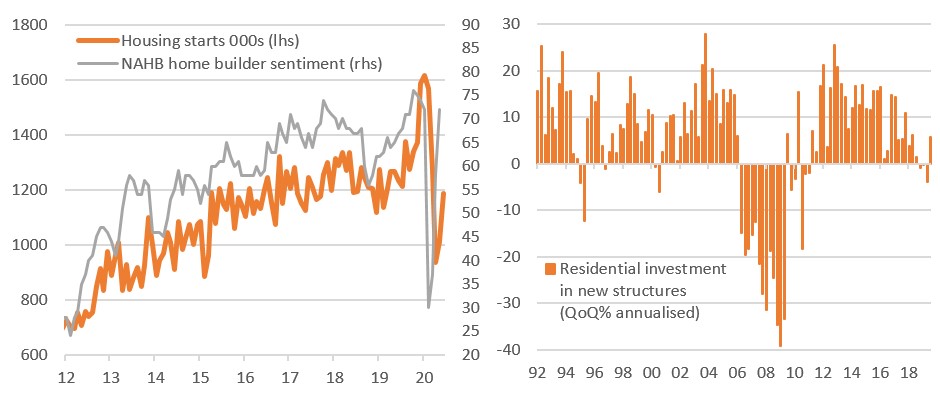

Existing home sales fell 32% between February and May, taking them towards the lows experienced in the global financial crisis while new home sales proved to be only marginally more resilient, falling 25% between January and April. Housing starts – a measure of construction activity – fell 42% between January and April with the construction sector losing 1.1 million jobs through March and April as State Governors shut down building sites.

Fed action has prompted a sharp recovery

However, the news is already turning for the better with lead indicators pointing to a vigorous recovery in housing activity. The Federal Reserve’s aggressive liquidity injections, interest rate cuts and asset purchases have calmed market nerves and kept credit flowing to the extent that mortgage rates are now at historical lows. A resurgent equity market is also a positive through lifting sentiment, particularly for those first-time buyers who kept their deposit invested there.

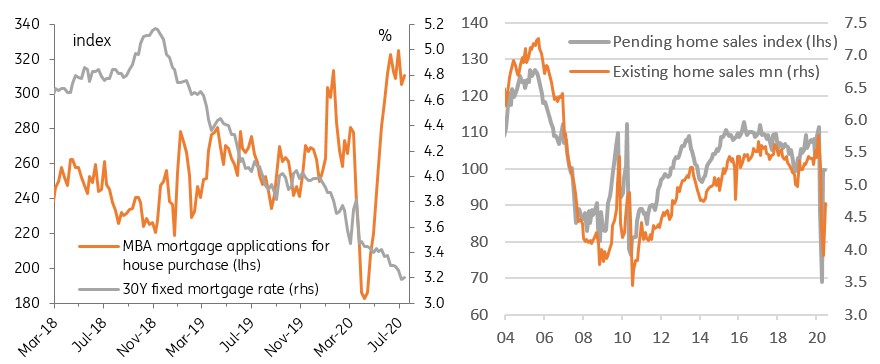

The result has been that mortgage applications for a home purchase surged to an 11-year high, which is remarkable given 32 million people, or nearly 20% of the labour force, are claiming some form of unemployment benefit. Record low mortgage rates have improved affordability while significant pent-up demand following weeks of lockdowns are also leading to a major bounceback.

Mortgage applications and new home sales at multi-year highs!

Another important factor explaining the vigour of the recovery is that the average age for a home buyer is 47, according to the National Association of Realtors. This demographic is less likely to have been impacted by unemployment, will be more financially secure and have a better credit history versus younger members of the population who are more likely to work on lower wages in retail and hospitality. Older home buyers are also more likely to be looking for an investment property or a vacation home.

The surge in mortgage applications already triggered a 44.3% jump in pending home sales in May while new home sales recorded a 19.4% bounce May and an 13.8% gain in June to leave the level at 776,000 – the highest since 2007! Both new home sales and pending home sales are recorded at the point buyers sign the contracts – right at the beginning of the transaction process. Existing home sales are recorded as transactions when contracts are closed, which can take a couple of months and explains why they continued to fall in May. However, they rose in June, with the strength in pending home sales suggesting we should be back up to the 5-5.5mn range next month (see right hand chart above).

Housing to be a major GDP growth driver in 3Q

The recovery on housing demand is also prompting a rapid revival in construction with the National Association of Home Builders sentiment having fully reversed its post-Covid losses. Construction employment has risen by 611,000 in the past two months, while housing starts have risen a cumulative 27% during the same period. Based on the recovery in sentiment further strong gains in jobs and construction are likely over the next couple of months, which will support 3Q GDP growth.

A strong housing market boosts demand elsewhere in the economy. Housing transactions are strongly correlated to retail sales – as people move to a new home they typically spend money on new furniture and home furnishings, garden equipment and building supplies such as a new paint job and a bit of home improvement. It also results in demand for moving services while generating legal and mortgage fees within the service sector, which should also all help boost 3Q GDP.

Construction activity bouncing back after shutdowns

CARES Act expiry and Covid spikes could limit further upside

However, there are some issues brewing for the residential property sector. The reintroduction of containment measures in the wake of a renewed flare up in Covid-19 cases means more business closures and rising joblessness that could threaten the broader economic recovery. While not necessarily directly impacting the home buyer demographic right now it could make potential purchasers more wary. In this regard, the average age of a first-time buyer is 33 and any economic uncertainty and potential fear over employment prospects mean that this first part of a housing market transaction chain remains the weakest link.

Another, potentially more significant issue is that the enhanced unemployment benefit within the CARES Act, providing an extra US$600 per week to 32 million people, and the federal eviction protection, both end this Saturday (25 July). Talks are ongoing about another round of stimulus, but we are likely as a minimum see the US$600/week tapered to something closer to US$200-450 per week with the protracted nature of the discussion possibly meaning a payment pause for a week or two.

In an extreme case this additional payment could disappear completely. Either way incomes will be falling for those 32 million people at a time when job opportunities are increasingly scarce due to renewed Covid lockdowns. This means a growing chance of missed rent or mortgage payments at a time when protection from eviction is ending – note several states such as California and New York have extended their own state legislation, but the majority of others have not. A rising number of mortgage defaults and foreclosures could undermine the recovery in the property market with our base case being a gradual moderation in housing market activity as we approach 4Q20.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

24 July 2020

Covid-19: The world’s slow, uneven recovery This bundle contains 8 Articles