US home sales hit by affordability and supply constraints

US home sales remain subdued thanks to elevated borrowing costs, high prices and a lack of supply. New home sales should continue to outperform existing ones in this environment, but price risks remain skewed to the downside. Commercial real estate woes are the bigger concern as office vacancies and higher refinancing risks point to rising loan losses

Existing home sales remain under pressure from affordability issues and a lack of options

Existing home sales fell 3.4% in April to an annualised 4.28mn versus expectations of a 4.3m outcome. Sales had been as high as 6.3mn as recently as January 2022. Higher borrowing costs and a general lack of affordability after prices rose nearly 50% through the pandemic have constrained demand, but we also have to recognise there is a lack of supply out there, which is also contributing to lower transaction numbers.

The more than doubling of mortgage rates over the past 18 months means many homeowners who would like to move are effectively locked in by the cheap financing they secured on their current property. New home sales have consequently been performing more strongly despite the drop in mortgage applications for home purchases – the buyers that are out there simply don’t have much to choose from.

New home sales are outperforming existing home sales as mortgage applications point to weakening demand

Affordability will remain a key constraint that points to downside risks for transactions. The latest weekly Mortgage Bankers Association data showed that the typical mortgage for a new home taken out last week was a 30Y fixed rate product with a size of $440,400 at a rate of 6.57%, giving a monthly mortgage payment of $2804, a record high. Twelve months ago this was $1750 per month.

Consequently, if you are considering buying a home today, you are looking at an annual mortgage cost of around $33,650 on average which, given a median pre-tax US household income of a little under $75,000, points to ongoing weak demand unless prices fall substantially or borrowing costs plunge.

Higher borrowing costs and elevated prices have led monthly mortgage payments to surge

If unemployment turns then rising supply could mean accelerating price falls

Should the US economy experience a hard landing and the start of a rise in unemployment, this would threaten a rise in default rates and an increase in the supply of homes for sale. In this scenario, falling demand and rising supply mean falling property prices would be the likely outcome. House price-to-income ratios remain extremely elevated, and for them to return to long-run averages, we would likely need to see prices fall by around 20-25% in the absence of any rise in incomes. Construction of new homes would inevitably fall as well.

Commerical real estate is where the bigger problems lie

Unfortunately, it isn’t only the residential sector that looks vulnerable. Last week the Federal Reserve warned of the risks facing the commercial real estate sector since the sharp jump in interest rates over the past 14 months “increases the risk” that commercial real estate loans will be difficult to refinance. A recent report from another bank suggested that up to $1.5bn of these loans need to be refinanced by 2025. With office occupancy nationally running at 45% according to data from Kastle and many offices in need of updating and investment, there is the very real risk that defaults rise – A PIMCO fund has defaulted on $1.7bn of office-related loans this year and Brookfield has defaulted on more than $750mn of debt tied to Los Angeles office blocks.

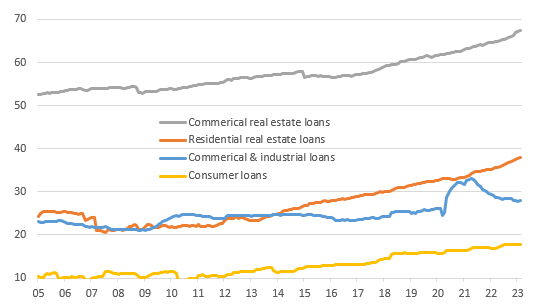

What makes this so problematic for the property market and construction sectors is that small banks account for such a high proportion of commercial bank lending to both residential and commercial property. As the chart below shows, banks with less than $250bn of assets account for two-thirds of the stock of all commercial lending to commercial property and more than a third of residential property lending by all banks.

Small and regional banks account for the majority of commercial real estate lending

Small banks will come under increasing pressure, threatening weaker credit growth throughout the economy

With these small and regional banks already being squeezed by deposit flight and facing the prospect of more intense regulatory oversight in the wake of recent high profile failures, loan losses on commercial real estate will only heighten the pressure on these banks. The Fed’s viewpoint is that “the magnitude of a correction in property values could be sizable and therefore could lead to credit losses by holders of C.R.E. debt.”

With the Fed’s Senior Loan Officer survey indicating credit conditions are rapidly tightening across the board and particularly for commercial real estate lending, this implies a sharp downturn in lending for the sector, meaning refinancing could be immensely challenging and create a downward spiral for prices that will suck construction spending sharply lower.

Tighter lending conditions point to a steep downturn in lending on commercial real estate, making refinancing challenging

This will have knock-on effects for other lending markets, with banks increasingly reluctant to lend across the board. This is hugely significant as what turns struggling businesses into failing businesses is when credit availability evaporates. Given small and regional banks account for more than 40% of all lending in the US, with a particular focus on small businesses outside of major cities, this is a troubling situation. Large banks are unlikely to be able to fill the gap and the risk is that unemployment climbs. In such an environment, the market pricing of significant and rapid interest rate cuts from the Federal Reserve from later in the year appears justified.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article