US: Freezing February will give way to March madness

Virtually all February data has disappointed as winter storms and cold conditions took their toll on supply chains and kept people inside. Today’s durable goods report was no different, but the data will all bounce strongly for March given massive fiscal stimulus and record low customer inventories

Bad weather and supply chain issues weigh temporarily on orders

Like most other February data, the durable goods orders report has undershot expectations by falling 1.1% month-on-month rather than rise 0.5% as consensus forecast. The core non-defense capital goods orders ex aircraft, which has a strong lead quality for determining where business capex is heading, fell 0.8% versus the 0.5% gain anticipated. While not great, we see nothing to worry about.

Bad weather is likely to have been a key factor here with all sectors witnessing declines aside from electrical equipment (+0.2% MoM). If you were experiencing slower production due to storm disruption you obviously need to order less for the next month. ISM orders figures remain very firm so March should rebound strongly on more seasonal weather patterns.

However, there are other issues such as the global semi-conductor shortage, which is impacting vehicle production around the world given they are in anything from brake sensors to satellite navigation to parking assistance systems. If you can’t get enough semi-conductors then you order less of everything else as well, be it steel or tyres – note that vehicle and parts orders fell 8.7% MoM. Assuming this can be resolved soon, orders should also bounce back.

Business surveys point to a strong March rebound

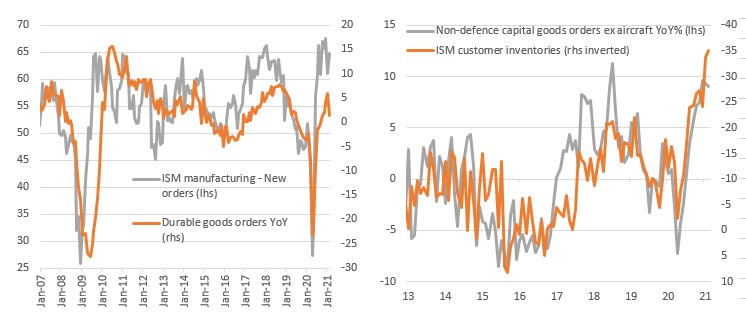

The February ISM report suggest manufacturers remain optimistic and they are seeing strong order flow. Indeed, as the chart below shows ISM new orders are at levels historically consistent with 15% year-on-year growth in durable goods orders. Furthermore, record low inventory levels as reported by the ISM, combined with the prospect of a broadly re-opened, stimulus primed economy in the second quarter, suggest domestic orders will continue to grow strongly this year.

Strong order books and low customer inventories suggest strong growth ahead

The investment outlook is strengthening

Export orders will continue to underperform given new lockdowns in Europe, but assuming we see an easing of restrictions in response to lower hospitalisations and rising vaccination rates we should see improvement in the second half of the year. All of this bodes well for capital expenditure as the chart below shows.

Consequently, while the February figures have disappointed there is nothing to be too concerned by. Consumer spending is expected to rebound strongly in March and April on the latest stimulus payments, manufacturing will roar back given the strong order books and low inventory levels while employment should continue to recover as the economy re-opens and job opportunities improve.

Investment spending to accelerate

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

24 March 2021

Night boat to Cairo This bundle contains 10 Articles