Evolution, not revolution for the Federal Reserve

- 30 January

- United States

The scale of change at the Fed won’t be as dramatic as expected six months ago, with data remaining the prime driver of policy changes. Nonetheless, the new chair, looking set to be former Fed Governor Kevin Warsh, may be more willing to restart quantitative easing should upward pressure on Treasury yields occur

Kevin Warsh set to be named new Fed chair, but will Powell stay on?

The battle between a president who believes the Federal Reserve should be cutting interest rates and an incumbent chair focused on protecting the central bank’s credibility to fulfil its Congressional statutory mandate – maximum employment and price stability – has been a gripping watch. Notionally, it should conclude on 15 May when Jerome Powell’s term as chair ends. However, barring a seismic economic shock, the president’s demands that the new chair cut interest rates “at least two to three points” to juice growth will not be met, risking a re-escalation in tensions down the line.

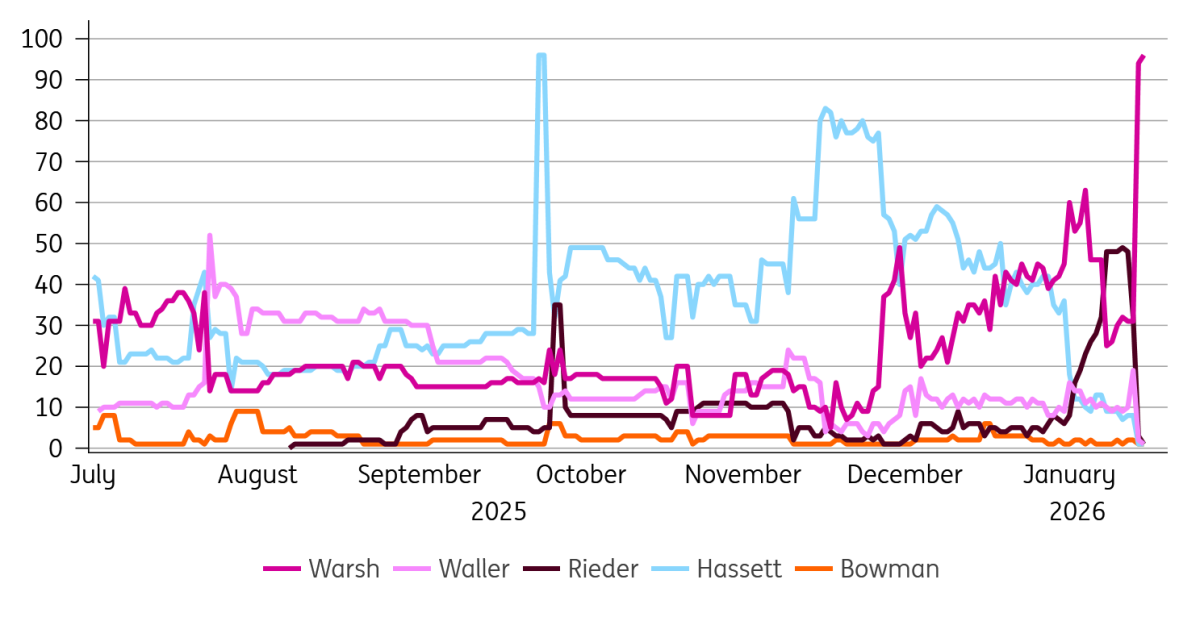

For the past few months, it has been widely assumed that Trump’s pick for chair would be one of Director of the National Economic Council Kevin Hassett, former Fed Governor Kevin Warsh, current Fed Governor Chris Waller and Rick Rieder, BlackRock’s Chief Investment Officer for Global Fixed Income. Headlines at the time of writing suggest Warsh is the favoured candidate, with a formal announcement imminent, despite the perception he was something of an inflation hawk during his previous time at the Fed.

The belief had been that arch-dove Stephen Miran’s temporary governorship, which ends on 31 January, would be used to facilitate entry onto the Board of Governors of an external appointee and with Powell expected to step down as a governor after relinquishing his chair position, another dove could be inserted into the committee. Then, with the Administration assuming it could force out and replace Governor Lisa Cook on “gross negligence” charges over alleged historical mortgage fraud, the president’s desire for lower borrowing costs could be steamrolled through.

Who will be the next Fed chair? Probability in PredictIt prediction markets

The Fed fights back

That is looking less likely by the day, with the Supreme Court arguments on the Lisa Cook case casting doubts on the president’s authority to remove her. This should keep her position safe until the summer – a decision is expected by late June. Moreover, there is a growing belief that Powell, having been served with a Grand Jury subpoena, is emboldened not to step down from his governor role – separate from his chair position – and instead continues to serve as an FOMC voting member until that position expires on 31 January 2028. The rationale being that he will do all he can to protect the Fed’s independence. President Trump acknowledged that prospect, cautioning, “If that happens, his life won’t be very, very happy, I don’t think.”

There are other changes: the scheduled voting rotations see the presidents of the Cleveland, Philadelphia, Dallas, and Minneapolis Feds gaining voting rights, and the presidents of the Chicago, St. Louis, Kansas, and Boston Feds losing them. However, given their respective commentaries, the most we can say is that these changes imply a very, very marginal dovish shift in positioning.

Given that FOMC interest rate decisions are decided by a committee on the basis that each voting member has one vote, a new Fed chair will not be able to do the president’s bidding unless the data supports it, with a majority agreeing. Kevin Warsh's previous experience of the decision-making process and his past emphasis on the need for price stability suggest he will not go down that route if he is indeed confirmed as the president's pick. Instead, we suspect that the new Fed chair would encourage members to be more forward-looking, given valid past criticisms that the Fed has been slow to respond to changing circumstances, most notably the delayed response to evidence of post-pandemic inflation.

Inflation fighting credentials remain critical

In any case, key members within the Administration, such as Treasury Secretary Scott Bessent, recognise that it’s the 10Y Treasury yield that they should be “focused” on given its implications for borrowing costs for households, corporates and government. Unjustified interest rate cuts risk damaging the Fed’s inflation credibility, which could push up the term premium for longer-dated borrowing costs. This would lead to a higher, steeper yield curve, which would undermine the president’s growth targets and potentially the dollar and equity valuations too.

Of course, this raises the interesting possibility, as we wrote in our 2026 outlook, that the “new” Fed may be more willing to restart asset purchases should the 10Y yield start to rise rapidly on, say, fiscal concerns. A more coordinated/collaborative approach between the Treasury and the Federal Reserve means QE action looks more probable.

Despite this, we expect the Fed, even under new management, to emphasise the need for independence, but perhaps be willing to be bolder – willing to take a risk – at potential turning points. As such, it is likely to be more of a gradual evolution rather than a revolution at the new Fed.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Europe’s Arnold moment – why strategy over spectacle matters

- This bundle contains 15 Articles