US economy shrinks on import surge

The economy contracted in the first three months of the year as importers desperately tried to bring in as many goods as possible ahead of tariffs. Inflation was also more elevated, fuelling the stagflation narrative and limiting what the Federal Reserve can do to help as economic sentiment sours

| -0.3% |

QoQ annualised |

US economy contracts for first time since 2022

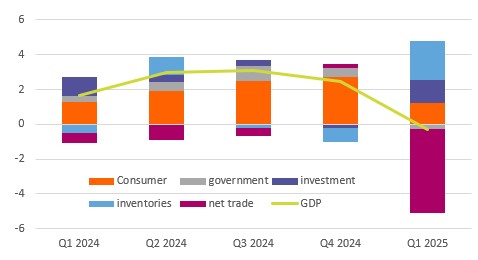

US first quarter GDP contracted at a 0.3% quarter-on-quarter annualised rate, the first time we have seen a drop in output since the second quarter of 2022. The consensus had been dropping sharply in recent days and turned negative yesterday (-0.2%) in the wake of another blowout goods trade deficit. The breakdown shows consumer spending performing better than we expected, rising 1.8% while non-residential fixed investment was robust at 9.8%, led by a 22.5% increase in equipment investment. Government spending cuts were evident with a 5.1% drop in Federal government expenditure dragging overall government spending down by 1.4%.

As widely expected it was the net trade component where most of the weakness was seen with businesses seeking to bring in imports ahead of the tariffs. It subtracted 4.8 percentage points from headline growth as imports surged 41.3% while exports rose only 1.8%. This surge in imports did result in a sharp rise in inventories, which added 2.25pp to headline growth and likely helped facilitate the strong increase in equipment investment.

Contributions to US GDP growth QoQ% annualised

Rather concerningly the price metrics were firmer than anticipated. The core PCE deflator rose 3.5% versus the 3.1% consensus, suggesting a bit more stickiness in inflation than thought ahead of what are likely to be tariff and supply disruption induced price hikes later in the year.

Weak activity and higher inflation set to remain the theme for 2025

Given this situation, the stagflation narrative is likely to continue to dominate economic debate. Yesterday's consumer confidence report suggests the risks are skewed towards a substantial slowdown in consumer spending as households face up to squeezed spending power from higher prices at a time when they are increasingly concerned about job losses and falling wealth. Government spending cuts are set to continue and with businesses uncertain about the trading environment due to worries about tariffs and potential supply shortages in coming months it looks as though hiring and investment will slow too.

With the inflation backdrop limiting what the Fed can do to help in the near term there appears to be little prospect of imminent interest rate cuts. However, we need to remember that inflation isn’t just goods. Services dominate and with foreign tourism dropping off and consumer caution becoming more apparent, we expect to see further weakness in leisure and hospitality pricing, air fares and eventually housing costs. When the Fed does come to the rescue at some point in the third quarter we suspect they will move hard and fast and fully understand why markets are now pricing 100bp of interest rates cuts for the year versus 79bp this time last week.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article