US consumers can’t lose the spending bug

- 16 July 2021

- United States

Strong June US retail sales suggests no let up in the appetite of consumers to spend on physical things despite the economic re-opening providing a broadening range of options, such as leisure and hospitality. With finances in great shape and incomes continuing to rise the outlook for spending is excellent

| 18.5% |

The annual rate of US retail sales growth |

Spending surprises despite downward revisions

US retail sales rose 0.6% month-on-month in June, a much better outcome than the 0.4% fall the surveys of economists were pointing too. There were downward revisions to May’s growth figure (-1.7% versus the -1.3% rate initially reported), but June’s better growth more than offsets this.

Vehicle sales were a drag, but not by as much as feared. They declined 2% MoM in value terms, which seems a little odd given unit sales of 15.4mn versus 17.0mn in May. The price rises reported in the CPI release were not enough to offset that so there could be some downward revision potential further down the line. Nonetheless, it is important to remember that softness in auto sales is because of the lack of available vehicles to buy given production/supply chain issues, rather than weak demand. The 45% year-on-year increase in used car prices is a testament to this.

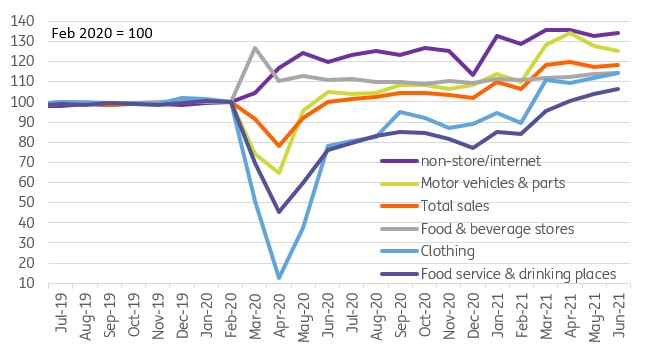

The appetite to keep spending was clearly seen in other components with sales excluding vehicles rising 1.3% versus expectations of a 0.4% gain. May’s growth figure was revise down by two tenths of a percentage point, but today’s report is clearly still a positive surprise. Electronics rose 3.3%, clothing was up 2.5%, eating and drinking out was up 2.3%, miscellaneous was up 3.4% and general merchandise was up 3.4%. On the negative side building material sales fell 1.6%, furniture fell 3.6% and sporting goods dropped 1.7%. As can be seen below, all of the major components are above pre-pandemic levels of spending.

US retail sales component spending levels (February 2020 = 100)

Strong foundations for further growth

This is an encouraging report that suggests consumer spending momentum remains strong. Moreover, retail sales is typically “only” 40-45% of total consumer spending, which in turn is usually around 65-70% of GDP. Clearly it is a very important component of overall economic activity, but with the economy re-opening there are a greater number of options on which to spend money. We will increasingly see a rebalancing of consumers’ total spend away from "things" that are picked up in retail sales, towards "experiences", such as travel, entertainment and leisure, which are not.

Today’s report suggests we shouldn’t fear a resulting drop in retail sales. Both goods and services can continue to grow. After all, consumer finances remain in great shape with incomes picking up and credit card borrowing having been paid down. Meanwhile, the Federal Reserve flow of funds data showed households have seen their wealth surge $20tn since the end of 2019 with $3tn of that increase in liquid cash, checking and time savings deposits. That is a huge amount of financial ammunition that could support strong consumer spending over many quarters.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more