UK money markets transitioning to a new monetary policy regime

With the Bank of England in easing mode, overnight rates will gradually become less attractive. Already we see value further out the curve as we see more room for policy rate cuts than markets. Overall liquidity conditions should remain good, with revamped central bank facilities giving access to liquidity at attractive pricing, also in times of stress

Money market funds benefit from inverted curve

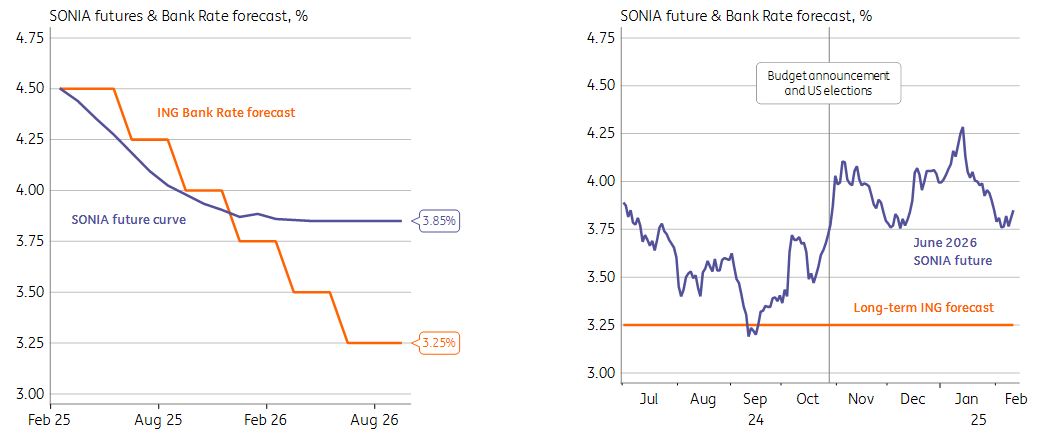

Since the turn of the monetary policy cycle in 2023, money market funds have seen significant inflows, but we think the peak has been reached. The difference between storing money overnight and investing in a 1Y UK government bond is now 100bp, but this will decline as the Bank of England (BoE) continues to cut. A resteepening of the curve makes it more attractive to fix rates at longer tenors, outside of money market funds.

Steeper curves will see outflows from money market funds

Markets currently price just 60bp of cuts from the BoE in 2025, which is still more dovish than at the start of the year. And although we also reduced the number of cuts in our forecast for 2025, we believe markets are underestimating the easing potential. We think 75bp of cuts is more likely, with another 25bp cut in 2026, with the risk tilted towards even more cuts. As such, we continue to see better value further out on the money market curve.

SONIA futures suggest just three more 25bp cuts, significantly less than our forecast

Bank of England facilities help offset falling bank reserves

As part of the broader policy normalisation process, the Bank of England continues unwinding its bond portfolio at a rate of £100bn per year, further withdrawing bank reserves from the system. Since early 2024, the Short-Term Repo (STR) facility has already seen increased uptake, supplying banks with reserves over weekly horizons. Now the BoE is also making a push to increase the use of the Indexed Long-Term Repo (ILTR), which offers reserves over a period of six months against various types of collateral.

ILTR and STR will help with liquidity while BoE unwinds bond portfolio

To stimulate the use of the ILTR, the BoE will tweak the pricing of the liquidity facility in the first half of 2025. As part of the monetary policy normalisation efforts, the BoE sees the ILTR as an important supplier of bank reserves. So far banks have made little use of the facility, but as reserves become more scarce and the pricing is made more attractive, we expect the ILTR to see significantly more uptake later this year. In effect, this reduces the pace at which bank reserves will diminish.

New Contingent Non-Bank Lending Facility introduced for times of liquidity stress

Furthermore, the BoE introduced the new Contingent Non-Bank Lending Facility on 28 January, which offers non-banks access to liquidity against gilts collateral. The facility will only be opened during times of stress in the gilt market and the pricing and terms are at the discretion of the BoE. As such, this backstop should prevent liquidity squeezes spilling over to gilt markets, as seen during mini-budget episode in October 2022.

Back then, former UK prime minister Liz Truss triggered a gilt sell-off in the pensions sector due to a need for liquidity to serve margin calls on interest rate derivatives. With this new facility, pension funds would have access to liquidity directly from the central bank, thereby preventing a broader sell-off in gilts. Overall, this facility should make the gilt market more resilient during times of stress, but the impact on money markets pricing is negligible.

Overnight rates already reflect a tightening of liquidity

The reduction in bank reserves is already being expressed in higher overnight deposit rates, but the upside is limited. The Sterling Overnight Index Average (SONIA) is now around 5bp below the Bank Rate and since the start of 2025 it has been nudging up again. Also when looking at the underlying distribution, the dispersion increased, suggesting some banks are increasing the interest rate they are willing to pay to attract deposits.

SONIA is an unsecured rate, which should in theory compensate lenders with a higher interest rate than secured funding (e.g., through repo). Yet due to market segmentation, money markets are not fully efficient. Only banks and a small subset of other financials can use the BoE’s deposit facility. As such, the SONIA rate can remain below the Bank Rate. Over time, lower bank reserves will increase the competition for deposits among banks, thereby pulling SONIA closer to the Bank Rate. Since banks can obtain (secured) funding from the BoE at the Bank Rate or at a small spread above it, SONIA is unlikely to drift far above the Bank Rate.

SONIA will drift closer to Bank Rate, but upside limited

Rates further out the curve are also showing signs of normalisation

Even though the BoE intends to keep the market impact at a minimum, the ILTR helps provide a soft cap on term rates. The pricing for the facility starts as low as the Bank Rate for high quality collateral (i.e., gilts) and can therefore offer an attractive alternative to market funding. Having said that, the BoE raises the price when the auction demand for the ILTR increases and money markets should therefore remain the main source of liquidity. But overall, the facility will help keep money market rates close to the policy rate.

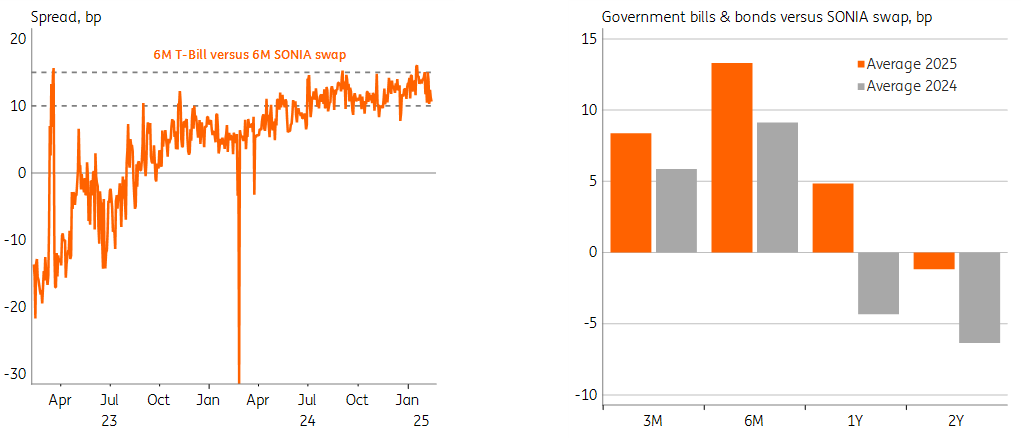

Since 2023, the 6-month treasury bill trades at a higher rate than the equivalent SONIA swap, but we don’t expect that the widening can go much further. The ILTR offers repo funding over six month periods, which in theory caps the 6-month bill to the Bank Rate. In practice, one needs to add a spread to account for the associated balance sheet costs and the remaining stigma from using a BoE facility. The 6-month bill can therefore continue to trade in the recent range of 10-15bp above SONIA.

Funding costs are normalising and BoE facilities like ILTR provide soft cap

The yields on government bills seem to have stabilised in recent months around 10bp above the SONIA swap, but for 1Y and 2Y tenors, there is scope for further widening. The 2Y spread was still negative for most of this year, but we can expect this to drift higher as the year progresses. If anything, the 2Y gilt may even settle at a spread above those of shorter tenors, as the 10Y spread further out the curve is already much higher at 50bp.

Overnight is attractive, but value in longer tenors

A key takeaway from all of this is that overnight rates still provide the highest return in an absolute sense, but this advantage should fade going forward. In relative terms, we think longer tenors provide better value, as we see more room for the Bank of England to cut than markets are pricing in. When looking at the cross-section of treasury bill rates, the sweet spot seems to be in 6-month tenors, where spreads versus SONIA swaps are widest. The ongoing tightening of liquidity conditions could still widen spreads further, especially at tenors beyond 1-year, but the BoE’s liquidity facilities should prevent sharp moves.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

18 February 2025

Money market outlook 2025 This bundle contains 4 Articles