UK economy heading for October contraction as Covid-19 returns

The UK recovery is set to stall through the autumn and winter as the 'reopening phase' ends and new Covid-19 restrictions are brought in. As the Chancellor announces fresh stimulus, we've taken a look at what new virus measures could mean for the economy. A decline in October's GDP data looks likely

The UK is seeing early signs of a renewed spike in Covid-19 transmission

UK Chancellor Rishi Sunak has announced fresh economic support today, with a new wage-subsidy scheme designed to top-up the pay-packets of employees working reduced hours.

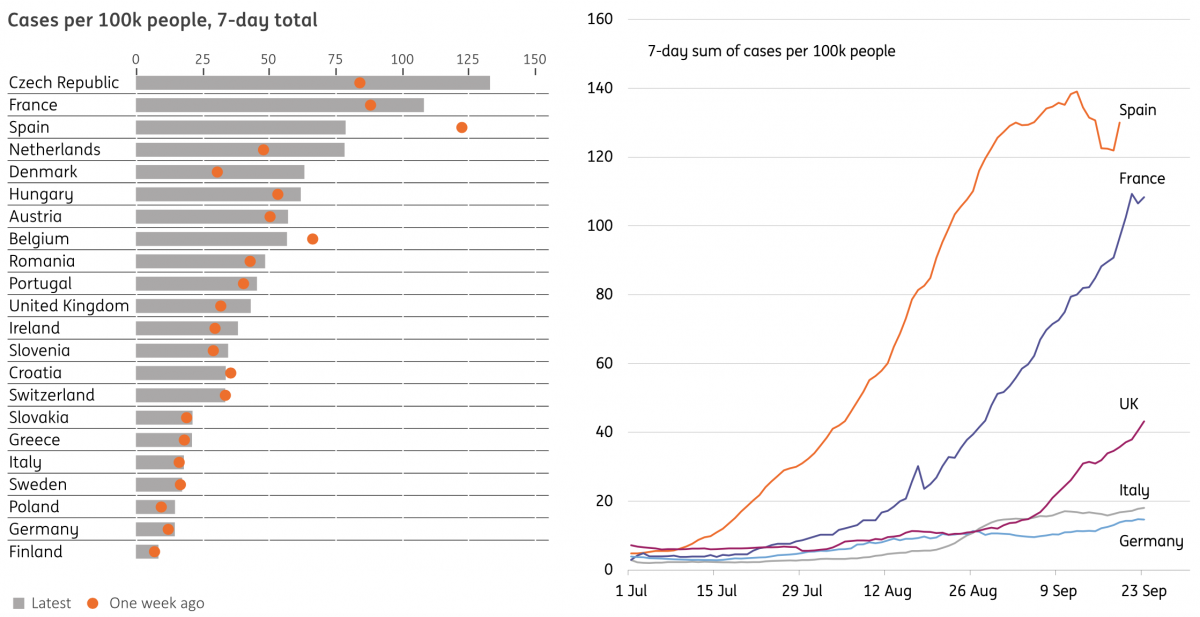

This comes amid a fresh spike in Covid-19 cases in the UK. So far the viral spread is at a less advanced stage than in other parts of Europe - the UK has recorded around 40 cases per 100,000 people over the past week, compared to over 100 in both France and Spain. But concerns that this could soon translate into a rise in hospitalisations have triggered a fresh round of restrictions across the UK.

So what’s the scale of the economic challenge that Sunak is facing as he unveils his 'winter economic plan'?

Coronavirus compared: UK cases rising, albeit not yet as fast as elsewhere in Europe

Well firstly, it’s worth remembering that the recovery was always likely to stall during the fourth quarter, now that the ‘reopening phase’ is over. And so far, the restrictions that have been announced over the past few days are unlikely to make a huge dent on GDP. The new rules, including covering those areas with higher levels of the virus, are predominantly focussed on limiting social gatherings rather than outright closure of certain economic sectors.

But there’s still a clear risk that further measures could be on their way if the rate of case growth doesn’t slow. A number of recent headlines have indicated the government may be mulling a two-week ‘circuit-breaker’ mini-lockdown.

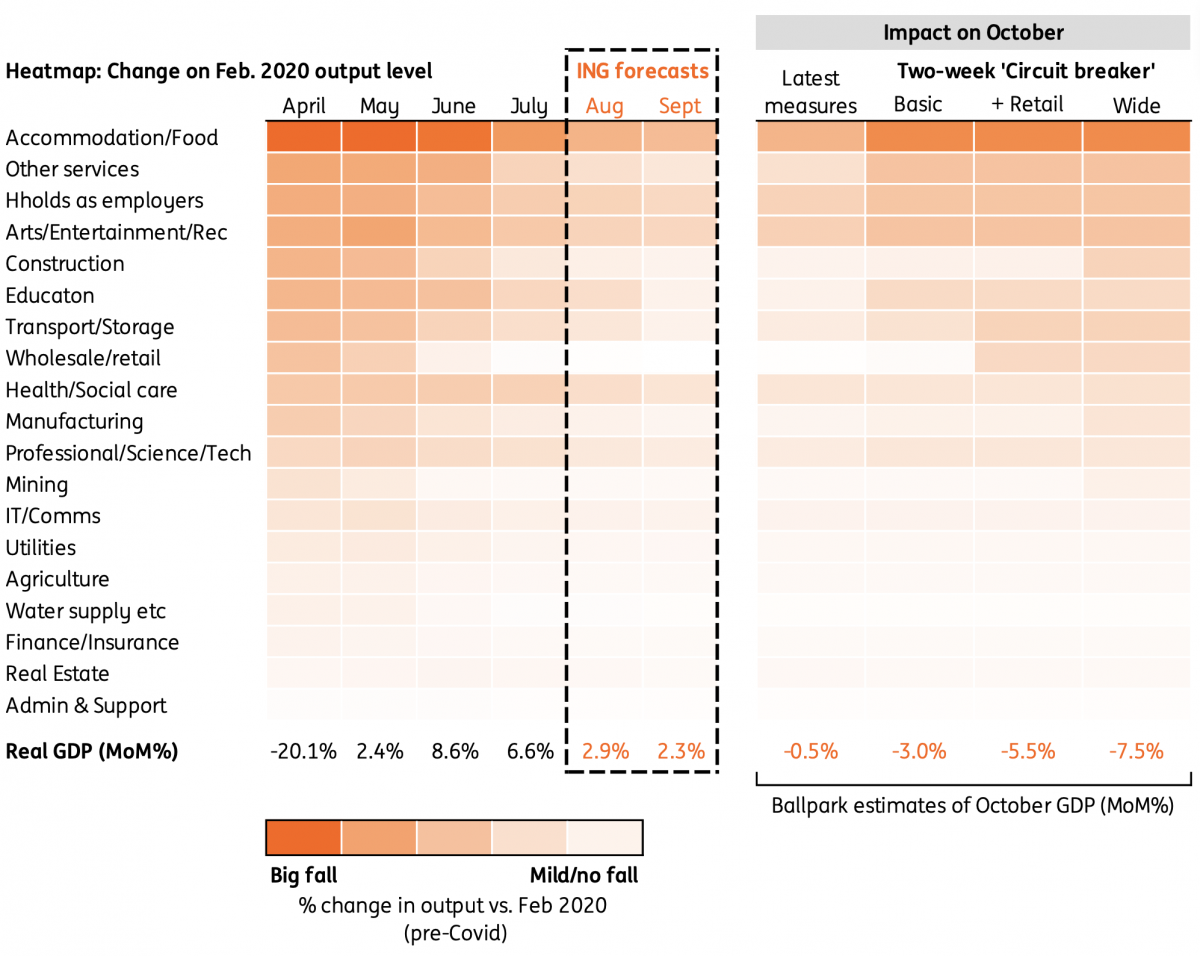

We think that a two-week ‘circuit-break’ involving closure of hospitality and schools could see October GDP fall by around 3%. If these measures also involved shop closures, then that decline could rise to 5-6%

What might that involve? Well, the key point is that this appears very unlikely to involve the severity of restrictions imposed back in March. Reports suggest this kind of scenario could see pubs and restaurants asked to close for a two-week period, as well as potentially schools.

We’ve done some ‘back of the envelope’ calculations to see what this might mean for October’s GDP figures, based on some assumptions on the impact at a sector-level. The heatmap shows the worst affected sectors during the initial lockdown (measured by the change on pre-virus levels), how they've recovered since, and how that might change under different ‘circuit breaker’ scenarios.

Four indicative scenarios for UK October GDP depending on Covid-19 restrictions

In short, we reckon that a two-week ‘circuit-break’ involving the closure of the hospitality sector and schools could see October GDP fall by around 3%. If these measures also involved shop closures, then that decline could rise to 5-6%, and if a wider range of sectors were included (e.g. parts of manufacturing/construction), then perhaps we’d be looking at a 7-8% contraction.

All of this is, of course, fairly rough-and-ready, and there are a few key ways in which the impact could vary.

The most obvious variable is the length of any such restrictions - would they really last two-weeks? The above estimates assume they do, but the question is whether ministers would have enough data after 14-days of closures to conclude that the virus spread has sufficiently slowed? While the bar for schools to stay shut for any longer appears high, it’s not inconceivable that the likes of pubs/restaurants could stay closed for longer in this kind of scenario. The effect would be to drag overall fourth-quarter GDP lower (see box below).

Will the public 'act with their feet'

Secondly, how will the public react? Evidence from the first round of lockdowns suggests that, regardless of the measures that were imposed, consumers often ‘acted with their feet’ and voluntarily restricted their movements given safety concerns.

So far, and perhaps not surprisingly, we’ve not seen much evidence of this during this second spike. While both restaurant bookings and retail footfall have leveled off over the past couple of weeks, neither dataset suggests consumers are meaningfully changing their habits again in response to virus fears. So far this is consistent with what we’ve seen in other European hotspots, at least according to Google Mobility data.

The UK's Google Mobility data

Fresh uncertainty poses additional challenge for jobs market

However, as our Eurozone team have highlighted, business surveys including the latest Europe PMIs, are beginning to air some fresh concerns about damage from the second wave. This brings us onto a third factor - uncertainty.

With the exception of some local lockdowns, the operating environment has been kept relatively stable over the summer as Covid-19 prevalence has stayed low. But the imposition of new restrictions will raise fresh questions about what the winter will bring for businesses - and it will inevitably see firms ramp-up plans for a return to full lockdown, even if in reality that currently appears a fairly low-probability event.

The primary impact is likely to be on jobs. There are already early signs in the latest data that the unemployment rate starting to rise, and we have thought it could hit 9% by the end of the year or early next.

The Chancellor's new wage subsidy scheme, which will subsidise a portion of an employee's salary if they are able to work at least a third of their normal hours, should help head-off some of the redundancies that may have otherwise occurred with the closure of existing Job Retention scheme in October.

However, inevitably this leaves some concerns about what will happen in sectors still effectively closed (e.g. events), where labour demand may insufficient for firms to justify bringing staff back on a part-time basis, and where the jobs will eventually be viable again once restrictions ease.

Further Bank of England action likely in November

The threat of a challenging fourth quarter suggests that the Bank of England will also inject fresh stimulus in November. The question now is what this might involve. Despite all the hype over negative rates, it’s clear from recent comments from Governor Andrew Bailey that quantitative easing remains the favoured tool. He also noted this week that negative rates, whilst in the toolkit, are unlikely to become a reality this year.

A side-note about fourth quarter GDP

Although, we've focussed on what possible restrictions might mean for October GDP, but what will the impact be on the full fourth-quarter figures?

Well, we know that third-quarter GDP is likely to come in at a blockbuster 16-17% QoQ, although this is of course because you are comparing it to a three-month period where the economy was essentially shut.

We're likely to see a similar, albeit smaller effect in the fourth quarter too. The economy was still getting back on its feet through July and August. So even if hypothetically the monthly level of GDP stays unchanged at September's forecasted level through October-December, then overall fourth-quarter GDP will still be around 2-3% higher than the overall GDP in the third.

The implication is that under the two-week 'basic' circuit-breaker scenario detailed above, we could still see overall quarterly GDP come in flat or even slightly positive for the fourth quarter as a whole. It all really depends on how all-encompassing the restrictions are on different sectors, and more importantly how long they end up lasting.

A wider 'circuit-break', or one that lasts longer than two weeks, would almost certainly drag fourth-quarter GDP below zero, even with the favourable 'base effect'.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

24 September 2020

Covid spikes threaten the recovery This bundle contains 10 Articles