Trump’s 50% tariff on aluminium will lift US prices and shift trade patterns

US President Donald Trump has raised steel and aluminium tariffs to 50% from 25%, which took effect on Wednesday. The tariffs are likely to weigh most heavily on the US aluminium market amid a lack of domestic capacity, and with the US importing significant volumes of the metal from abroad

President Trump hopes the increased levies on aluminium will protect margins for domestic mills and spur investment in new production capacity. The tariffs will not apply to imports from the UK, which will remain at 25%, to allow for negotiations on new tariffs or quotas by the 9 July deadline.

The doubling of tariffs has come after a federal court struck down some of Trump’s other duties, which were put in place under an emergency law. His tariffs on metals were not subject to that ruling.

US needs imports to meet domestic demand

The US is a net importer of aluminium with its domestic production not enough to meet its needs. This is unlikely to change soon.

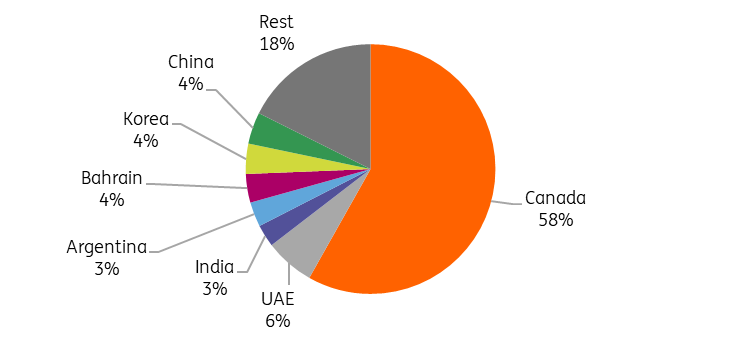

The US imports roughly half of its aluminium from abroad, with Canada the biggest supplier, accounting for 58% of imports. That's followed by 6% from the United Arab Emirates, figures from the US government show. The US also relies on Mexico and Canada for around 90% of its aluminium scrap imports.

Industries like automotive and manufacturing in the US, which heavily rely on aluminium imports and are deeply integrated with US supply chains, would face increased costs and disruptions since many parts cross the border multiple times before becoming a final product.

US imports more than half its aluminium from Canada

US aluminium prices surge on higher tariffs

These new tariffs will raise the price of aluminium in the US even further. Following Trump’s announcement, the US Midwest aluminium premium surged more than 50% this week to the highest since 2013. The increase in the premium, which is the best indicator of tariff risk, suggests US consumers could be paying about 50% more for the metal than international buyers.

The premium is added on top of the global benchmark prices, which are set on the LME to deliver the metal to the US Midwest.

Tariffs also risk demand destruction in the US, as the extra costs would most likely be passed on to end consumers.

US aluminium premiums surge as Trump doubles tariffs

Trump said the tariffs are aimed at bolstering domestic production and bringing jobs back to the US. However, in 2024, the output of the US aluminium industry was 10% lower than in 2017, before the introduction of the first round of Trump tariffs.

The aluminium industry has shrunk dramatically over the past few decades. In the 1980s, the US produced more than 30% of the world's aluminium; now, it produces 1%.

Rising energy costs have played a major role in the decline of the US smelting industry over the years. Canada's aluminium industry, on the other hand, benefits from cheap hydropower to power its smelters.

The US currently has four operating aluminium smelters, which together produced 680,000 tonnes of metal in 2024. This compares with the US consumption of around 4.9 million tonnes.

Higher tariffs on imports could lead to additional domestic smelter investment and development. However, restarting idled smelters could take months, while building a new smelter would take even longer.

Last month, Emirates Global Aluminium announced plans for a new aluminium smelter in the US, which could help reduce the US’s reliance on imported aluminium and increase domestic aluminium production. The plant will be the first new primary aluminium smelter built in the US in over 40 years. It is expected to have a capacity of 600,000 metric tonnes per year, nearly doubling the US primary aluminium output. Construction is expected to start by late 2026 and be completed by the end of the decade, with first production anticipated by 2030. Its final go-ahead is contingent on securing a long-term power supply.

Is copper next on Trump's tariff list?

The increase in steel and aluminium tariffs also increases the likelihood of the implementation of copper tariffs. Copper prices in New York are rising again this week after hitting record highs earlier this year. Copper prices in the US are up by more than 20% so far this year, as prices have continued to benefit from front-running of tariffs, while prices in London have risen around 10% this year.

The race to get copper to the US before any tariffs are introduced has tightened markets elsewhere. It started in late February, when copper prices in New York surged above London prices after President Trump launched an investigation into whether to impose import tariffs on the metal. Comex copper stocks are at the highest level since 2018, while inventories in the SHFE warehouses are at the lowest since 2022, and in the LME sheds, they now stand at the lowest level since June.

The US is reliant on copper imports for its domestic consumption. In 2024, the US imported around 850,000 tonnes of copper (excluding scrap), accounting for around 50% of its domestic consumption. Like for aluminium, it might be challenging to replace US copper imports with domestic production, at least in the near term.

Comex copper stocks are at the highest level since 2018

Meanwhile, steel and aluminium cargoes are being diverted from the US since the imposition of 25% tariffs earlier this year, with traders redirecting sales to Europe to avoid Trump’s tariff chaos, putting pressure on European premiums. The full impact of tariffs will likely take time to become more apparent, but they are likely to lead to a realignment of global trading patterns.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article