Transportation & power sectors are key for metals outlook

- 13 October 2021

- Commodities, Food & Agri Sustainability

Copper, aluminium, nickel, cobalt and lithium are all set to benefit from the energy transition. How much will depend on the proactiveness of government and the private sector. The trend is clear, it is just a matter of how quickly it happens. Here is how we see demand from road transportation and the power sector evolving under our scenarios

Copper

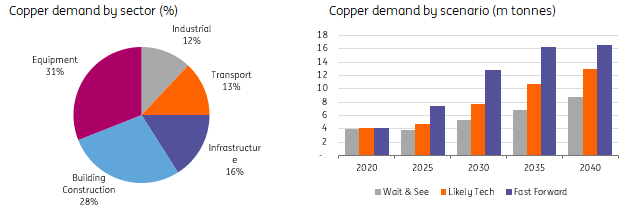

Global copper consumption is estimated at almost 29mt. It has grown at a compound annual rate of 1.97% between 2012 and 2019.

Equipment and building construction are the largest end users of copper, making up 31% and 28% of total demand, respectively. Infrastructure and transportation follow at 16% and 13%, respectively, whilst the remainder goes towards the industrial sector. Infrastructure will include transmission and distribution networks, as well as telecommunication networks. The bulk of transportation demand will go towards road transportation, but there is also a sizeable amount that goes towards railroads and shipping.

Copper demand will benefit from a growing share of electric vehicles, along with more renewable infrastructure and investment in the grid. Under our 'Wait & See' scenario, copper demand from road transportation and the power sector grows by 117% between 2020 and 2040, equivalent to a compound annual growth rate of 3.9%. Copper demand grows at annual rate of 6% under our 'Likely Tech' scenario, while under our most aggressive scenario, 'Fast Forward', demand from these two sectors grows at a CAGR of 7.2% to total almost 17mt by 2040.

Copper demand split and demand outlook by scenario for road transportation & power sector

Aluminium

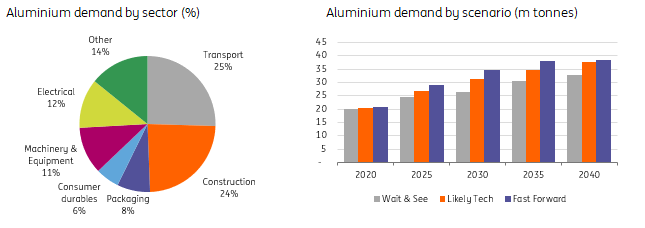

Current annual aluminium consumption totals around 90mt (including secondary aluminium). The largest end user for aluminium is transportation, making up 25% of total demand. The next two largest end users are construction and electrical, making up 24% and 12%, respectively.

Aluminium is another big winner from the energy transition. The metal has already benefited from the push towards lightweighting to improve vehicle efficiency and there is further upside ahead. Lightweighting is even more important for EVs as an even larger proportion of the chassis and body use aluminium. Meanwhile, increased wind and solar deployment in the power sector will drive higher aluminium demand. Given the cost advantage of using aluminium over copper as well as its lighter weight, almost all above ground transmission and distribution lines will use aluminium. A larger share of aluminium cables may also be used underground given the cost advantage.

While there will be significant growth in aluminium demand from EVs, there will be displacement from reduced ICE vehicle sales. Therefore demand growth for total road transportation will be much more modest than growth seen from the EV segment. Our 'Fast Forward' scenario sees aluminium demand from road transportation and the power sector grow by a little over 3% per annum between now and 2040, or from a little more than 20mt to 38mt by 2040. Our 'Likely Tech' scenario sees similar annual growth over the period, while under our 'Wait & See' scenario, demand grows at an average of 2.5% per year.

Aluminium demand split and demand outlook by scenario for road transportation & power sector

Nickel

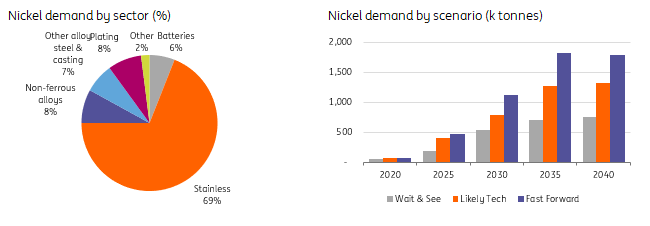

Nickel demand currently stands at around 2.4mt and is dominated by stainless steel. Almost 70% of demand comes from the stainless steel sector. The battery industry still makes up a small proportion of nickel demand at just 6%. However, with the expected growth in EVs, this is expected to grow significantly in the years ahead.

Nickel demand from the power sector will not be significant, with demand from stationary storage relatively small. However, the use of stainless steel in renewable infrastructure will indirectly be advantageous for nickel, given its use in stainless steel production.

Nickel demand from road transportation and the power sector grows by 13.2% per annum between now and 2040 under our 'Wait & See' scenario, 15.3% per annum under our 'Likely Tech' scenario and 16.8% in our 'Fast Forward' scenario.

Nickel demand split and demand outlook by sector for road transportation & power sector

Lithium

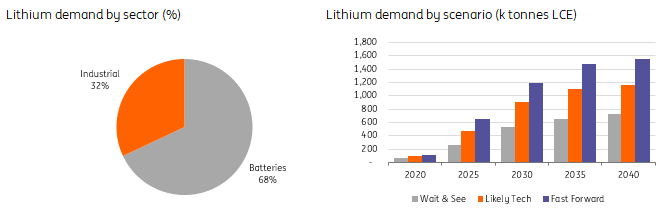

Global annual lithium demand totals 290kt LCE. The growth in electric vehicle sales is largely behind this and is clearly a trend which is set to continue. The batteries industry makes up the bulk of lithium demand, at close to 70%. Clearly, technology advances are a risk to the bullish demand outlook for lithium. However, we assume under all our scenarios that lithium-ion batteries will be the dominant battery used by vehicle manufacturers.

Looking at road transportation and the power sector, it is the former which will dominate future demand growth. The power sector will see growth from a build-up in stationary energy storage capacity but the absolute numbers are a fraction of what will be seen in electric vehicles.

Under our 'Wait & See' scenario, we see total lithium demand from EVs and the power sector growing by 13% p.a. through until 2040. While under our 'Fast Forward' scenario, annual demand growth will be around 14% to leave demand from these two sectors at 1.6mt LCE by 2040.

Lithium demand split and demand outlook by scenario for road transportation & power sector

Cobalt

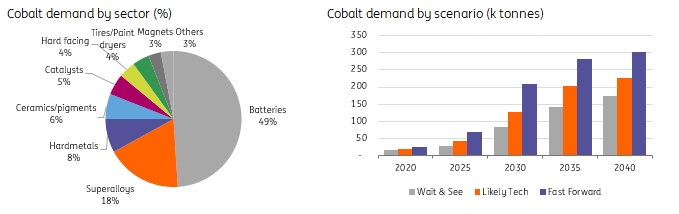

Cobalt demand currently stands at around 135ktpa, with the battery industry dominating demand, making up almost 50% of total cobalt consumption. Like nickel, cobalt demand will be largely driven by the transportation sector, while the power sector sees much more modest demand under all of our scenarios.

There is plenty of concentration risk around cobalt, with 66% of current supply coming from the Democratic Republic of Congo. In addition, there are worries over the sustainability of the DRC supply chain, particularly when it comes to supply from artisanal mines. As a result, there is a push to reduce the use of cobalt in lithium-ion batteries and even produce cobalt free batteries. The battery chemistry used in future is a key uncertainty when it comes to forecasting cobalt demand under our different scenarios.

Under our 'Fast Forward' scenario, we forecast that cobalt demand from road transportation and the power sector grows at an annual rate of 13.6% through until 2040. Demand under the 'Likely Tech' scenario grows at a CAGR of 13.2%, while under our most pessimistic scenario, 'Wait & See', cobalt demand grows by 12.8% per year.

Cobalt demand split and demand outlook by scenario for road transportation & power sector

In the next two articles we will dive deeper into the industries which we believe will drive metals demand higher in the years to come. Specifically, road transportation and the power sector.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Energy transition: Metals demand set to take off

- This bundle contains 7 Articles