Trade update: reciprocal tariffs, fragile deals and legal uncertainty

As of 7 August, the US enacted a sweeping set of reciprocal tariffs, with rates ranging from 10% to 41%, following the Executive Order issued on 31 July. While some countries have reached preliminary agreements with the US, many of these deals remain non-binding and subject to unilateral revision

Where we are right now

- Elevated tariffs expected to persist through year-end, with the US effective average tariff rate remaining at 15-20%, above earlier projections.

- Legal uncertainty surrounds IEEPA-based tariffs; fallback mechanisms for the administration include Section 122 (15% cap, renewable) and Section 338 (up to 50% tariffs or import bans).

- Trade deals offer limited relief, with many agreements still non-binding, symbolic, or logistically unfeasible.

- Retaliation risk rising, especially if deals collapse or unilateral changes continue

Tariffs take hold: The ‘Liberation Day’ legacy is here

Remember 2 April? That was the original date, dubbed ‘Liberation Day’, when President Trump first hurled the tariff hammer at the world. This initial announcement triggered a sharp sell-off, with US equities experiencing their worst single-day losses since the pandemic. Now, four months later, the higher tariffs have come into effect, ranging from a minimum of 10% to a maximum of 41%. Transhipped goods are subject to a 40% tariff, although it is not clear how those goods are actually identified.

Goods that were already loaded and moving before 7 August 12:01 a.m. EDT, and that arrive and are processed before 5 October 2025 at 12:01 a.m. EDT, will not face the new tariffs. Instead, they’ll be taxed under the older rates to avoid penalising shipments that were already en route when the new tariffs were announced.

Symbolic deals or real relief?

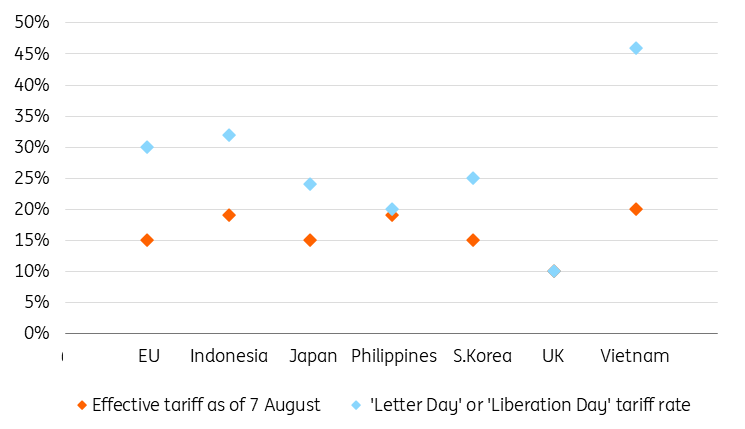

Several countries have reached preliminary agreements with the US. However, many are not legally binding, and President Trump already unleashed a new set of threats, such as a 35% on the EU if it doesn’t provide the $600bn investments to the President’s liking. We’ve said it before, and we'll say it again: this 7 August date does not mark the end of the tariff saga, and higher tariffs on individual countries could still be imposed. Also, regarding ‘trade deals’, final, legally binding agreements may differ from what’s been publicly announced. Vietnam, for instance, expected an 11% tariff but received 20%, a change made unilaterally by President Trump. And remember, several deal components appear unfeasible or largely symbolic indeed (e.g. the EU’s promise of buying $750bn US energy products within the next three years) and could ultimately fall apart.

Compared to our base case from early July, recent trade deals have also turned out less favourable for US trade partners than anticipated. As a result, the average US tariff rate has risen to 18.2% as of 7 August (estimates from the Budget Lab), with some countries facing significantly higher rates. This is above the previously expected 12% to 15% range.

Still, for some of the US's largest trading partners, the new tariff rates are more favourable than previously announced. Notably, the EU has secured itself a ‘big and huge deal’, as the 15% is a flat tax, meaning the duty for a good below 15% will be raised to a maximum of 15%, while goods taxed above 15% will not see additional tariffs. For all other countries, any additional duties, fees and surcharges apply, often raising the actual tariff rate above the tariff rate listed in the Executive Order’s Annexes.

Overall, however, the US trade and tariff strategy remains a mystery – countries which have not engaged in negotiations have received more favourable rates than countries which have. Another factor which is thus highly likely to persist: The irrationality in the US trade strategy.

‘Trade deals’ leading to lower tariff rates as of 7 August

Overall, however, a lot still hangs in the balance. Mexico and China are still locked in negotiations.

Mexico received a 90-day extension, maintaining tariffs at 25% for non-USMCA goods and up to 50% for metals.

China has a deadline of 12 August. It's officially a binding date, but, of course, it could be extended.

And some countries are already facing a harsher tariff regime, namely Canada, India and Brazil.

Since 1 August, the tariff rate on Canadian non-USMCA compliant goods has risen from 25% to 35%.

As of 6 August, Brazilian goods face an additional tariff rate of 40%, which, combined with the 10% baseline rate effective from 7 August, brings the total to 50%.

India’s tariff rate will be raised to a total of 50% - 25% reciprocal tariffs plus an additional 25% tariff for buying Russian Federation oil, effective 27 August.

And a quick word on Sectoral tariffs and 'de minimis' suspension: Sectoral tariffs are in place or are due to be implemented, subject to the findings of the Section 232 and Section 301 investigations.

Pending Section 232...

...and Section 301 investigations

There has also been an update regarding de minimis shipments. While the de-minimis exemption for shipments from China has already been suspended as of 2 May, as of 29 August, all de minimis exemptions for commercial shipments globally have been suspended. Previously, goods valued under $800 were duty-free. Now, imported goods sent via non-postal channels and valued at or below $800 will be subject to all applicable duties. For goods shipped through the international postal system, duties will be assessed using one of the following methods:

- Flat-rate duties apply for 6 months:

- $80/item for <16% tariff countries

- $160/item for 16–25%

- $200/item for >25%

- After 6 months, ad valorem tariffs based on country-specific IEEPA rates.

Over 1.36 billion de minimis shipments entered the US in 2024, up from 134 million shipments in 2015, according to the White House.

Protectionism persists as US tariff strategy deepens amid labour market cracks

Protectionism remains the dominant theme, and despite the US economy appearing to be doing well on paper, cracks are beginning to appear, as evidenced by the weak jobs report in July and the major downward revisions to May and June. It led to the sacking of the US Bureau of Labour Statistics Head, Erika McEntarfer – don’t expect any changes in the US stance yet, but rather an intensification (e.g. Section 232 and Section 301 tariffs).

This means that the average US tariff rate, previously assessed to remain between some 12% to 15%, is likely to remain around this higher level until the end of the year, assuming the court does not invalidate the IEEPA tariffs. This adds another layer of uncertainty regarding the trade and tariff landscape.

Legal uncertainty: IEEPA in court

Above all, the cloud of legal uncertainty continues to hang over everything. On 31 July, the US Court of Appeals heard arguments on whether President Trump exceeded his authority under the International Emergency Economic Powers Act (IEEPA). The lower court had already ruled that the IEEPA does not grant the president unilateral power to impose broad import duties, especially when the declared national emergencies – such as drug trafficking or trade imbalances – are not directly addressed by the tariffs themselves.

If the appellate court upholds the ruling, the administration may be forced to unwind tariffs that have generated over $46.8 billion in revenue in the fiscal year 2025 up to 13 July, according to the CBP trade statistics data, with $18.4 billion paid on goods from China and Hong Kong alone. However, fallback options remain. These include:

- Section 122: Allows for tariffs up to 15%, renewable every 150 days, but requires Congressional approval for extensions

- Section 338: Enables up to 50% tariffs or import bans in response to discriminatory practices

The legal ambiguity surrounding IEEPA-based tariffs adds another layer of complexity to the trade landscape as it affects the credibility of existing deals. In short, the US tariff regime is unlikely to soften. Even if the courts strike down IEEPA-based tariffs, the administration retains a robust legal toolkit to maintain or escalate trade barriers. This entrenched protectionism, coupled with legal volatility, ensures that uncertainty will persist well into the final quarter of 2025.

Retaliation remains a real risk

Retaliation remains limited for now, but the risk is rising. If deals collapse or unilateral changes from the US side persist, expect more aggressive responses from affected countries. The trade landscape is shifting – and not necessarily in favour of global stability.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article