3 reasons for weak investment in the eurozone

Eurozone investment has fallen behind its pre-pandemic trend because of the underperformance of capital-intensive industries, high interest rates and policy uncertainty. Governments are now also starting to tighten their belts, leaving little room for a vigorous recovery in the near term

Like in the US, investment is underperforming in the eurozone. Investment (gross fixed capital formation) is about 10% below where it would have been had it followed the pre-pandemic trend, and keep in mind that the trend was already very weak before the pandemic started. Unlike the US, the eurozone suffered from an energy crisis, which explains to a large extent the divergence in economic developments after the pandemic. Still, the weak investment performance in the eurozone cannot be explained by the energy crisis and energy uncertainty alone. For a region that needs to overhaul defence spending, requires an urgent energy transition, and faces structural labour shortages, shouldn’t investment be higher?

Weak demand and a bleak outlook push investment below trend

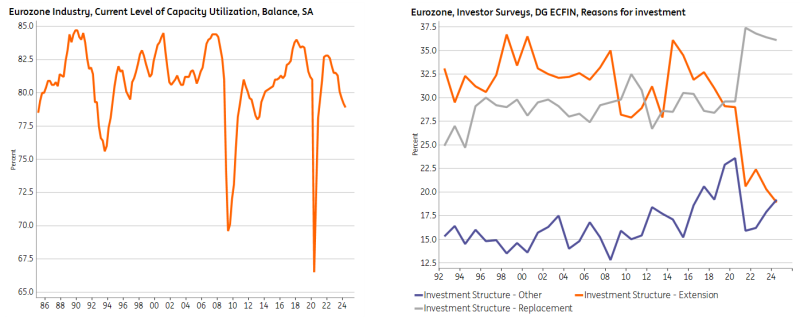

For the eurozone, weak investment seems to make more sense than in the US. The economy recovered less quickly from the pandemic and eurozone industry is going through a much larger correction than in the US. With industry being particularly capital intensive, it is easy to see why investment needs at this point are relatively low. Capacity utilisation in the eurozone has been steadily declining since the first quarter of 2022 and is currently at 78.9%, well below the historical average of 80.8%. Part of this decline can clearly be attributed to the energy crisis since the start of the Russian invasion of Ukraine.

With supply exceeding demand in capital-intensive industries, it is logical that we see very weak investment demand for expansion purposes in the eurozone. According to an annual European Commission survey, investment for extension purposes stands at the lowest level since the beginning of the survey in 1992.

Also, expectations for the near term are not necessarily very strong. Businesses remain worried about the limited potential for the eurozone economy in the near future and are not only concerned about structurally higher energy prices in the eurozone compared to the US but also about energy supply since the start of the energy crisis. This has put the brakes on investment in the eurozone.

Eurozone investment is weak due to sluggish economic performance

High interest rates create a hurdle to investing

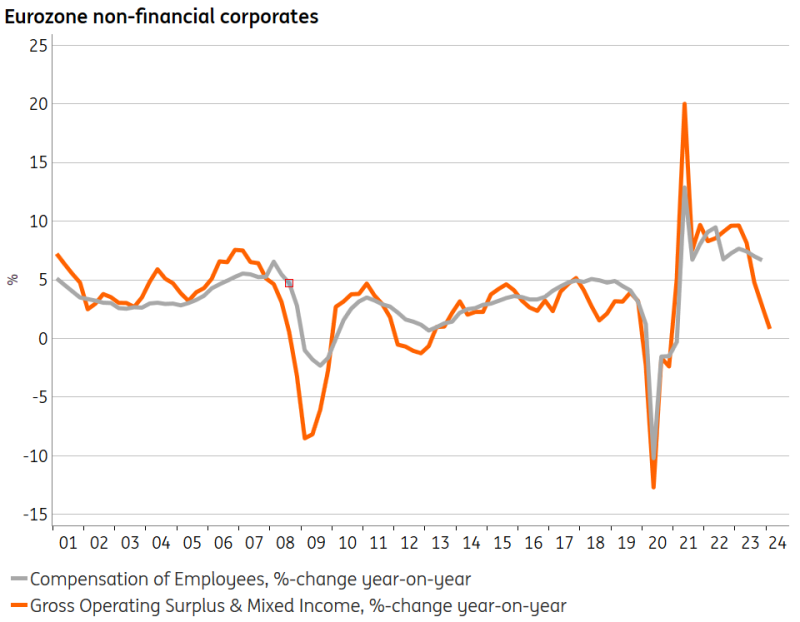

Like in the US, interest rates matter. As a driver of investment, the financial picture is currently deemed very unattractive, according to the same European Commission survey mentioned earlier. This means that while interest rates in the eurozone may be lower than in the US in absolute terms, they are still considered to be a considerable barrier to investment right now. The same can be seen when looking at reasons for bank lending, according to the European Central Bank, which indicates that high interest rates are contributing negatively to borrowing decisions. While we do expect modest declines in interest rates on the short end of the curve, we expect longer-term interest rates to remain around current levels for the foreseeable future, which means that the effects of monetary easing remain rather limited.

Still, other costs are also rising, which would lead to stronger investment requirements regardless of limited expansion opportunities. Wages, for most businesses the largest cost, have started to rise and labour shortages are large in the eurozone. So investing to replace labour with capital would be a logical consideration. Then again, during the period of particularly pressing shortages, profits were very strong. This has limited the immediate need for businesses to invest during a time of high interest rates. Wage growth in the eurozone also picked up more slowly than in the US, allowing businesses the relative luxury of waiting for a while. With profits dropping quickly at the moment and wage growth stubbornly high, some investment to substitute labour for capital could be seen in the quarters ahead.

Falling profits and stubbornly high wage growth could boost capital spending

Government investment under pressure as fiscal prudence returns

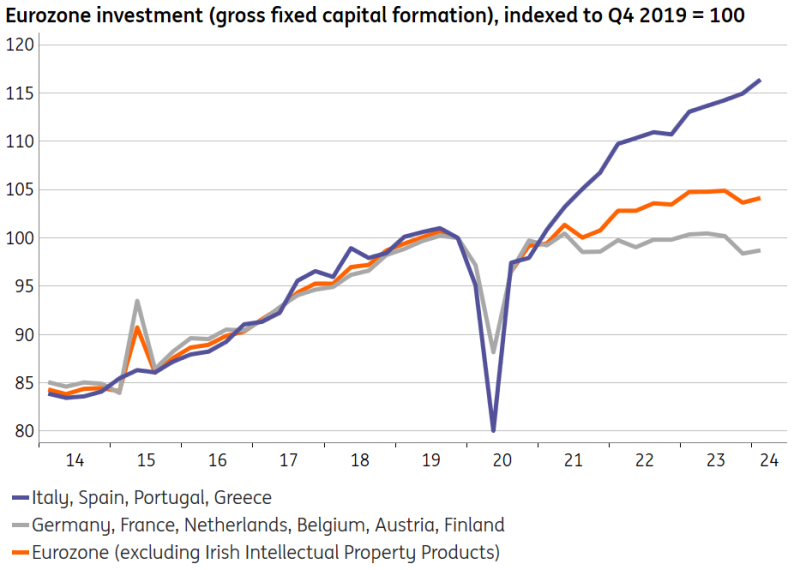

In Europe, it’s not just business investment that’s under pressure. Government investment has been recovering somewhat but spending and incentives are set to get squeezed in eurozone economies as fiscal prudence returns. While the US is still running a 6%+ budget deficit, eurozone economies are supposed to adhere to budget rules, which is reducing opportunities to boost investment. With populists gaining ground in many countries, traditional government expenditure on health and welfare will be harder to cut, which means that government investment and incentives for business investment are at risk. A logical exception seems to be defence as countries scramble to get their spending budgets in order as the Russian war in Ukraine continues. But even there, progress remains slower than hoped for in terms of increasing structural spending, and given modest European defence production capacity, orders have gone elsewhere.

This is not the case everywhere though. The EU Recovery and Resilience Fund plays an important role in funding private and public investment. In southern and eastern European countries, this is sizable, which is visible in the recovery of investment after the pandemic. Southern eurozone countries have raced ahead and are now beating their pre-pandemic trends in investment, while northern countries are driving the overall lacklustre recovery. In fairness though, a large part of this is because of the Italian “super bonus” isolation incentive scheme, which had a significant impact on investment. Through 2026, we do expect recovery fund projects to be completed, resulting in a sizable investment boost for most southern economies.

This is not the only way that governments impact investment though, policy uncertainty has increased in the eurozone with politics becoming more fragmented and traditional parties losing ground. This is the case globally of course, with protectionism on the rise, including the increasing threat of tariffs. This creates an extra hurdle to business investment.

Southern Europe has moved to a faster investment trend, in part because of the sizable EU Recovery Fund investment

Will eurozone investment catch up to the pre-pandemic trend?

Catching up to the pre-pandemic trend in the eurozone is likely going to be a challenge. With a sluggish economic outlook over the medium term, interest rates expected to remain higher than before the energy crisis, and slowing opportunities for government support, it is quite possible that a lower trend will materialise. At the same time, businesses could now start to invest in capital-labour substitution with wage growth trending higher and labour shortages still very much in play. Also, defence, energy and climate transition investment is still on the cards. The need for more investment in the eurozone is evident. However, the extent to which this investment will accelerate into a faster growth trend remains uncertain.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

EurozoneDownload

Download article

9 July 2024

Investment conundrum – why businesses are reluctant to put money to work This bundle contains 3 Articles