3 calls for the UK as political uncertainty deepens

The recent spike in gas prices for next winter doesn't bode well for the UK economy, which otherwise is benefiting from a tight jobs market and high savings levels. The risk of a technical recession later this year is rising, reducing the need for much additional tightening from the Bank of England. It comes as Boris Johnson resigns as British Prime Minister

UK economy to flirt with recession over the winter

The British Prime Minister, Boris Johnson, isn't the only one facing a crisis of confidence; so's the average British consumer. As it's announced the PM is resigning, a glance at the latest confidence numbers, which hit another all-time low last month, would ordinarily suggest a recession is inevitable. So, too, would the fact that real household incomes are set to fall by roughly 2% this year, despite fresh government support in recent weeks. However, the economy is likely to avoid a technical recession this summer.

That's partly because of an extra bank holiday last month, which will artificially boost third-quarter GDP growth. But more importantly, the jobs market remains tight.

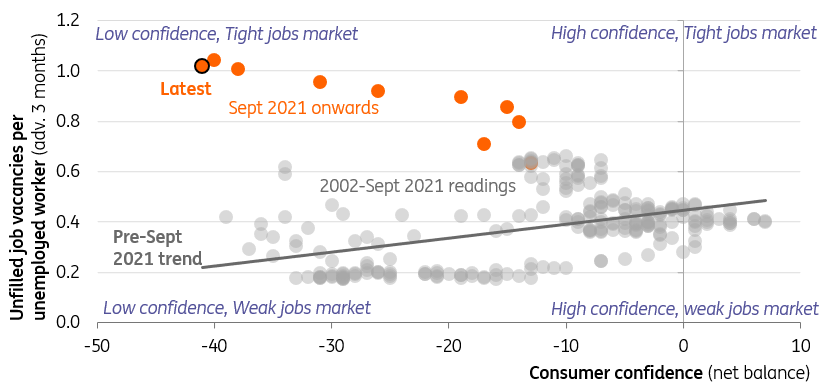

While this is undeniably a lagging indicator of economic performance, the fact that there’s one job vacancy for every unemployed worker looks to be increasingly linked to structural causes. Lower inward EU migration and elevated long-term sickness rates have prompted a stark drop in participation. Hiring demand appears to have peaked, but there’s a strong incentive for firms to keep staff on board even if margins are squeezed, given rehiring challenges.

If unemployment stays low, or only rises modestly, we suspect there will be a limit to how bad the consumer spending story can get for the time being. The chart below shows that it’s highly unusual to see such low confidence with such a tight jobs market. High household savings levels and scope for credit card borrowing to increase may also offer scope for consumers to partially smooth the income shock.

But the story is likely to get more challenging as we head into winter. The December UK natural gas contract has hit an all-time high in recent days, reaching almost 450 pence/therm, up from 250 only a matter of weeks ago and above the 400 level reached in March. That makes it more likely that the Ofgem consumer energy price cap stays flat or even goes slightly higher in the new year, even after the 55-60% increase we're now forecasting in October. If sustained, these high price levels also mean we could see more widespread demand destruction in heavy industry and much greater pressure on corporate margins generally. Like in the eurozone, there's a clear risk of a technical recession over winter.

Low consumer confidence with a tight jobs market is very unusual

Inflation to peak at 11% in October but fall back considerably in 2023

This latest rise in gas prices, coupled with the prospect of 15-20% food inflation, means headline CPI is likely to hit 11% in October. By that point, energy alone will be contributing more than five percentage points, and food almost two. But some other recent sources of price pressures appear to be cooling, and in fact core inflation – currently around 6% – may be roughly at its peak.

Like in the US, headline inflation is likely to drop like a stone in 2023 – especially beyond April, the one-year anniversary of the first huge electricity price increase. By the end of next year, both food and energy are likely to be a slight drag on inflation and we think headline CPI can still fall a little below target, crazy as that currently sounds.

Bank of England set to underdeliver on market hike expectations

Mounting recession fears have already seen markets pare back expectations for Bank Rate next year, with the peak now seen in the 2.9% area, down from over 3.5%. That's arguably still too high, though in the short-term we think the combination of a weaker pound and aggressive Fed action will lead the committee to hike by 50 basis points in August. That would take us into what's arguably neutral interest rate territory (probably around 2%), potentially negating the need for further 50bp moves. We expect rates to peak at around 2%.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

7 July 2022

ING Monthly: Europe’s recovery is cancelled This bundle contains 14 Articles