THINK Ahead: Europe loves a lever, and has plenty of pulling power

Markets ended April in a remarkable place, don't you think? Investors are banking on Fed rate cuts, tax cuts and tariff reductions to keep things afloat. That might prove naive, says James Smith. But he does argue that Europe has more levers to pull to keep a downturn at bay. And next week, here come the central banks…

How Europe is better placed to deal with Trump's tariff storm

Here’s a mind-blowing statistic: April saw the smallest monthly change in the S&P 500 in almost two years. It fell by just 0.8% between the start and the end of last month. Ten-year US government bond yields, meanwhile, were down just six basis points.

If only April could have been more exciting, guys?

Yes, yes, obviously I am cherry-picking dates here; heaven forbid an economist would do such a thing. Those figures do slightly gloss over the 12% 'peak-to-trough' and subsequent dip to recovery in the stock market. And best we don’t talk about what happened to the dollar…

Still, markets are in a remarkable place, all things considered. Investors aren’t exactly jubilant. But it feels like they’re increasingly concluding the US economy can avoid a full-blown recession through a combination of swift Fed easing, tax cuts and a reduction in US-China tariffs.

I don’t know about you, but I can already see a few holes in that. And our man in New York, James Knightley, agrees.

Take those tax cuts. James is sceptical that the deficit hawks in Congress will permit much over and above the extension of the 2017 tax cuts. The President’s touted giveaways on overtime and pensions probably won’t make the cut. Remember that tax cut extensions do nothing for disposable incomes. And any genuinely new tax cuts probably won’t show up in the economy before 2026.

As for tariffs, it feels like a climb-down might be in the offing where China's concerned. The mood music is improving, anyway. You can see the makings of a potential off-ramp for both sides to de-escalate without losing face.

But simply reducing China tariffs to the 60% area, as recent reports have hinted at, still presumably means a large chunk of imports will be uneconomical. And unless a climbdown happens imminently, the supply chain damage could be sizeable. With trade volumes already visibly falling at the major West Coast ports, maybe it’s already too late.

We’ll soon find out, but don’t assume the Fed will quickly step in and save the day. Markets are pricing 30bp of easing by the time of the July meeting. That's eminently possible, even if it's a little hard to square with the Fed’s very visible concern about the inflationary impact of tariffs, which we’d expect to be on full display at next week’s meeting.

Inflation is set to rise more quickly than the economic data turns weaker. Jobs growth is holding up for now, anyway. And James K argues this could mean no Fed cuts before September.

Interestingly, though, he thinks if the Fed were to wait that long, it might have to cut big. Waiting until payrolls numbers turn more sober is a risky business, given employment data is famously backwards-looking. It implies the Fed could end up behind the curve.

Sensing a bit of déjà vu? That’s because it sounds remarkably similar to last summer, where weaker jobs numbers forced the Fed into a 50bp cut last September. The recession scare was a false alarm back then, and risk assets subsequently rallied. The same might not be true this time around.

Let’s not exaggerate, though. James is still a bit reluctant to call an outright recession, even if he is getting more nervous. Neither is he calling for the Fed to cut rates below 3%, which is what markets are now pricing.

But our point is that if markets expect fiscal and monetary policy to rescue things rapidly, they are likely to be disappointed.

The opposite is true over here in Europe. Governments are splashing the cash, and though that won’t show through immediately, our team thinks it will become a powerful force by 2026. In the meantime, the European Central Bank is much freer to keep cutting rates than the Fed, with inflation looking much more benign.

It’s a similar story in the UK. The government is also spending big this year, though the inflation outlook is admittedly a bit trickier. Services inflation is proving sticky, though we’re more optimistic about that than the Bank of England seems to be. A rate cut next week is a no-brainer. And two more are likely to follow later this year. There’s plenty of scope to cut much further if things do go pear-shaped with tariffs.

Europe still faces plenty of headwinds. But at least has levers it can pull to insulate against a tariff-driven recession. The US might not be so lucky.

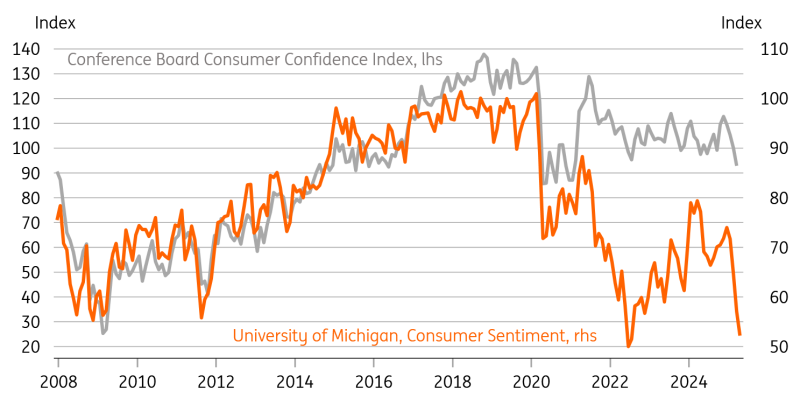

Chart of the week: US consumer confidence is falling fast

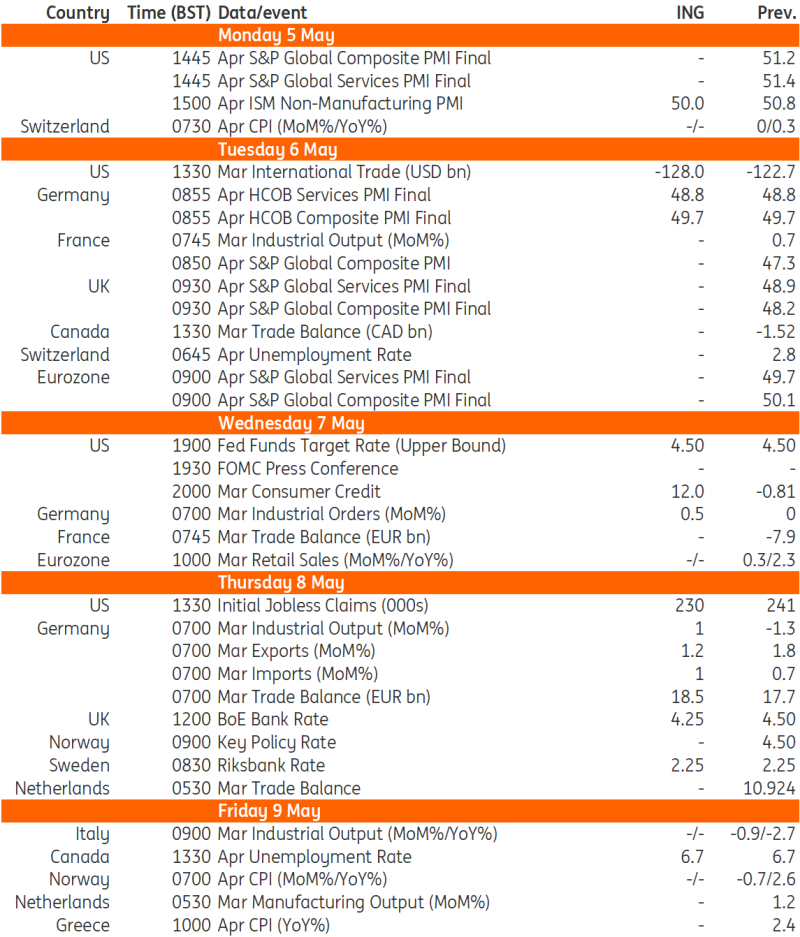

THINK Ahead in developed markets

United States (James Knightley)

- Federal Reserve (Wed): The President and his Administration continue to pressure the Fed to cut interest rates but that will fall on deaf ears again next week with monetary policy set be left unchanged. In his most recent comments Fed Chair Jay Powell warned that the US can't have a strong labor market without price stability, stating that “our obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem”. This suggests little prospect of a near-term interest rate cut.

- Fed Governor Chris Waller was more explicit suggesting a move is unlikely at the May or June FOMC meetings, arguing that with the 90 day pause on reciprocal tariffs “I don’t think you’re going to see enough happen in the real data in the next couple of months, until you get past July”.

- ISM Services index (Mon): There's a very real risk this dips into contraction territory, which would underscore the sense that the economy is cooling and recession is a realistic possibility.

United Kingdom (James Smith)

- Bank of England (Thurs): We expect a 25bp rate cut, but we'd be surprised to see the Bank turning more dovish generally. Tariffs aren't as much of a headache as in other parts of Europe, while services inflation is proving stubborn. That could change as we head into summer, but more now we expect the BoE to simply reiterate that future cuts will be "gradual". Read our full preview

Sweden (James Smith

- Riksbank (Thurs): Policymakers have said they don't expect to cut rates any further and we don't expect any change next week. However, if the ECB continues to cut to below 2%, then we think we could get one extra cut out of the Riksbank in June. Read our full preview

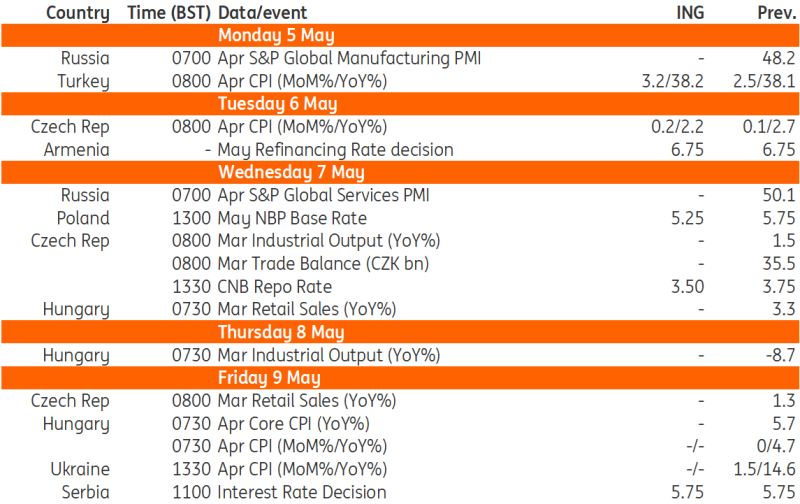

THINK Ahead for Central and Eastern Europe

Poland (Adam Antoniak)

- NBP rate (Wed): The substantial decline in April's inflation, moderating wage growth and softer economic data give the Monetary Policy Council (MPC) room to ease monetary policy this month. Will it be a 50bp or 25bp cut? We lean towards the former, however, it may be accompanied by a less dovish post-meeting press release designed to help cool market expectations. Investors are pricing 150bps of rate cuts in the next three months. We expect a pause in June and further policy actions in July, when the NBP staff will prepare updated macroeconomic projections.

Czech Republic (Frantisek Taborsky)

- Inflation (Tue): Inflation in April probably fell to 2.2% YoY, driven by lower fuel prices and movements in USD/CZK. Recreation should also show some seasonal downward movement, though food prices continue to rise and other items are showing some upside as well. The upside risk, in our view, is housing prices.

- CNB rate (Wed): The May decision will depend on those inflation figures, but we expect a 25bp rate cut accompanied by a hawkish tone and some votes for a pause. However, an upside inflation surprise would mean another pause in the cutting cycle. Overall, the CNB's new forecast will have mixed revisions but suggest inflationary upside risk.

Turkey (Muhammet Mercan)

- Inflation (Mon): In addition to FX pass-through impact especially on core goods, April inflation will reflect a 25% electricity price hike for households and the effect of agriculture frost on fresh fruits and vegetables prices. Accordingly, we see monthly inflation at 3.2% MoM, translating into a slight increase in annual inflation to 38.2% YoY.

Armenia (Dmitry Dolgin)

- Interest rates (Tue): We expect the central bank to keep the key rate at 6.75%, rather than opting for a modest cut, given the generally cautious mood surrounding inflation risks and capital account considerations in the region amid global trade tensions. Additionally, the fiscal deficit of circa 3% GDP, as well as fast and accelerating domestic lending growth of 27-31% YoY, with funding growth lagging in a 13-24% YoY range, could serve as domestic pro-inflationary risks. A cut can't be fully ruled out, given the overall CPI rate was 3.3% YoY in March, close to the long-term target of 3%, and the data for April would be available only on the day of the central bank decision, adding to the uncertainties.

Key events in developed markets next week

Key events in EMEA next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article