The system: Holding up but vulnerable

The rapid tightening of monetary policy and significant outlook uncertainty is straining the system and testing the markets' capacity to absorb risks. The UK has shown how sketchy market liquidity can quickly lead to a solvency issue. Central bank ambitions to tighten could be frustrated if confronted with material pressure on the system

The financial system is vulnerable amid deteriorating market liquidity

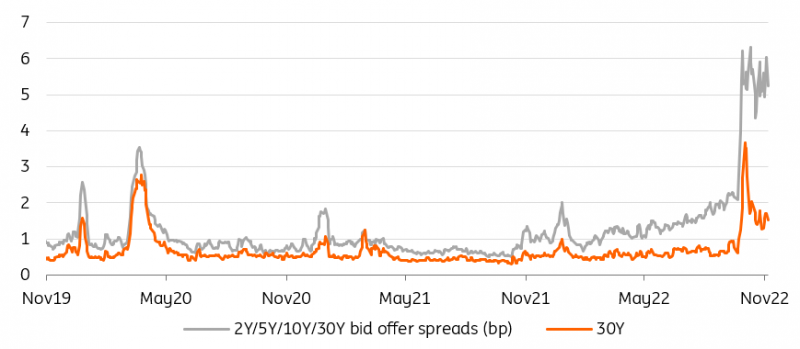

As we approach the start of a new year, markets remain in a fragile state. At its foundation is the issue of market liquidity. Many of the common indicators of market liquidity are now at worse levels than they were at the peak of the Covid-19 pandemic. Take bid-offer spreads for government bonds, the go-to safe and supposedly most liquid of assets, which still reside at exceptionally wide levels. High realised and implied market volatility, while also an effect of central banks moving into action and a sign of the uncertainty surrounding the outlook, are straining the market’s capacity to absorb risk and lead to higher costs for market making.

Wider gilt bid-offer spreads show that markets are increasingly dysfunctional

A liquidity problem can quickly morph into a solvency issue. This is what the UK recently experienced when the government’s expansionary fiscal plans sent shockwaves through gilt markets. Fears of higher issuance and a more hawkish Bank of England (BoE) reaction sent rates higher, but it was the pension funds' leveraged positions and ensuing margin calls that led to the situation spiralling out of control, eventually forcing the BoE to step in with purchases of long-end gilts, as well as forcing it to revisit fiscal plans.

From home grown risks ...

On the back of the UK experience, the fiscal factor has received more attention as a potential trigger of market moves that could eventually put market liquidity to the test. The initial impact on rates can work via the sheer supply and credit channel, but currently also via the anticipated central bank response if the fiscal developments are seen to have a clear inflationary effect.

A fiscal trigger for sudden moves may look less likely in the euro area and US political setups ...

Substantial government programmes to support economies in light of surging energy prices have been set up or at least flagged in the euro area. One would think that the political decision process in the euro area – as well as in the US – as an aggregate makes the central bank response channel a trigger for sudden repricing less likely than what was witnessed in the UK. But if the economic slump deepens and another winter with potentially limited energy supply looms, one cannot exclude markets starting to focus on fiscal sustainability again.

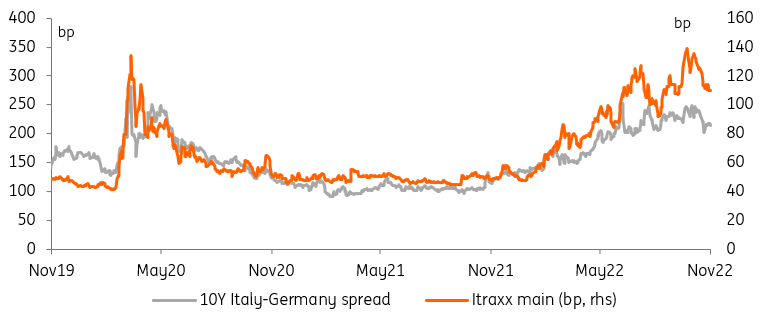

Euro sovereign spreads remain a cause for concern, but are holding up better than expected

This happens against the backdrop of central banks running down their balance sheets, leading to an increased net government debt supply that private investors will have to absorb. The Federal Reserve has been in the process of quantitative tightening (QT) for some time, the BoE just started this November – with the notable hiccup in gilt markets surrounding the pension funds – and the European Central Bank (ECB) is slated to begin in 2023.

... but sovereign debt crisis fears still linger amid ECB quantitative tightening

It seems obvious to look at government bond auction metrics which have already suffered, though those are also a reflection of a limited desire for duration risk rather than the credit itself. However, with a view to the eurozone and its experience of the 2012 sovereign debt crisis burnt into collective memory, it is not too hard to imagine how a combination of political choices and geopolitical events could again sour investor confidence. The ECB has put in place a backstop – the Transmission Protection Mechanism – but being tied to conditionalities, its effectiveness could be blunted.

... to outside triggers

Of the outside factors that could put the financial system’s capabilities to the test, geopolitical risks are one of the more obvious given the ongoing conflict in Ukraine. A sudden escalation, and in particular an immediate impact on energy prices, could put central banks in a tough spot as their inflation goals move further into the distance, requiring more forceful action while the economic backdrop takes a heavy blow, further straining public and private finances.

One of the outside risk factors, however, relates to the policies of the Bank of Japan (BoJ) which so far has been an outlier amid the global charge of central banks tightening their policy reins. Importantly, the BoJ is conducting purchases at the long end of the Japanese government bond curve to cap yields. Any sign of the BoJ yield curve control ending could have large knock-on effects on yields outside of Japan. It could trigger another large and potentially sudden hike in global bond yields. Markets are already eying the end of the current BoJ governor’s (Haruhiko Kuroda) term in April 2023.

Stable markets are no longer an argument for owning fixed income

Suppression of money market risks about to fade

Money markets can be viewed as the plumbing of financial markets, which is also the reason why we have seen central banks acting quickly to intervene here in the past. We are still seeing the effects of this in the high levels of excess reserves within the banking system and the compression of money market spreads.

The blanket provision of excess reserves is no longer compatible with the goal of tackling inflation

But this suppression of risks is bound to be scaled back as the blanket provision of excess reserves is no longer seen as compatible with the broader policy goal of tackling inflation. Markets are left more susceptible to credit events or sudden dashes for liquidity.

For instance, the term funding provided to banks by the ECB via the targeted longer-term refinancing operations (TLTROs) and the excess of reserves flooding the system has led to a compression of Euribor rates over the risk-free 3m ESTR swap, a spread that has traditionally served as a measure of risks embedded in the banking system. In the United States, one indicator that we like to monitor is where banks print 3-month commercial paper as a spread over the risk-free rate (3mth term SOFR). It’s a simple measure of how easy it is for banks to fund themselves in the short-term market. Currently, this spread is at around 30bp (and European banks are printing at 50-60bp). That’s far wider than it was, but not yet enough to cause any material consternation.

The scaling back of central bank support is adding to the uncertainty investors are already facing as markets are perceived to be more prone to the materialisation of systemic risks, and the UK is considered a warning shot.

The implication should be that risk measures can stay elevated or may even have to rise further. The above are only a selection, but it is especially relevant to monitor systemic risk measures while central banks are still tightening policies, in the sense that ambitions to do so will be frustrated if confronted with material negative pressure on the system. Anything that threatens to take the system down, or to risk doing so, is therefore out of the question.

It’s also relevant as we progress through the 2023 slowdown/recession period, as any deep recession can pressure the system, as defaults can rocket. In that sense, it can act to accelerate a transition back to interest rate cuts.

As such systemic risks could be a more credible reason for a “material pivot” than recessionary fears. After all, tighter policies from central banks are designed to slow growth and tend to accept the risk of recession. But what central banks can’t accept is any threat to the functioning of the system. No need to panic yet, but this is what we really need to be cognisant of.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

Rates outlookDownload

Download article

10 November 2022

Rates Outlook 2023: Belt up, we’re going down This bundle contains 9 Articles