The ripple effects of soaring energy prices

- 17 February 2022

- Commodities, Food & Agri Energy Transport & Logistics Manufacturing, Construction and Retail

The effects of soaring energy prices are felt by many sectors. Aviation, shipping and the chemical industry are directly impacted by higher energy prices. The food industry, travel agencies and hospitality are impacted by second-round effects. A firm’s resilience depends on its profit margin and ability to pass through price hikes

Energy prices went through the roof in 2021 and are expected to stay high in 2022

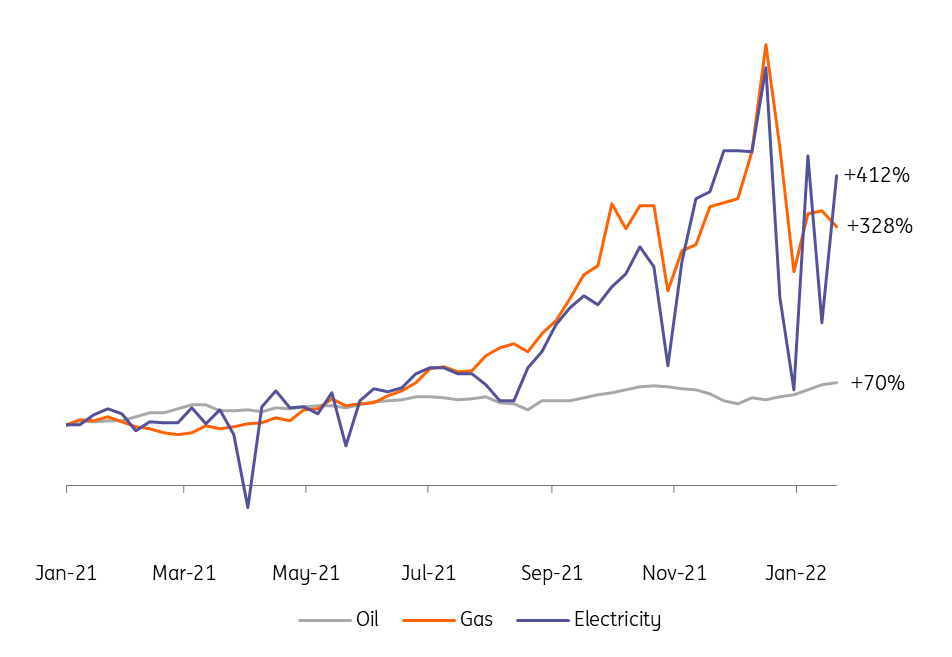

European energy markets became very tight and volatile over the course of 2021. Power prices quadrupled, gas prices tripled and oil prices almost doubled. By mid-December, at the peak, gas and power prices had risen sevenfold, reaching unprecedented levels. Unfortunately, there is no quick fix for high energy prices and we expect energy markets to remain tight in 2022.

Power prices quadrupled, gas prices tripled and oil prices almost doubled in 2021

Index of weekly power price (German baseload), gas price (Dutch TTF) and oil price (brent oil), January 2021 to January 2022

Duration matters: first- versus second-round impact of higher energy prices

Higher energy prices can impact companies in many ways. The immediate impact is through higher costs from rising energy prices (first-round impact).

If higher energy prices are sustained, they can (with a delay) result in second-round effects. Energy-intensive companies can pass on higher energy prices to their clients. As a result, they too are confronted with higher costs. Production of energy-intensive products could also become unprofitable at high energy prices. Producers might lower production levels which could create shortages further up the supply chain.

In this article, we look at the impact of higher energy prices on companies in different sectors, in terms of both first- and second-round price effects.

Sectors are impacted differently by higher energy prices

The impact of high energy prices differs based on the sector and the amount and type of energy they use. Aviation and shipping, for example, are the most energy-intensive sectors. But aeroplanes and cars primarily use oil products where the price has gone up much less compared to gas and power.

Highest first-round effects in aviation and shipping

Most industrial sectors are energy-intensive, too, and rely more on gas and power for heating and feedstock, where prices have skyrocketed. There are also sectors that are less energy-intensive such as construction, trade and the automotive industry. Despite the energy intensity and fuel mix, all these sectors are impacted by rising energy prices.

High energy use aviation, shipping and chemical industry

Use of terrajoule energy per € 1 million Value added output, EU-27 in 2018*

Second-round effects could be substantial in the food & rubber industry, for travel agencies and hospitality

Direct users of oil, gas and power are not the only ones dealing with soaring energy prices. High energy users will, to varying degrees, pass on the effects of price hikes, albeit with some delay.

For instance, the food and beverage industry procures many products from agriculture. If farmers have to increase their prices due to higher energy costs, the food industry has to deal with this as well.

Travel agencies also purchase a lot from energy-intensive sectors like aviation and road transport. They are faced with more expensive plane tickets when airline carriers are forced to increase ticket prices due to more expensive kerosine.

Second-round effects of high energy prices are largest in food & beverage industry

Procurement from very energy-intensive sectors (see graph above) as a share of total production, 2018*

High energy use doesn’t mean high vulnerability

Sectors that use a lot of energy are not by definition hit hard by rising energy prices. The impact depends on their profit margins and the ability to pass on price increases to clients.

Market power is, therefore, an important factor. Below we discuss how this works for different markets and sectors based on calculations using Dutch sector data, as the Netherlands is one of the few countries which has this data available. We expect similar results in other countries, too.

The results of this analysis are found in the graph below. The vertical axis represents the volatility of all the sector input prices (so not only energy prices). The horizontal axis embodies the variation of the profit margin.

Sectors vary in the degree to which volatile input prices impact profit margins

Sector development in The Netherlands, 1997-2020*

Steady input prices and profit margins in retail, wholesale and healthcare

In the left corner (Quadrant III) we find sectors that aren’t much exposed to procurement price shocks. Consequently, their profit margins are stable as they aren’t faced regularly with price increases. In this quadrant we find the sectors, retail, healthcare, wholesale and construction. We have seen that these two last sectors are vulnerable to second-rounds effects but historic data reveals they are marginal.

Energy price hikes and market power results in lower profit margins in automotive, the cement industry and travel

High profit margins are a cushion for higher procurement prices. It is often thought that market power gives companies the opportunity to pass through higher input prices. However, this is not the case in general. Often, these firms have already increased their sales prices to the maximum price that clients are able (or willing) to pay. They can’t therefore increase their prices further without losing sales. Consequently, higher energy prices will harm the high profit margins of these companies with market power.

This is the case for many firms in the sectors in Quadrant II of the graph. For instance, building material companies of concrete, cement and bricks operate in a small local market. This is due to the characteristics of these materials. They are large and heavy and therefore difficult and costly to transport. This makes these local markets less competitive. The pass-through of energy price fluctuations is therefore slower as these companies already have high output prices. Appreciating energy prices will therefore be mainly absorbed by a drop in the profit margin.

Energy price hikes in competitive markets lead to cost pass through

In general, sectors with high competition will have firms with lower profit margins due to price battles in these markets. What will happen in these markets when companies are confronted with higher costs from soaring energy prices?

Due to the low profit margins, firms in these markets aren’t able to swallow the higher procurement prices, otherwise, they will be loss-making and in a worst-case scenario could potentially go bankrupt. There will be severe price negotiations and in some cases, suppliers might stop or threaten to stop delivering for a while, but eventually and in general the price will go up. So these companies don’t have a huge profit cushion but they can pass through higher procurement prices. The market output price will go up because all competitors are facing the same problem. These sectors are found in Quadrant IV, for example, the food industry and road transport.

Qualitative model of price pass through effects

High price vulnerability and roller coaster profits in aviation and basic metal industry

In Quadrant I, we find aviation and the basic metals industry. These sectors face high, volatile input prices and profit margins. The extreme energy intensity (see first graph) and the homogeneous product that is delivered in these sectors make it very hard to react to energy price fluctuations.

How companies can cope with energy price risks

As profit margins are often thin and many sectors are energy-intensive, firms have to closely follow oil, gas and power prices. There are several strategies that companies can follow to mitigate price fluctuations. All of them have their pros and cons and most companies make use of a combination of these strategies. Therefore, we should point out that the exposure, risk appetite and market situation for every single company is different:

Minimise energy use: By using energy-efficient production processes, the amount of energy will be diminished and the vulnerability to energy price hikes will diminish. Air carriers can for instance invest in more energy-efficient aeroplanes. This strategy however takes time and is less suitable to accommodate the immediate impact of high energy prices.

Use a price escalation clause: This makes it possible for firms to pass on energy price increases to the customer. This is mainly done in B2B markets. Price clauses with private consumers (B2C) are more difficult to achieve and therefore not common.

Directly procure inputs: Firms can directly procure oil, gas or power at the moment a sales deal is closed. This secures the calculated energy price at the moment of closing the deal. They can do this in two ways. First, they can agree on the price with a supplier and ensure delivery of the fuel at the moment needed in the production process. However, it must be said that suppliers are sometimes reluctant to lock in such long term contracts as the price risk is handed over to them. Second, firms can buy the needed energy directly, have it delivered directly and stored until needed. Yet, this results in (high) storage costs and a decrease in working capital.

Commodity futures: If the above strategies are not possible, a hedge with a commodity future is an option. However, futures are complicated financial products which have to be fully understood and constantly monitored.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more