The reasons behind Europe’s productivity problem, and how to solve it

- 30 April

The productivity gap between the US and the eurozone is widening. Weaker productivity growth within sectors and a shift of labour towards low‑productivity activities continue to weigh on growth. While wider adoption of artificial intelligence (AI) could lift productivity, a return to the pre‑pandemic annual growth rate of 0.7% appears unlikely

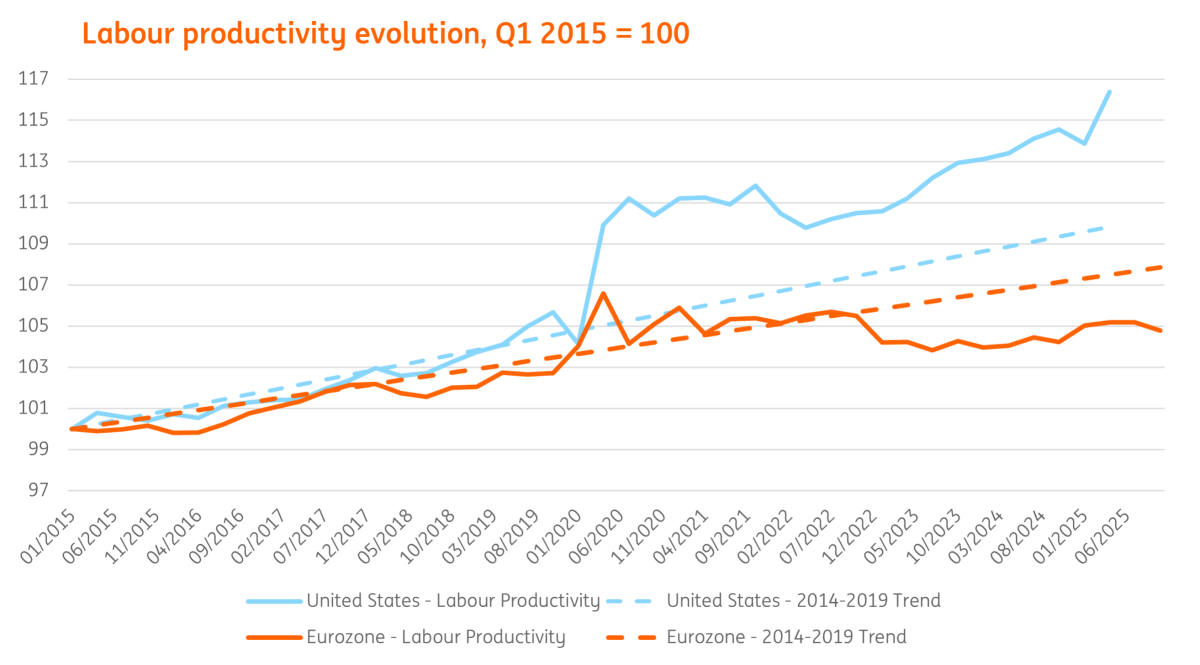

US productivity pulls decisively ahead of the eurozone

As we discussed in a previous article, eurozone GDP growth has increasingly been held back by weak labour productivity growth. What stands out is not just the recent softness, but a long‑running slowdown that has been far more pronounced in Europe than in the US.

In 1995, output per hour, measured in Purchasing Power Parity‑adjusted dollars, was virtually identical on both sides of the Atlantic. By 2019, however, the eurozone was already lagging the US by 18%, according to an ECB study. Since then, the gap has widened further, as eurozone productivity decelerated sharply relative to its pre‑pandemic trend at the end of 2025, while US productivity growth is accelerating.

US labour productivity accelerates while eurozone productivity stagnates

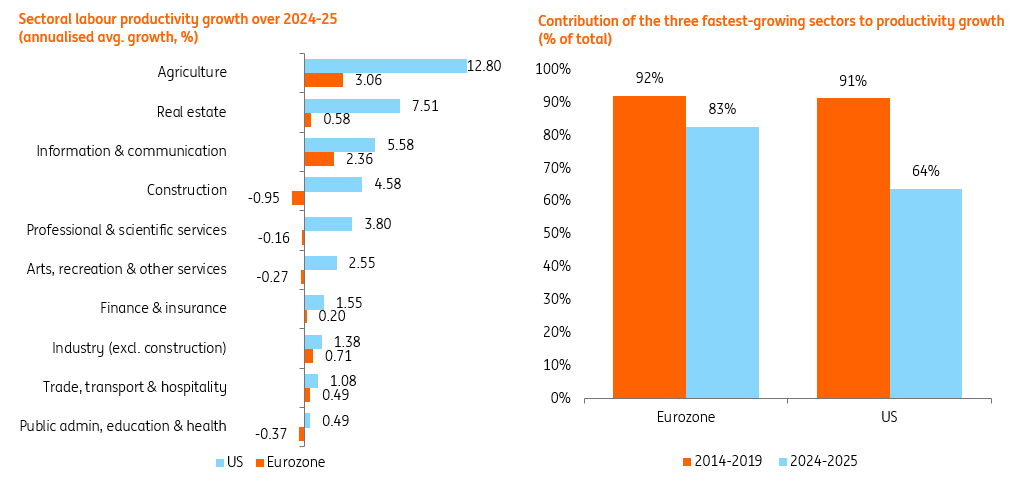

Average productivity hides large sectoral differences

Of course, average labour productivity per hour can hide important underlying dynamics. Average productivity growth can be seen as coming from two sources: firms becoming more efficient within sectors (with changes in economically larger sectors being more important for overall productivity growth), and workers moving into sectors where productivity is higher.

Within sectors, recent data reveal large differences in labour productivity growth between the US and the eurozone. In the US, productivity gains have been broad‑based and particularly strong in agriculture, real estate, and information and communication services, while eurozone productivity growth has been much weaker and, in some cases, negative. Moreover, whereas during 2014-19 the three fastest‑growing sectors accounted for around 90% of total productivity growth in both economies, this share has since fallen to about 64% in the US, pointing to a more broad‑based and widely shared productivity expansion in recent quarters as a key driver of the growing productivity divergence between the eurozone and the US.

Even within sectors, eurozone productivity growth lags

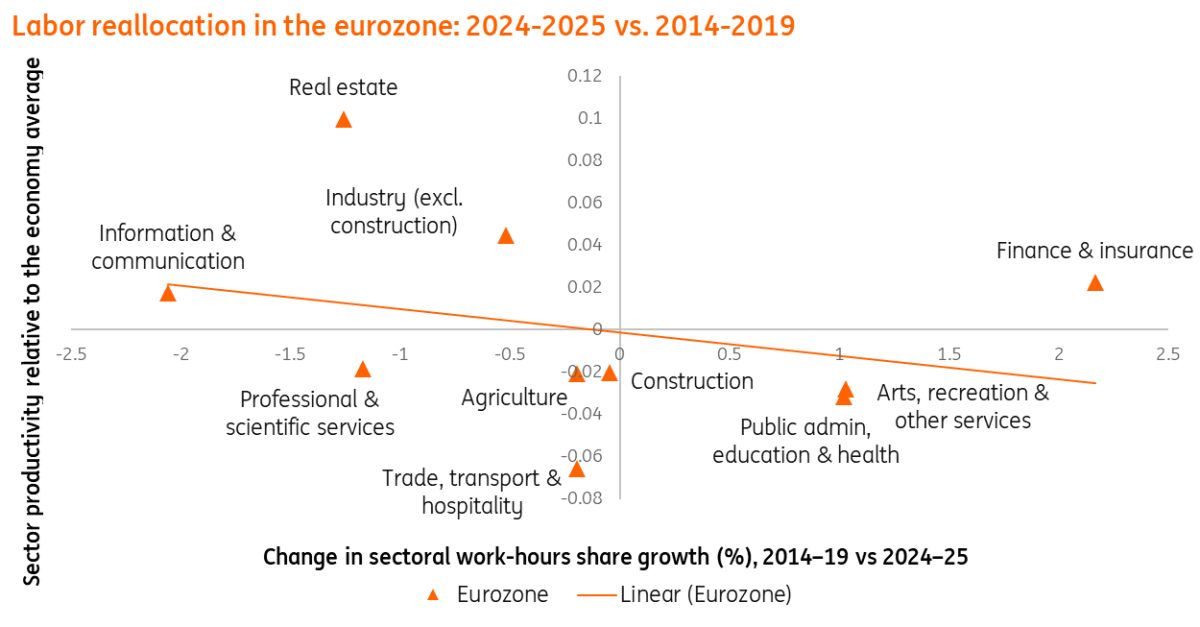

Labour reallocation is amplifying Europe’s productivity slowdown

Labour reallocation has further weakened aggregate productivity growth in the eurozone in recent years. Compared with 2014-19, employment has increasingly shifted towards services such as public administration, education and health, where productivity growth is structurally more limited, while higher‑productivity sectors like industry have lost employment share. This pattern is consistent with what economists call Baumol’s cost disease: as productivity rises faster in some parts of the economy than in others, labour and spending tend to move towards slower‑productivity services, mechanically dragging down overall productivity growth.

Labour in the eurozone increasingly shifts towards less productive sectors

AI offers long‑term potential, but has yet to lift eurozone productivity

Of course, Europe is not doomed to remain stuck in a slow productivity and subsequent subdued growth environment. AI represents a significant opportunity to enhance productivity in the future. A study from the Kansas City Fed shows that, in the US, higher AI adoption correlates with faster productivity growth across industries. Notably, progress has thus far been driven by a limited number of high-impact sectors, suggesting that the AI trend is still in the phase of broadening.

Across most metrics, such as the development or hosting of AI models, Europe lags significantly behind both the US and China. While some analysts argue that the speed of adoption matters more for future productivity than where the technology is developed, US data indicates that (physical) distance from AI innovation influences how quickly and effectively AI is integrated into other sectors and business processes. Moreover, approximately 40% of the aggregate effect of AI on productivity growth is actually related to the development of AI itself in the ICT sector, underscoring the importance of native AI capabilities; the limited availability of locally developed AI models is therefore constraining Europe’s overall productivity improvement. Reliance on foreign technologies also entails risks in a more fragmented global landscape, and cultural differences may impede the effectiveness of AI solutions developed abroad.

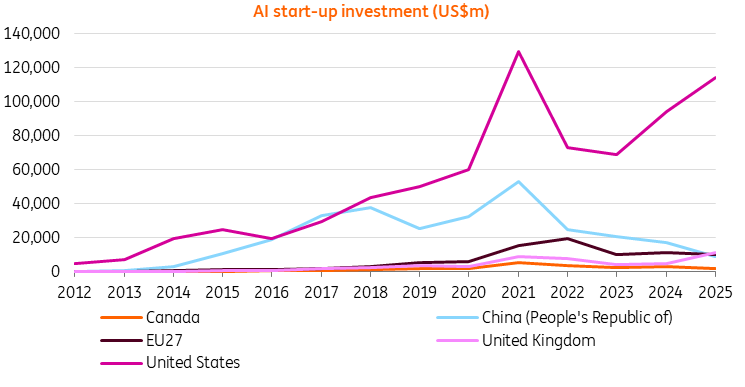

These structural disadvantages are also reflected in investment data, which show that Europe remains at a much earlier stage in the AI development cycle than the US and China. According to data from the OECD AI observatory, AI startup investments in the US were approximately 11 times bigger than those in the EU in 2025. The 2026 AI index report similarly highlights how Europe is falling behind the US and China in overall AI investment.

Europe lags the US and China in AI investment

A modest pick-up in productivity growth is feasible

In summary, the US has experienced a phase of accelerating labour productivity growth in recent years, whereas the eurozone saw declining productivity growth in 2024-25 compared to the pre-pandemic period of 2014-19. Productivity growth has stagnated or decreased across most sectors, compounded by a shift in labour force allocation from more productive to less productive industries. AI presents an opportunity to improve sectoral labour productivity growth, yet regulatory constraints, rigid labour markets, and the scarcity of indigenous AI models may temper these benefits. Cecilia Jona-Lasinio estimates AI has the potential to boost labour productivity growth by up to 1.0 percentage points in the US and 0.3 percentage points in Europe. The figure for Europe is in the ballpark of what we have estimated before, though for the US it is actually higher in Jona-Lasinio’s model.

Another approach to enhancing labour productivity in Europe and the eurozone would be to counteract the Baumol effect, namely, by reallocating labour from less productive to more productive sectors. However, this remains challenging in ageing societies, where sectors such as healthcare continue to gain in importance. Consequently, efforts should prioritise increasing productivity within individual sectors, including non-market areas (think of e-government, AI in health care, …). This strategy could contribute to rising eurozone productivity in the coming years, though a return to the annual average growth rate of 0.7% observed between 2014 and 2019 appears unlikely.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more