Hungary’s labour market cools slightly

The cost of living crisis has not gone completely unnoticed in employment statistics, with labour metrics cooling slightly in the autumn. However, the labour market still remains tight, which also puts upward pressure on wage growth

| 4.3% |

Unemployment rate (Aug-Oct)ING Forecast 4.0% / Previous 4.1% |

| Worse than expected | |

There has been a slight increase in the unemployment rate

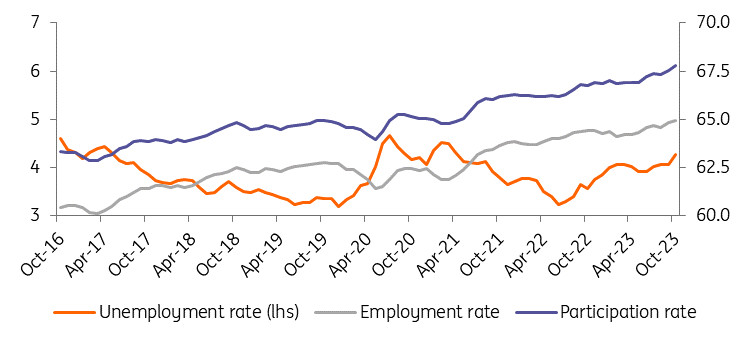

According to the latest unemployment statistics published by the Hungarian Central Statistical Office (HCSO), there was little change in the labour market in October. The model estimate for the tenth month of the year showed a slight deterioration in the unemployment rate (4.1%). Meanwhile, the official three-month moving average of this labour metric (based on a survey) rose by a similar 0.2ppt to 4.3%. Against this backdrop, the number of people out of work has once again risen meaningfully above 200,000, a level not seen since March 2021.

Looking at the longer-term trend, the cost of living crisis has not gone completely unnoticed in the labour market. Apart from a (seasonal) improvement this summer, there has been a slow, trend-like deterioration in the unemployment rate since spring 2022. However, it is important to note that both the activity rate and the employment rate in the labour market have increased significantly over the same period. In other words, more and more people want to work as a result of the impact of the crisis on their livelihoods, and they have been absorbed to a significant extent, but not entirely, by the labour market.

Historical trends in the Hungarian labour market (%, 3m moving average)

Looking at the monthly data, perhaps the most important change is that the number of people in employment rose by around 10,000, while the number of people unemployed rose by 11,000 and the number of people without a job by just under 2,000. On the one hand, these changes are within the margin of error, i.e. they are not significant. On the other hand, they suggest that more people are entering the labour market as the year draws to a close, but that finding a job is not as easy as it was a year ago.

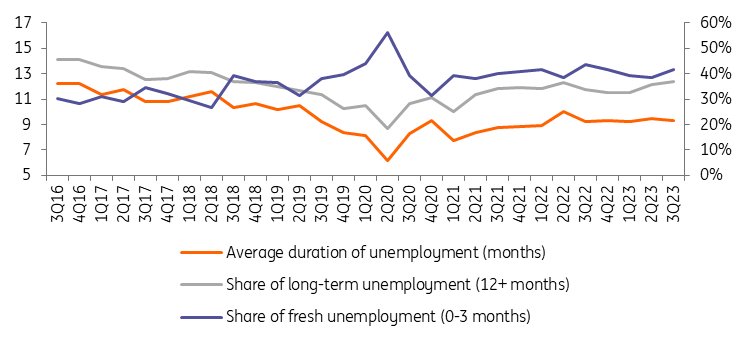

Compared to the beginning of 2023, there has been a significant increase in the proportion of people who have been unemployed for 0-3 months (i.e. either recently lost their job or recently returned to the job search), although there has also been an increase in the number of long-term unemployed who have been out of work for more than a year. The hiring propensity of companies thus appears to be easing significantly in the overall economy. Nevertheless, considering the cost of living crisis, we can conclude that the Hungarian labour market remains in good shape and labour shortages remain significant.

Unemployment by job search duration

Going forward, we do not calculate for any structural changes in the labour market for the rest of the year. The vast majority of companies will continue to insist on retaining staff, having learned from the shocks of recent years that it is quite difficult to expand the workforce in a recovery period in an economy with a structural shortage of labour. In this regard, judging by the latest third-quarter GDP data, the Hungarian economy is on the verge of recovery.

The structural labour shortage can raise workers’ bargaining power and therefore support wage increases, especially in light of the recent minimum wage agreement. Positive real wages may support the economic recovery, but they also carry reflationary risks. For the time being, we believe that the corporate costs of the expected real wage increase can be covered by expected revenue growth and efficiency gains, so that while the risk of a price-wage spiral remains, we see a good chance that it can be avoided.

| 14.1% |

Gross earnings growthING Forecast 14.1% / Previous 15.2% |

| As expected | |

Slowdown in average gross earnings on the back of base effects

According to the latest wage statistics published by the HCSO, the pace of year-on-year (YoY) average wage growth in Hungary slowed slightly in September. On the one hand, the 14.1% YoY average wage growth (for the full range of employers) can still be considered very strong. On the other, the slowdown in wage dynamics compared with the pace observed in recent months is due to a strong base effect, as salaries of professional members of law enforcement agencies increased significantly in September.

Nominal and real wage growth (% YoY)

Meanwhile, regular earnings in September were 14.9% higher than a year earlier, which means that the increase in total earnings (including bonuses and one-off payments) is higher than the increase in average earnings. This also means that one-off payments and bonuses were lower in September this year than a year ago. Again, this should come as no surprise, as at the end of last year, with inflationary pressures rising, many companies decided to give their employees one-off payments. The aim was to improve the financial situation of workers without imposing a long-term increase in wage costs on firms.

It is therefore likely that, for the same reasons, the increase in regular earnings in the coming months will be higher than total average earnings. The impact of bonuses can also be seen from the fact that the increase in median gross earnings (14.1% YoY) was exactly the same as the increase in average gross earnings.

Wage dynamics (three-month moving average, % YoY)

The detailed data also shows that the base effect of last September's pay settlement for law enforcement officers influenced the change in average wage growth in the whole economy. In the public sector, the pace of wage growth slowed considerably, from almost 15% to just under 12% YoY. Meanwhile, wage growth in the private sector has also slowed, although this is mainly due to a decline in the level of one-off payments.

Looking at the individual branches of the economy in general, the pace of wage growth has slowed significantly almost everywhere, but there are a few exceptions, like scientific and technical activity, and education.

As inflation continued to slow in September, the 12-month negative real wage growth on an annual basis has come to an end, despite the slowdown in average wage growth. The purchasing power of average wages was 1.7% higher in September 2023 than it was a year earlier, which is a significant change, but at the same time needs to be taken with a pinch of salt. In general, this simply means that the purchasing power of the population has started to increase again compared with the previous year.

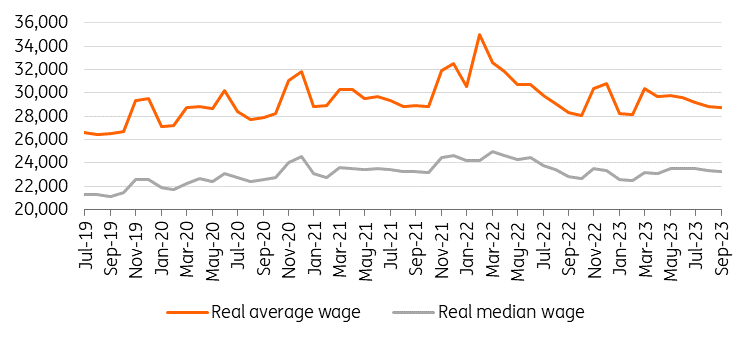

The level of average and median real wages (1990 CPI adjusted HUF)

The problem might be that this is only one month of positive data, and it looks at the growth compared to the same period of the previous year. However, if we look at the level of monthly real wages at 1990 prices (i.e. we are not looking at a percentage change), our calculation shows that the level of real wages was 28,784 forints (around US$83). This compares with an average monthly wage of around 31,000 forints (US$89) in the last three months of 2021, calculated at 1990 price levels. This shows that the current positive year-on-year change basically marks the beginning of a recovery and that there is still a long way to go before the purchasing power of wages catches up with the decline caused by the inflation shock and the living standards crisis.

The purchasing power of average wages is currently around the average in 2020, so we have managed to invent the time machine and get back to the 2020 standard of living in terms of wages. None of this suggests that households are going to start consuming a lot just because a statistic has gone from negative to positive. The recovery in domestic demand will therefore be a slow and gradual process, in our view.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article