Europe’s job market is increasingly AI-ready

AI is set to become a key and much-needed economic growth driver. In recent years, job growth in Europe has centred on tasks that artificial intelligence can speed up or even take over. But we could soon see a two-tier Eurozone, with the north outpacing the south in AI-related productivity gains

With low growth and ageing societies, boosting productivity growth is key to economic prosperity in the eurozone in the years ahead. And that’s where AI comes in. Productivity has declined by 1.6% since the third quarter of 2022. This has come with a tight labour market by historical standards, as unemployment has dropped to the historical low of 6.1%. And with populations ageing, the chances of growth in the active population are small. So, we need artificial intelligence to revamp that productivity growth in the coming years.

So, which jobs will be impacted, and how? That’s what we’re trying to answer. And here’s an interesting point: most job creation in the eurozone has been in occupations most susceptible to AI innovation. And whether tasks are merely speeded up or completely taken over, both channels would improve productivity growth. Of course, many people will feel threatened by that, and they’ll certainly feel the effects.

Another crucial point in this: we think Northern eurozone countries will be impacted more by AI initially than those in the south of the continent as current employment is more susceptible to AI disruption. This potentially unlocks more productivity growth in the north, which could cause further divergence of the growth potential.

So, in this report, we're going to be focusing on the potential of AI to impact jobs in the eurozone. We find that in recent years, most job creation in the eurozone economy has been in occupations which are likely to be impacted by AI in the years to come, either by speeding up tasks or by actually taking them over. As threatening as the latter will sound to many, both channels would improve productivity growth. This seems to be more the case in the northern than the southern eurozone markets. As the north currently faces more labour shortages and the south experiences high unemployment, that seems favourable for the overall economic outcome.

AI impact on jobs differs significantly between occupations

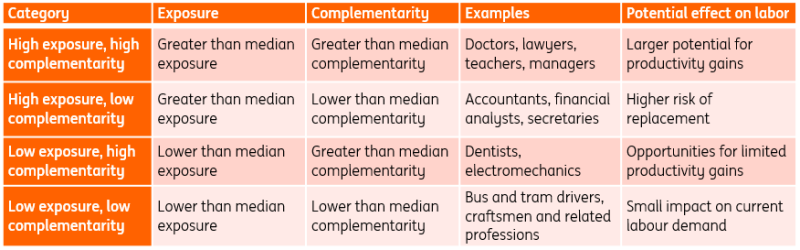

To get a sense of how much impact AI can have on the eurozone labour market, we categorise occupations into four groups along two axes: how exposed they are to AI and how complementary their tasks are to AI. In other words, how strongly could AI influence the tasks of a profession, whether AI could perform these tasks itself, or if AI provides support in performing them? We use the measure of complementarity from Pizzinelli et al. (2023), which builds on the exposure index of Felten et al. (2021).

A high score on both indicators suggests that a profession could extensively use AI in daily work and thus likely become more productive. A low score on complementarity and a high score on AI impact mean that AI could replace many tasks of a profession.

AI is likely to change the work of those with higher educational levels

Software developers and accountants are just two examples which fall into the quadrant, as they can expect more competition from AI because many tasks can be automated. Think of writing code and financial reporting, for instance. At the same time, lawyers and doctors could benefit significantly from AI in their work, as it can speed up tasks such as drafting documentation and staying up-to-date with developments. For legal, think of speeding up contract analysis and document review; for the medical profession, think of helping diagnose patients and transcribing medical documents.

Perhaps not surprisingly, people in manual labour, like construction and hospitality, seem to be less impacted by artificial intelligence. Overall, AI is expected to change the work of those with middle and higher education levels.

Classification of professions based on the impact of AI on work

Recent eurozone job growth has made the labour market more AI-compatible

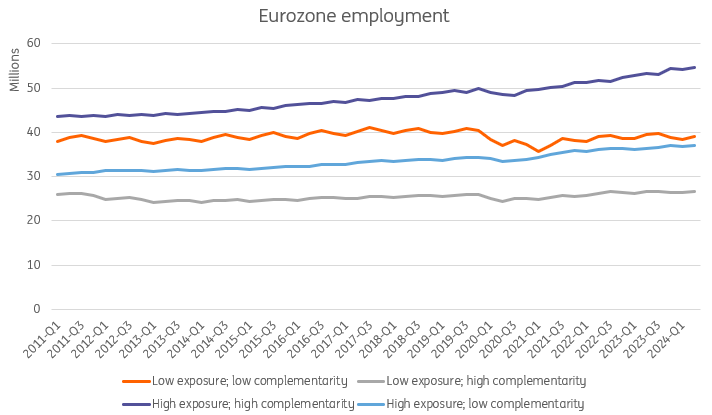

Looking at the entire eurozone labour market, jobs with a high exposure to AI account for the biggest part of it, with high-complementary jobs being the largest group. In large part, this is because of the sectoral growth in the economy, which has been more service sector-oriented. Jobs in the service sector generally have more tasks that can be performed by or enhanced by AI. In fact, it is exactly this category which also saw the fastest job growth since 2015, increasing its share of total employment from 32% to 35%.

Implementing AI would improve productivity in this group. Fast growth over the past five years has notably been seen here for engineers, teachers, admin professionals, and health professionals,.

Employment growth over time has become more favourable for AI improvements

The increase in jobs with high AI complementarity has mainly come at the expense of those which are the least likely to be impacted by artificial intelligence, those with a high degree of manual labour. This gap opened most notably during the lockdown period. Think of the hospitality sector, where waiters, bartenders, cleaners, and the like saw large declines in the number of people employed, and that figure hasn't yet recovered. This has resulted in a structural decline as a share of the total workforce, down from 28 to 25% between 2015 and now.

At the same time, we note that employment in jobs with a higher risk of being taken over by AI is also increasing. Over the past five years, general office clerks and software developers have been in the top three occupations, which have increased in absolute numbers in the eurozone. The steady increase over time was barely impacted by the pandemic and is likely to take over the 'little AI impact' group of occupations in terms of employment.

Of course, the big question is when will AI be advanced enough to be implemented so that this type of employment eventually becomes less relevant in the total labour market.

Country differences won't foster faster convergence

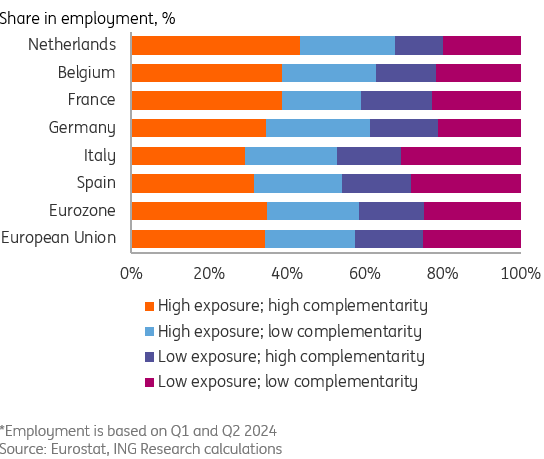

Within the eurozone, there are stark differences per country when it comes to the AI compatibility of current jobs. The northern European countries have a higher share of jobs with high exposure and complementary to AI. In the Netherlands, it is 43%, in Belgium and France, 39%, and in Germany, 35%. Economies with high value-added service sectors with a relatively high number of highly educated people are therefore very suitable to benefit from AI implementation.

The productivity gap between the north and south could become larger

In Southern Europe, the percentage of workers that can be affected by AI is lower. Notably, in Spain and Italy, the number of jobs that have little to do with AI is still large: almost half. However, in Southern Europe, unemployment is also much higher, and labour shortages are smaller, which means that efficiency gains have the potential to be more disruptive to the labour market in these countries.

That might be a positive, but the productivity gap between the north and south could become larger on the back of AI implementation, which generally is not good for economic convergence in the bloc.

Differences between countries show higher AI potential in northern eurozone countries

AI's potential for productivity gains, growth, and divergence

Over time, the eurozone labour market has become increasingly compatible with AI-induced productivity improvements. As labour markets remain tight with unemployment at historic lows and the labour market rapidly ageing, this is a potentially key driver of economic growth in the years to come. At the same time, the question is how fast it can really be adopted widely.

While progress is being made, the broader labour market impact of AI so far remains modest. Once it does happen, though, it looks like northern European countries can profit more than those in the south, given the composition of their economies and labour forces. That means that the convergence within the monetary union of the last years could soon end. In fact, AI could disrupt not only the labour market but also broader convergence in the eurozone.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article