Credit Outlook - 21 calls for 2021: I want to break free (again)

We update our Credit Outlook for 2021, taking selected strategic calls. Where we look at what has happened thus far in 2021, and where our expectations are for the second half of the year. But quite simply, we think the greatest single determinant for credit market direction over the next few months will be rates.

After rolling in the deep, we want to break free

We often compare the state of the credit markets to song titles. Late last year, when we published our 2021 outlook, we dubbed it rolling in the deep, referring to how we expected credit spreads to tighten due to strong technicals despite underlying deterioration of leverage.

The call has been successful so far with pretty decent excess returns over swap rates, but total returns are almost exclusively negative due to underlying rates. For the second part of the year that returns picture is set to remain in tact, inflationary threat, pressure on credit metrics, low if any inflows and curve steepening combine for a less bullish environment thus this time credit spread tightening will not alleviate the pain.

Indeed we have frequently used Queen as our source of analogies, and as credit continues to trade at the low end of the 2021 range, we see potential for it to test the upper band of that range and basically for spreads to say, once again, we want to break free.

2021 thus far – don’t you remember

2021 has been as expected whereby the compression trade was indeed at the forefront, as spreads were in a slow slugging grind tighter.

Taking Euro financial and corporate indices as proxies, financials have tightened 9 basis points in total since the beginning of the year and corporates have tightened by 12bp. Meanwhile, Euro corporate BBB spreads have tightened 16bp year-to-date.

Spread developments and forecasted widening chart

The sector breakdown does illustrate the recent compression, with the likes of autos, leisure, services and real estate all outperforming substantially. Additionally, autos, leisure and real estate are the only sectors with positive total return on a YTD basis.

Spreads and return per sector YTD

Additionally, there has already been some slight steepening of curves. Outflows from longer-dated funds have accelerated over the past few weeks, particularly in USD. The USD market has had less of a demand for higher beta. In Euro, there has been a change for shorter duration debt. Flows have been largely skewed to the 3-5yr maturity. This may well indicate future softness in credit.

The credit markets

The greatest single determinant for credit market direction over the next few months will quite simply be rates.

The backdrop of a potential inflationary threat and dare we say it, the T-word - tapering will, despite strong credit market technicals, have a pronounced effect on positioning necessary for some excess returns in 2H21. In contrast to our 21 calls for 2021, we are now, therefore, a little more bearish.

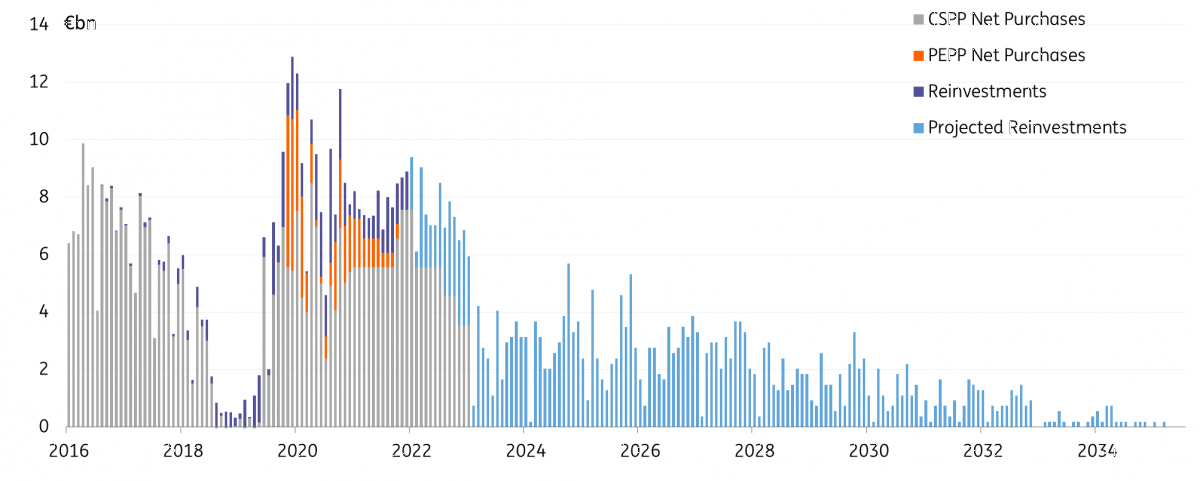

Any widening in credit will be limited; the ECB failed to give further guidance last week and made no mention of tapering nor slowing PEPP. As expected the ECB meeting was rather uneventful. The only noteworthy thing was that front-loading of PEPP would continue. This means there will likely be around €2bn in corporate purchases per month under PEPP. This comes on top of the €5.5bn average net purchases from CSPP per month.

Additionally, coming into the second half of the year we are more likely to see less ECB eligible supply coming into the market, in the form of corporate hybrid supply and Reverse Yankee supply. In which case, we may see the ECB being pushed more and more into the secondary market. This is of course very supportive for spreads and we favour eligible debt for the second half of the year. This may also delay our bearish stance somewhat for eligible debt, as the ECB keep spreads supported.

ECB's corporate purchases and future projection

Of course, the messaging from the ECB, in terms of the end of PEPP, is centred around keeping the support in play as long as needed.

However, it must indeed end at some point, and a potential option for the ECB to add a smoothing effect is to increase APP purchases to absorb the pain. This could be as significant as €40-50bn per month, up from the current €20bn per month. Whilst most will be needed to target PSPP; we feel that the ever popular CSPP will also benefit. Indeed we wouldn’t be surprised that the net result is zero; in other words, CSPP increase in purchases of corporate credit could outweigh the lack of further PEPP involvement in credit. That bump in purchases could be to the tune of the current net €5.5bn to target €7bn per month. Currently, CSPP runs at 25% of APP, so a slight decline would still mean a net rise.

These strong technicals are further supported by a few other elements:

- Exodus from credit unlikely given that rates will remain historically low; the need for even the slightest bit of possible yield ensures a lasting bid for credit.

- Looking farther afield, CSPP may well remain active until mid-2023. The messaging here from the ECB is that it shall remain until shortly before they start raising the key ECB interest rates. Our economists are looking for the first rake hike to be in late 2023.

- Besides looking even further afield, the reinvestments of redemptions by CSPP shows an increasing trend whereby later in 2023 and into 2024 onwards, we expect that when we look at only the re-investment flows, the credit will still be supported by a bid of some €2.5bn a month on average.

- The slowing of supply compared to 2020 and the expected drop for H2 2021 also entails that CSPP struggles to purchase the volume needed through the preferred route of primary purchases but is increasingly pushed into the secondary market hence supporting spreads.

Nonetheless, the current tight valuations, supply (targeting the long-end), and importantly upwardly mobile underlying rates will combine to create a less positive environment for credit.

The shorter maturities are favoured for the second half of the year,

- Defensive positioning.

- Credit in the short-end is cosmetically cheap as it has in the recent past struggled, in spread terms, to dive further into negative-yielding territory. A slow rise in short-end rates improves the potential for this negative-yielding credit to tighten.

- L&M exercises target the short-end as excess liquidity raised in 2020 is put to work. Consequent supply targets the long-end.

- Parking liquidity, the same excess liquidity, is at times used to buy short-dated credit.

On the other side of the pond, the FED firesale of ETF and corporate bond holdings might not be too much of a big news item or direct driver for spreads, but it is just another ingredient to a more bearish credit outlook. In combination with more pressure on rates in the US, the limited ETF and mutual fund inflows will struggle to keep pace with these sales. Despite low supply, we feel that spreads will be softer in USD, both softer in terms of relative performance to EUR and expecting these too to target and end of year target of the higher end of the 2021 trading range.

What does this mean in terms of credit markets

- Excess returns at best minimal

- Favour short-end

- Play hybrids for yield selectively

- Compression trade starts to falter, assess risk to higher beta sectors.

Corporate supply – right on track to hit forecast of €350bn

On a year-to-date basis, corporate supply is sitting at €162bn. This is, of course, below the substantial crisis-fuelled supply of last year, sitting at €242bn YTD. But supply is now running ahead of 2019's YTD supply of €156bn. Supply thus far is nicely in line with our forecast of €350bn by the year-end, in which we had forecast €200bn in the first half and €150bn in the second half of the year.

We expect supply in June to pencil in c.€30-35bn, leaving the first half of 2021 supply just marginally shy of the €200bn expectation.

Forecasted supply per quarter

We have, however, slightly adjusted our sector breakdown of supply. The real estate sector in particular has been very substantial this year.

On a YTD basis, the real estate supply sits at €28bn, up significantly from €16bn last year YTD and €10bn in 2019 YTD. We expect real estate supply will remain relatively heavy and reach up to €50bn by the year-end.

On the other hand, the consumer sector has been rather underwhelming, with just €6bn YTD. When compared to the substantial €47bn pencilled in by this time last year, and €23bn in 2019.

Supply forecasts per sector

Reverse Yankee supply expected to rise - USD to underperform EUR

We still expect USD spreads to underperform against EUR later in 2021. Alongside this, we see the cross-currency basis swap and 3m vs 6m roll to remain tight and expect it to remain so. In combination, this will offer a cost-saving advantage for US corporates to issue in EUR and swap back to USD. As a result, we stand by our forecast for corporate Reverse Yankee supply to reach €80bn by the end of the year.

USD spreads will particularly underperform against EUR spreads when we see the inevitable weakness in the credit markets in the second half of the year, particularly when we begin seeing widening on the back of inflationary fears, tapering and a rise in rates. This is largely due to the technical picture being notably stronger in Euro than in USD, particularly with the ECB remaining active in purchasing corporate debt.

Cross currency basis and excess USD over Euro 5yr

Cross currency basis and excess USD over Euro 10yr

Corporate hybrids - we expect hybrid supply to continue to be substantial

Corporate hybrids have also seen significant supply. The YTD total is up to €22bn. This is already ahead of the previous year's full-year totals. Nonetheless, this is still marginally below our expectations, and still, a sizeable amount of supply is required to reach our forecast of €50bn. In any case, we expect hybrid supply to continue to be significant.

There is still significant value in hybrids relative to Equities in terms of valuation, but hybrids are trading very much in line with BB rates spreads. However, when compared to B rated spreads, there is certainly some value to be found.

Hybrids vs Equities

Illustration of a regression between corporate hybrid spreads and equity prices over the past 5 years

Hybrids vs BB Spreads

Illustration of a regression between corporate hybrid spreads and equity prices over the past 5 years

ESG - Covid the catalyst for ESG in credit

When credit markets widened and concerns over Covid-19 grew at the start of the pandemic, there was a huge outflow from mutual funds that invested into credit. Some 30% of assets under management were withdrawn in a month or so. But the retracement of these funds has been strong, and 2020 ended with net inflows. A closer look at this shows a very green picture as the initial Covid exodus has caused demand for green to increase relative to grey debt. Fund flows inflowing into ESG have basically dominated flows and caused a shift from grey to green. Indeed in some cases, non-ESG funds have seen outflows over the last few years.

Over the past two years, ESG funds have accumulated a substantial inflow of 85% of assets under management (AuM). Non-ESG funds have seen only marginal inflows, which has accumulated to just 3% of AuM over the past two years. And indeed, non-ESG funds have seen mostly outflows since August of 2020.

Euro fund flows – ESG vs Non-ESG

Funds inflowing into ESG mutual funds is very substantial

The growing ESG market is still unbalanced in terms of demand and supply. Indeed there is a clear increasing and strong demand for ESG debt. However, the supply is still lacking in relative terms. Sustainable-linked bonds do offer an easier way for issuers to come to the ESG market. As the market grows, we will see normality and balance prevail.

ESG supply has consistently been increasing. Already there has been €30bn in corporate ESG supply this year, running ahead of last year's €18bn. This year, financials have supplied €24bn, up significantly from the €6bn supplied last year YTD. Last year pencilled in &euro 64bn in total ESG supply, of which €39bn was from corporates and €25bn from financials. We forecast ESG supply to reach at least €50bn in Corporates and &euro 50bn in Financials this year.

We see the sustainability linked bonds market as the fast-food of ESG bond finance compared with the white linen tablecloth variety of green bonds, which are best associated with a Michelin-starred restaurant where everything is perfectly laid out. By which we mean, sustainability linked bonds are significantly easier, simpler and quicker to issue, and as such, these bonds are certainly gaining traction. Last year saw €3.5bn in supply. Already in 2021, €3.3bn has been supplied.

We see this as supportive in several ways:

- It allows more issuers to tap ESG demand as the process of issuance is far less complicated. This will be particularly advantageous for less frequent issuers.

- It adds more volume to the ESG market as a whole as an alternative to a green bond. The ESG market is certainly growing year on year. However, there is still a balance issue relative to the strong demand for it.

- It is still ECB-eligible. The ECB has included a provision to work around their guidelines in which debt with a step coupon is in principle ineligible as collateral by making step coupon bonds eligible if they are tied to ESG targets.

Update on our 21 calls for 2021

1. Technicals dominate, carry pays, spread softness potentially for 2H21

Technicals still dominate as the ECB remains active, net supply remains relatively low, and fund flows are positive, albeit marginal. We still expect spread widening in the second half of the year.

2. Steepening curves to persist, Hybrids to hit €50bn

Curves have begun steepening over the past few weeks from the very flat levels. We expect this to continue, notably as spreads widen and rates rise. This will be particularly seen in BBB rated curves. Hybrids supply sitting at €22bn YTD.

3. Value in USD, reverse yankee supply will resurge

Reverse yankee supply has been limited this far, but we expected a late runner. Sitting at just €25bn YTD, we expect supply to pick up in the second half of the year as USD spreads are expected to underperform against EUR spreads.

4. Expected default rates too low

We expect default rates to rise slightly from here, but we also expect default rates to stay elevated for a prolonged period. Under the basis of our economic outlook, spreads are looking too rich as we expect widening, a continuation of downgrades and fallen angels and the growing pool of leverage with worsening leverage metrics.

5. Prefer corporates over financials

We maintain our preference for corporates over financials on the back of CSPP and PEPP purchases and a more challenging environment for European banks in 2021. We maintain our Overweight stance on utilities, telecoms, healthcare, household goods and banks bail-in.

8. Corporate supply to fall, but will still be a sizeable amount

Supply thus far is nicely in line with our forecast of €350bn by the year-end, in which we had forecast €200bn in the first half and €150bn in the second half of the year. We expect supply in June to pencil in c.€30-35bn, leaving the first half of 2021 supply just marginally shy of the €200bn expectation.

16. Financials Supply: More of the same

After further favourable TLTRO conditions, our financials supply forecast was taken down. In any case, it will still be very similar to slightly less supply compared to last year.

19. 2021: another groundbreaking year for sustainable supply

The growing ESG market is still unbalanced in terms of demand and supply. Indeed there is a clear increasing and strong demand for ESG debt. However, the supply is still lacking in relative terms. Sustainable-linked bonds do offer an easier way for issuers to come to the ESG market. As the market grows, we will see normality and balance prevail.

20. ESG to outperform in 2021

The growing demand will indeed produce a 'greenium' (green premium). However, this is not currently being seen in the considerably tight environment in which we're trading. We will likely see more ESG outperformance when spreads begin to widen, as ESG spreads will hold firmer.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

14 June 2021

Surprise, surprise This bundle contains 5 Articles