4% annual GDP growth in Hungary looks out of reach

The Hungarian Central Statistical Office confirmed the stagnation in GDP in the fourth quarter of 2023. The carry-over effect will be weak and the details point to some stress points, which makes us less optimistic about the outlook

| 0.0% |

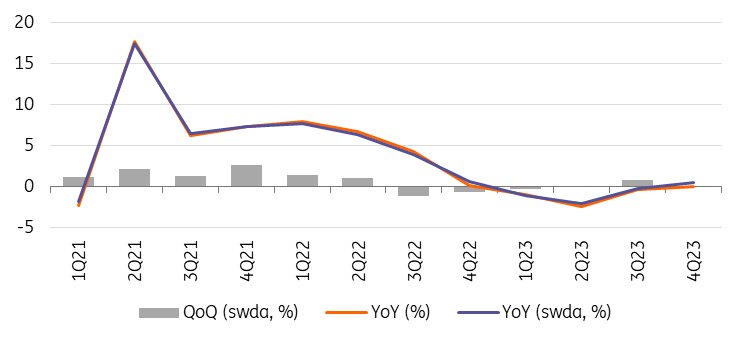

GDP growth in Q4QoQ, seasonally and working day adjusted |

Stagnation confirmed

As expected, the Hungarian Central Statistical Office (HCSO) made no significant changes to the fourth quarter GDP data. On a quarterly basis, the Hungarian economy stagnated at the end of last year. The seasonally and calendar-adjusted year-on-year index improved to 0.5% after an incremental positive revision. The raw figure was unchanged at 0.0%, underlining the impact of fewer working days in the fourth quarter.

The effect of the small revisions, which affected earlier quarters, brought the decline in GDP to 0.7% for the whole year in 2023 (calendar adjusted). On the basis of the raw data, the economy contracted by 0.9% due to fewer working days than in 2022. There were no major surprises in the detailed data, with individual segments of the economy performing broadly in line with expectations. The weaker-than-expected GDP figure was the combined effect of all factors rather than any surprise underperformance of one segment.

Hungarian GDP growth

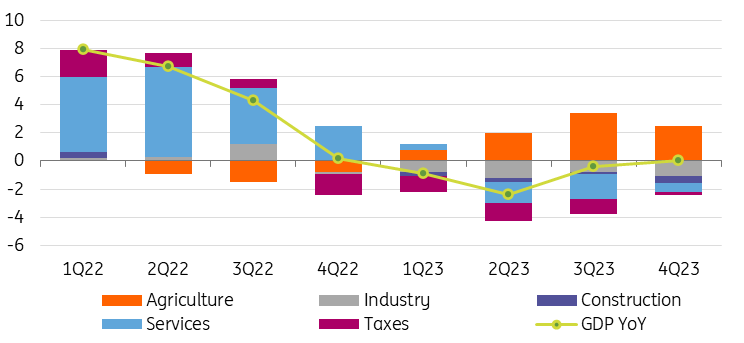

Agriculture saves the day, Services finally improve

On the production side, as was to be expected from the monthly statistics, industry and construction contracted, holding back quarterly GDP growth. The problem for industry, apart from weakening export activity, is still the lack of domestic demand. The construction sector has a long-standing problem - the high interest rate environment and subdued public investment momentum have resulted in insufficient replacement of those projects approaching completion.

On the other hand, agriculture made a positive contribution, once again acting as a major driver thanks to favourable weather conditions. Its value added rose by 4.2% on a quarterly basis. Otherwise, the only significant positive factor in the fourth quarter was the services sector, which finally helped the economy after five quarters of decline. Rising real wages, increasing purchasing power and a gradual improvement in consumer confidence were already reflected in this segment, which grew by 1.5% on a quarterly basis. The fastest growing sub-segments were leisure and logistics. The latter is likely to reflect the improvement in purchasing power in the form of increased demand for online shopping and households' growing demand for entertainment.

Contributions to GDP growth - production side (% YoY)

In terms of traditional year-on-year growth indicators, agriculture grew by 81.1% in the fourth quarter, on the back of a supportive weather situation this year and an extremely low base last year. All the other main components of production recorded significant declines. Industry and construction were around 8% weaker than a year earlier, with both sectors showing a marked deterioration in their year-on-year indices from the third quarter as well. Wholesale and retail trade contracted by almost 10%, suggesting that improving consumer confidence is not the panacea to quickly cure economic problems.

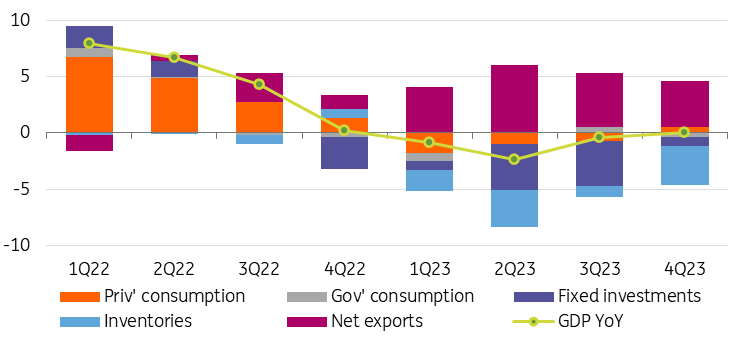

Export continues to weaken, domestic drivers improve

On the expenditure side, household final consumption expenditure continued to grow on a quarterly basis, in line with the performance of the services sector. Government consumption was more subdued than in the third quarter, reflecting the weak fiscal situation and the need for more caution on the budget side. As can be seen from the detailed investment report released by the HCSO, gross fixed capital formation increased in parallel with the improvement in construction investment, offsetting declines in other areas.

The most notable weakness was in exports of goods, which fell for the third consecutive quarter, most recently by 2.4% on a quarterly basis. It is therefore apparent that the contraction in global external demand and the general weakness in the manufacturing sector observed around the world are also weighing on Hungary's export sector. With domestic demand still weak (though healing) and energy consumption more constrained, the country's demand for imports has continued to shrink.

Contributions to GDP growth - expenditure side (% YoY)

Again, turning to the year-on-year indicators, these show that domestic demand fell by almost 4% in the fourth quarter. This was mainly due to a sharp decline in government consumption, in line with subdued spending due to the difficult fiscal situation. The 4.1ppt contribution to growth from net exports was just enough to offset the decline in domestic demand. The performance of foreign trade has gradually deteriorated over the past three quarters, a clear warning sign, while domestic drivers have shown continuous improvement.

Our expectations are for a subdued 2024

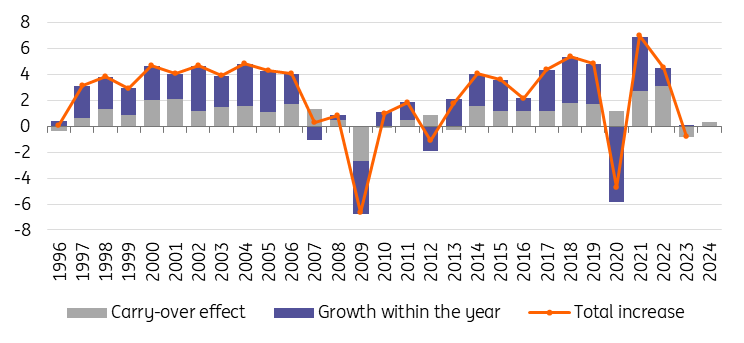

For 2023 as a whole, therefore, the Hungarian economy shrank by 0.9% on the basis of raw data. The saviour was agriculture, without which Hungarian GDP would have shrunk by 3%. All other major sectors of the economy contracted, so it was a general downturn that affected all sectors of the economy. 2023 was a crisis year. What makes the overall picture even worse is that the carry-over effect will also be small due to the weak performance in the fourth quarter.

If the Hungarian economy were to stagnate in every quarter of 2024, as it did in the last quarter, the statistical effects would result in GDP growth of only 0.4% this year. The carry-over effect in this year’s economic activity will be 0.4ppt. In order to achieve the annual economic growth of around 4% that the government is hoping for, each quarter of this year would have to show growth of at least 1.5% when compared to the previous quarter.

Composition of Hungarian real GDP growth (% YoY)

The Hungarian economy has never been able to achieve such dynamic growth for four quarters, with the exception of the special recovery period after the extreme Covid downturn. The closest we came to this was around 2018, when there was much higher business and consumer confidence, an extremely low interest rate environment, supportive monetary and fiscal policies, and a record-strong Hungarian labour market. In the absence of all this, we can hardly expect the economy to grow by around 4% this year.

Consumption and investment should slowly improve on the back of real wage growth, a declining interest rate environment and the arrival of EU funds. Continuing with the positives, the inventory effect could be a supportive factor as well. Countering this, the rise in unemployment is a warning sign. The recovery in domestic demand could be increasingly offset by a continued weakening of exports, particularly given the latest global manufacturing situation.

Industry could be a drag on growth this year (based on our carry-over calculations), construction will not be dominant and agriculture will also drag on growth due to the high base and having a year of average crop yields (or even below average as some recent reports suggest). The services sector could therefore be the sole driver of the economy this year. Against this backdrop, our latest 2024 GDP growth forecast is 2.1%.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article