The Commodities Feed: Oil surges on escalation fears

Oil prices have surged early morning Friday with unconfirmed reports of explosions in the Middle East. Meanwhile, cocoa prices hit new record highs after robust grinding data

Energy – Middle distillate concerns

Oil prices have surged this morning with Brent more than 2% higher at the time of writing, following unconfirmed reports of explosions in Iran, Syria and Iraq. If these reports turn out to be true, fears over further escalation will only grow, as well as concerns that we are potentially moving closer towards a situation where oil supply risks lead to actual supply disruptions.

As we mentioned earlier this week, middle distillate cracks have come under significant pressure more recently which will be raising demand concerns. The prompt ICE gasoil crack is now trading close to US$18/bbl – the lowest levels since July last year. In addition to weaker cracks, the prompt timespread has also flipped from backwardation into contango, suggesting ample supply in the prompt market. The spread has weakened from a backwardation of more than US$9/bbl earlier this month to a contango of US$2.50/bbl currently.

Meanwhile, the latest trade data from China shows that diesel exports in March totalled 1.42mt, up from 630kt the previous month, but still down 1.7% YoY.

While middle distillate fundamentals are clearly weaker, there are still risks surrounding the market, given Ukrainian drone attacks on Russian refining capacity.

Inventory data from Insights Global show that gasoil inventories in the ARA region fell by 25kt over the last week to 2.12mt, but still leaves stocks largely around the 5-year average. In Singapore, middle distillate stocks fell by 1.07m barrels to 10.14m barrels, which again is still broadly in line with the 5-year average.

US natural gas prices strengthened yesterday with front month Henry Hub futures settling more than 2.6% higher on the day. This is despite storage data from the EIA yesterday coming in largely in line with consensus. US natural gas storage increased by 50Bcf last week, compared to expectations for a 51Bcf increase, but below the 5-year average of a 61Bcf increase. Total US natural gas storage remains very comfortable with it standing at 2,333Bcf, up 22% YoY and more than 36% above the 5-year average. While high inventories have weighed on prices for much of the year, expectations for largely flat domestic supply growth and the ramping up of LNG export capacity later this year suggests the US gas balance should tighten later this year and into 2025.

Metals – China metals output near record highs

Chinese refined copper and zinc production reached near-record levels in March despite persistent weakness in domestic smelters’ profit margins, data from the National Bureau of Statistics showed. Refined copper output rose 7.9% YoY to 1.15mt last month, while daily production averaged 37kt/d – near the all-time high of 38kt/d reported in November. Cumulatively, copper output rose 10% YoY in the first quarter of the year. As for zinc, monthly output rose 3.5% YoY to 651kt or 21kt/d in March, close to the record of 21.9kt/d in November. Spot copper TCs in China fell to record lows of $0.10/t last week, according to data from Fastmarkets,

Cancelled warrants for most base metals on the LME jumped sharply yesterday indicating market nervousness about the new Russian metal sanctions. Cancelled warrants for copper rose 14,350 tonnes to 32,525 tonnes as of yesterday, the biggest daily move since 18 October. Meanwhile, requests to withdraw aluminium rose 16,000 tonnes to 294,975 tonnes, while cancelled warrants for lead increased 19,100 tonnes to 126,625 tonnes as of yesterday.

Agriculture – Cocoa grinding data remains firm

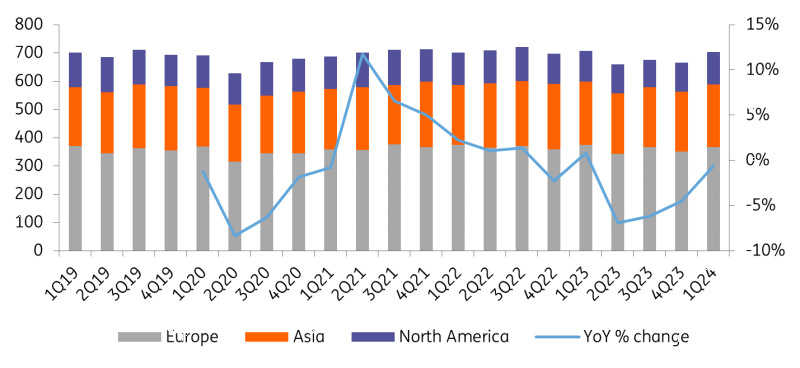

Cocoa prices saw significant strength once again yesterday on the back of robust grinding data. London cocoa rallied by more than 9% on the day, and traded to a record high of GBP9,809/t. The high price environment we have seen in cocoa for sometime was expected to weigh on demand. However, aggregated 1Q24 grinding data for Europe, North America and Asia was down just 0.6% YoY, and actually up 5.5% QoQ. The stronger data was driven by North America with grindings up 3.7% MoM, while Asian and European grinding was down 0.2% and 2.2% YoY respectively. The robustness in the data suggests that cocoa prices will need to stay higher for longer to ensure adequate demand destruction, given the large deficit the global market faces this season.

In its recent monthly update, the International Grain Council decreased its 2024/25 global corn output forecast from 1,233mt to 1,226mt largely driven by the output losses expected from the US, while consumption projections were lowered to 1,223mt from previous estimates of 1,230mt. Meanwhile, global corn-ending stocks are expected to fall to 291mt from 297mt. Similarly, the council cut its global wheat ending stock estimates to 259mt from its March projection of 262mt. For soybeans, the council left its 2024/25 global ending stock estimates unchanged at 75mt.

The latest trade numbers from China customs show that corn imports declined by 22% YoY to 1.7mt in March. The decline in imports could be largely attributed to estimates for a record 2024/25 domestic crop, due to improved yields and increased plantings. Meanwhile, cumulative imports are still up 5.1% YoY to total 7.9mt over the first three months of the year. Among other grains, monthly wheat imports surged 34.2% YoY to 1.8mt, although cumulative imports are still down 1.4% YoY to total 4.3mt.

Cocoa grinding remains robust despite surging prices (k tonnes)

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

Oil Natural gas Middle East Middle distillates Metals LME Grains Geopolitics Diesel Copper CocoaDownload

Download article