The challenges brought by shrinking central bank balance sheets

Quantitative tightening and a reduction in central bank liquidity will add upward pressure to long rates. Money market rates were suppressed in 2022. In 2023, they will be free to reflect systemic risks

The age of quantitative tightening

The Federal Reserve will continue to allow US$95bn of bonds per month to roll off its balance sheet over the course of 2023. At the end of 2022, the balance sheet will have shrunk by a little over US$0.5tn, and then a further US$1.1tn is scheduled to be rolled off by the end of 2023. That would be a cumulative reduction of over US$1.6tn if all goes to plan. One issue here, however, is the roll-off over the second half of 2023 would co-exist with interest rate cuts from the Fed. While these may seem at odds with one another, remember that balance sheet roll-off is not outright selling bonds (hard quantitative tightening), it’s just allowing the Fed’s balance sheet to normalise. That can be viewed as a separate exercise to interest rate cuts, at least for a period.

QT can be viewed as a separate exercise to interest rate cuts, at least for a period.

The Bank of England is also well advanced on the way to quantitative tightening. The first non-reinvestment of a gilt reaching maturity occurred in March 2022, and the first gilt sale took place in November. Overall, the Bank intends to shrink its balance sheet by £80bn a year in the first year through a mix of passive (non-reinvestments) and active (outright sales) QT. This pace may accelerate in future years, but we assume that this is the relevant pace in the near term which, in FY 2023-24, should result in roughly half of that amount in passive and half in active QT.

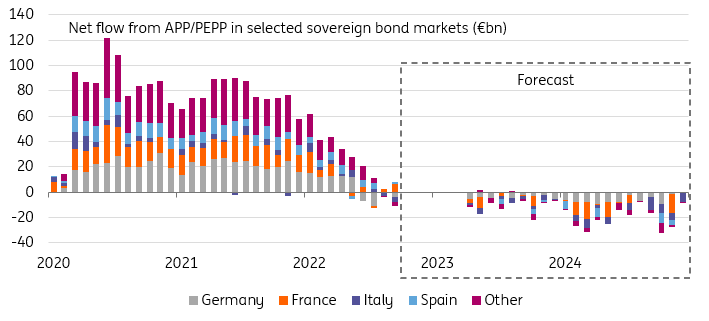

Net QT flow out of key European government bonds in 2023 should be limited

The European Central Bank is only at the beginning of this process. QT will start in 2023 with a gradual phasing out of its Asset Purchase Programme redemptions (one of its two QE bond portfolios), followed by the same process for the Pandemic Emergency Purchase Programme (the other portfolio) in 2025. Assuming a 50% APP reinvestment cap for the second and third quarters, and an end in the fourth, the balance sheet reduction should amount to €156bn.

Counterintuitive and delayed effect on duration

The main effect of QE on markets is to suppress duration premium, the extra yield investors demand as compensation for taking interest risk over long periods of time. There are a variety of models that show how much lower yields are as a result of QE. In the case of the 10yr Bund, our own estimate stands at 230bp. It should also be noted that the effect of QE has typically been priced into yields before purchases actually happened. Markets are, after all, forward looking.

We’ve already seen part of the increase in yields that QT should trigger

As a general rule, we think it is fair to think of QT as QE in reverse. In our view, central bank balance sheet moves have been well-telegraphed months in advance, and so we’ve already seen part of the increase in yields that this should trigger. Much, however, depends on how long QT lasts. In a world where the process of balance sheet reduction is allowed to continue for years, the upward pressure on yields should gradually build up.

QE has supressed Bund yields by 230bp, but don't expect a sharp reversal

We’re more circumspect, however. We think QT poses financial stability risks and central banks will struggle to carry on once their policy focus shifts to easing. As a result, we suspect most of the upward effect on yields has already been felt. This is at least true for treasuries and gilts, and less so for euro rates. If we’re wrong, however, and central banks manage to significantly reduce their balance sheets, then some upside risk to our forecasts will have to be reckoned with.

If central banks manage to significantly reduce their balance sheets, then some upside risk to our forecasts will have to be reckoned with

What these models have in common is that the impact of QE is greater at longer maturities. At face value, this means QT should exert a steepening effect on the curve. In practice, it hasn’t. The reasons are manifold, but the main one is that the QT effect has been drowned out by central bank hiking cycles, typically a flattening influence on the curve. In places where the sequencing between hikes and QT is clearer, like in the eurozone, there is a better chance of that steepening effect to be visible once the ECB ends its hiking campaign over the course of 2023.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

10 November 2022

Rates Outlook 2023: Belt up, we’re going down This bundle contains 9 Articles