Central and Eastern Europe’s fiscal and monetary response to Covid-19

What is behind the magic of high numbers of anti-crisis programs to combat the economic fallout from Covid-19? Some CEE countries can afford policy responses like developed markets as their central banks kickstart QE support programs

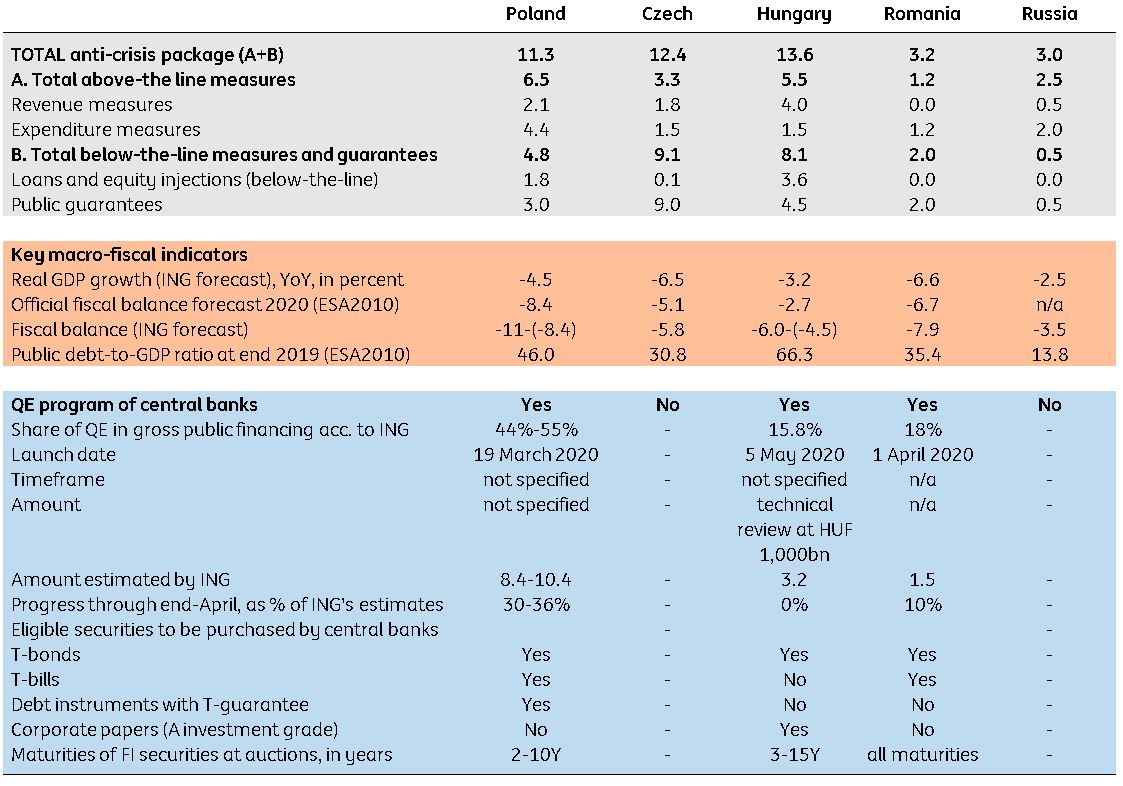

Above-and below-the-line rescue measures

Central and Eastern Europe countries are part of a select emerging market group, which can afford developed markets-like policy responses to Covid-19 recession: large fiscal stimulus backed by central bank asset purchases on the secondary market to prevent side-effects of higher public borrowing needs i.e. mitigate tightening of financial conditions, which would limit the positive impact of fiscal impulse.

The discretionary policy response to the pandemic can be split into:

- Above-the-line measures: direct support for companies and households through new spending, cuts in tax or social security contributions moratoria - they impact budgets and debt immediately.

- Below-the-line measures: public loans and capital injections and guarantees to firms in troubles. They affect fiscal accounts indirectly and partially.

Hungary: Biggest anti-crisis response package

Hungary announced the biggest anti-crisis response package of 13.6% of GDP, of which 60% is liquidity support, and the remaining 40% is direct fiscal support (the highest relaxation of tax burdens in CEE).

The National Bank of Hungary is starting QE with Govies purchases on 5 May. In 2020, QE may reach up to 3.2% of GDP and cover 16% of gross public borrowing needs. In the past, mortgage and corporate bonds were already on the list of eligible assets purchased by the central bank, and these programmes are likely to be extended.

Czech Republic: Guarantees-based package and the most conservative central bank

The Czech Republic pledged to deliver the second biggest anti-crisis program in the region of 12.3% of GDP.

It seems to be high, but it requires much red tape, so it starts slowly and doesn’t serve as fast as expected. Also, public guarantees constitute 70% of the program, while direct fiscal support amounts to just 3.2% of GDP. The program does not benefit from support from the central bank in terms of QE.

The Czech national bank remains the most conservative in the region as it cut interest rates but claims that QE is the last resort measure, which can be deployed in the case of a prolonged recession, the threat of deflation or financial stability risk.

Poland: Largest QE-based fiscal shield in the region

Poland ranks third in this comparison with the announced measures totalling 11.3% of GDP.

But the fiscal component encompassing direct support is the most generous in the region. The Polish government took the boldest redistributive measures, with additional discretionary spending on protecting jobs, sustaining incomes for households, and supporting firms. Overall, above- the- line fiscal measures should reach 6.5% of GDP. In relation to GDP, this is the highest fiscal stimulus not only in CEE but in Europe.

Poland's fiscal measures are not just the biggest in the CEE region, but also in Europe

Such a fiscal shield would not be possible without a large central bank program of asset purchases, which may reach 8.4-10.4% of GDP according to our estimates and should be the highest in the region. So far, a large expansion of central bank balance sheet has not affected the currency. We explain it by a strict liquidity control - money printed is tightly managed by the state-owned bank BGK so shorting PLN isn't easy. NBP cut interest rates aggressively and frontloaded aggressive POLGBs purchases, which led to a drop in T-bond yields.

More than half of the projected net public borrowing needs in 2020 should be satisfied by other bonds aside from Polish government bonds, issued by BGK and the Polish development fund. They should be bought by local banks, and then to a large extent purchased by the central bank, and foreign investors looking for extra spread vs expensive POLGBs. Strong central bank support for the government bonds market also prevents adverse currency reaction to high QE.

Romania: Moderate fiscal stimulus with first-ever but modest QE

Romania's anti-crisis program of 3.2% of GDP, of which 2% of GDP are public guarantees is relatively small. The direct support is just 1.2% of GDP because the government conducted procyclical policy in the past and brought the deficit to a high level. It could only add a small fiscal stimulus now.

The National bank of Romania has started its first-ever QE program in April, but its scale is limited due to worries about RON fragility.

Russia: Modest anti-crisis response with no QE in sight

The Russian anti-crisis response has been modest so far, just 3% of GDP.

In this package, 2% of GDP is spending (of which only 1% of GDP are new outlays), another 0.5% of GDP are tax breaks. The public guarantee program is just 0.5%of GDP. The public support is targeted - only the most affected individuals and businesses are eligible. We expect a new wave of support measures to be announced soon totalling around 1% of GDP, evenly split between state guarantees and public spending.

Quantitative easing doesn't seem to be on the cards in Russia, but the central bank is likely to continue easing monetary policy from the current 5.5% to 4.5-5.0%. Also, it is ready to provide refinancing loans to banks if required.

CEE's anti-crisis response, as % of projected GDP in 2020, unless otherwise indicated

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

7 May 2020

Covid-19 pandemic: Entering the next phase This bundle contains 14 Articles