The Bank of England’s August dashboard

Will the Bank of England push back on rate cut speculation this week? We doubt it, even though its forecasts may actually point to even more overheating over the next few years. The Bank's smooth Brexit assumption is increasingly under question, although on balance we expect interest rates to stay unchanged for the rest of the year

The Bank of England's August dashboard

Will the Bank push back on rate cut expectations? We doubt it

The August inflation report will undoubtedly be an awkward one for the Bank of England. When policymakers sit down to discuss monetary policy this week, there will be less than three months left until Brexit, making it very tricky to craft a set of new forecasts.

On the face of it, market pricing – which is now looking at a 50% chance of a rate cut this year – is too flat for policymakers’ liking. The forecasts the Bank published back in May already pointed towards a risk of the economy overheating – a subtle hint that rates may need to rise faster than investors were assuming.

Will the Bank try and set markets straight, by explicitly pushing back against rate cut speculation? We think it's unlikely

The swaps curve (upon which the Bank's forecasts are based) has flattened even more since May, and this will only amplify the degree of overheating built into the Bank’s new projections. Growth and inflation forecasts at the two/three year horizon may get notched up slightly.

This begs the question, will the Bank try and set markets straight, by explicitly pushing back against rate cut speculation?

We think it's unlikely. Don’t forget that the Bank’s forecasts are premised on Brexit going smoothly – something that looks increasingly questionable. And while President Trump has opted against hitting China with fresh tariffs so far, there’s little sign of an imminent resolution to trade tensions either – a clear risk for global growth.

We therefore don’t expect the Bank to change its guidance on where interest rates will go next – other than to simply reiterate that “limited” rate hikes may be needed if Brexit goes smoothly. The challenge for policymakers will be to justify the inconsistency between their more hawkish forecasts, and more cautious rhetoric, without stepping into the political arena.

We think the Bank will use a similar tactic to the one they used back in June, which was to point towards the rising perceived risk of 'no deal' within financial markets, as a reason for extra caution on interest rates.

We don't expect interest rates to change this year

While the Bank’s guidance still notionally hints at tightening, we think this is very unlikely to materialise this year given rising Brexit noise. As we've recently noted, the risk of a general election later this year is clearly rising, and this will only add to the uncertainty currently weighing on growth. The prospect of further declines in investment, coupled with the recent lacklustre retail spending numbers, suggest underlying quarterly growth (once volatile production/inventory numbers are stripped out) will remain capped at around 0.2/0.3% for much of the rest of the year.

However we think talk of a rate cut is a little premature – wage growth is at a post-crisis high, and given this is as much a structural as a cyclical phenomenon, we suspect it will continue to perform solidly for the time being. Pay growth has been a key hawkish factor in its recent decision-making, and is a key reason why we think rates are most likely to remain on hold for the rest of the year

GBP implications: Asymmetric sterling reaction skewed towards downside

The BoE meeting this week should be a non-event for sterling, even if the committee strongly reiterates its guidance for eventual rate hikes, and pushes back against the current market pricing of rate cuts.

This is because markets are unlikely to interpret this scenario as realistic. Domestically, the perceived probability of a 'no deal' Brexit as well as early elections has risen, while externally, other global central banks are easing policy. Any attempt by the BoE to signal future rate hikes would therefore be viewed as highly non-credible by the market, and is unlikely to spill over into rate expectations or help GBP.

EUR/GBP could head towards 0.95 and GBP/USD below the 1.20 level over coming months

If anything, the GBP reaction to any dovish/hawkish surprises from the BoE is likely to be asymmetrical and skewed towards a weaker sterling. This is because the market will be more reactive to a dovish change in its interest rate guidance (for example if the bank acknowledges the case for cuts, effectively endorsing the market’s view), rather than a scenario where the BoE tries to make the case for hikes. As we said above, the latter is unlikely to be viewed as credible.

As we discussed in GBP: The pressure is building, we see clear downside risks to GBP over coming months. With the new government's rhetoric on a 'no deal' Brexit firming (e.g. Michael Gove’s comments that “no deal is now a very real prospect”) and the rising likelihood of early elections, sterling should remain under pressure.

EUR/GBP could head towards 0.95 and GBP/USD below the 1.20 level over coming months if early elections materialise, and the Conservative party under Boris Johnson runs on a divisive Brexit stance against the EU.

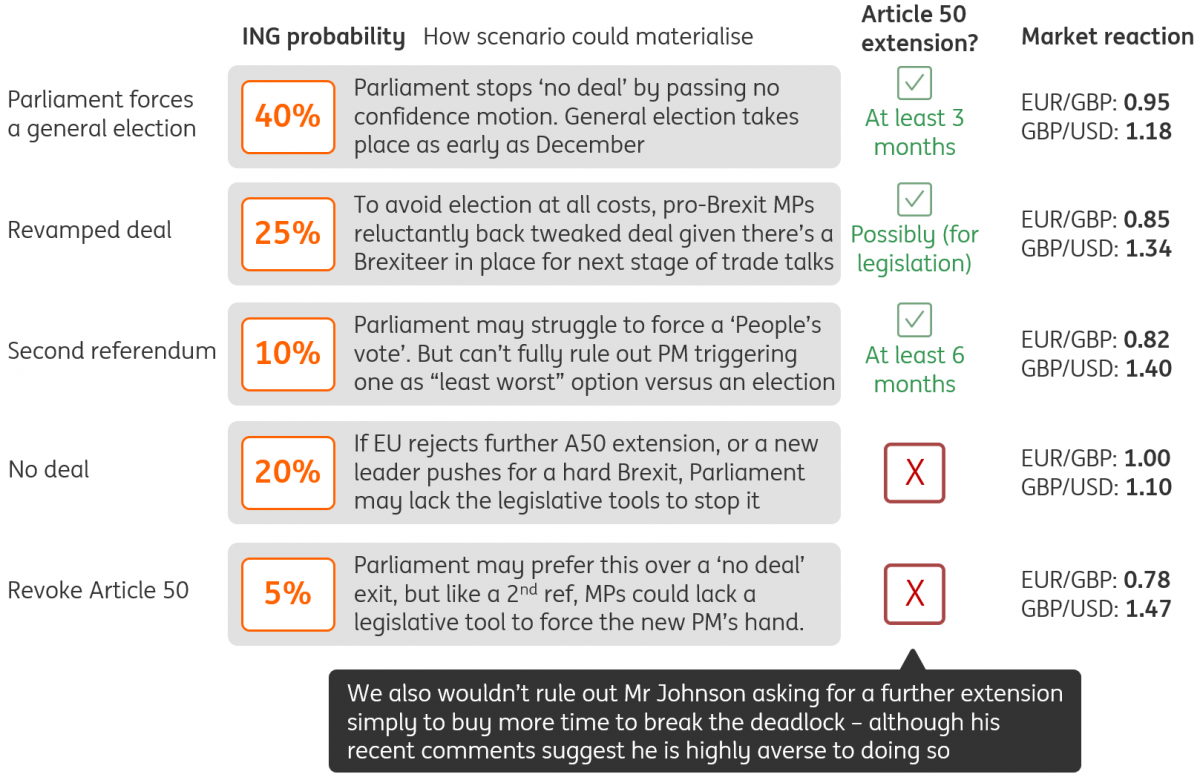

Our latest Brexit scenarios

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article