Promising growth figures for Switzerland, but 2020 looks challenging

Decent growth in the Swiss economy in the last quarter of last year coupled with rising economic indicators pointed to a dynamic 2020. But the coronavirus outbreak is sure to complicate things

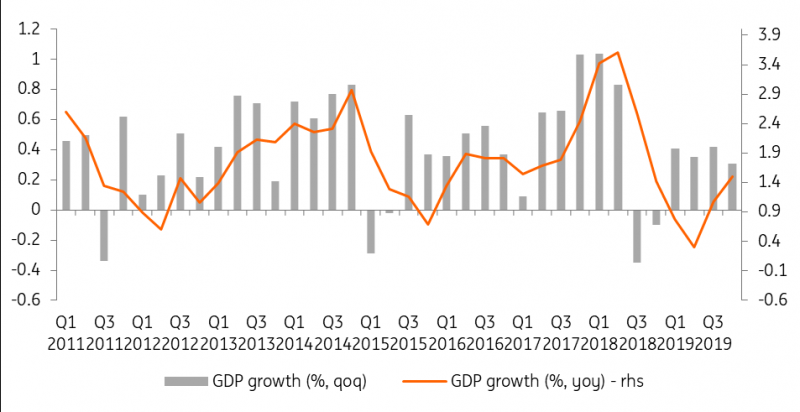

Decent growth in the fourth quarter

Swiss GDP growth stood at 0.3% QoQ in Q4 2019, a solid and expected result but down from 0.4% in the previous quarter. Manufacturing lost momentum, which was adversely affected by a less favourable international environment, and merchandise exports declined which had been the engine of growth in Switzerland until the third quarter. In the fourth, domestic demand supported economic growth, with household consumption rising, boosted by an increase in purchasing power due to falling consumer prices.

The Swiss economy was therefore in the same kind of situation at the end of 2019 as the economies of the eurozone: a struggling export sector offset by solid domestic demand. For the whole of 2019, GDP grew by 0.9%, a sharp decline from the 2.8% we saw in dynamic 2018. Note, however, that GDP was negatively impacted by the absence of major sporting events in 2019, unlike in 2018. These have a strong influence on GDP because television rights are paid to companies based in Switzerland. SECO (State Secretariat for Economic Affairs) estimates that adjusted for the effects of sporting events, growth in 2019 amounted to 1.4% (compared to 2.3% in 2018).

Swiss GDP growth

2020: A complicated year ahead

2020 started rather well. Business cycle indicators have all been on the rise and external demand seemed to be picking up. The economy appeared to be somewhat freeing itself from its shackles and had entered a slight rebound phase, which could have led to an increase in annual growth to around 1.4% for 2020.

The spread of the coronavirus will harm growth

Nevertheless, the spread of the coronavirus epidemic and the containment measures taken in China, Europe and Switzerland will harm growth. At this stage, it is extremely difficult to make a forecast, which will depend mainly on the duration of any disruption. Nevertheless, it can be estimated that growth in at least Q1 and Q2 2020 will be affected, probably leading to zero or negative readings in both quarters. As a result, we're expecting growth to be below 1% in 2020, and probably below the 0.9% seen in 2019, despite the positive effect of sporting events. This forecast could be revised downwards if the epidemic extends well into the second quarter, severely impacting tourism and trade, should any major sporting event be impacted.

The SNB could be forced to intervene

Uncertainty linked to the coronavirus epidemic tends to push up the value of the Swiss Franc, as the Swiss currency is considered a safe haven. The EUR/CHF exchange rate fell below the 1.06 mark on 28 February for the first time since 2015. This is a problem for the SNB, which finds itself forced to intervene on the foreign exchange market to deflate the CHF in a context of negative price growth in Switzerland.

So the question is, what can the SNB do if the 'flight to safety' were to continue and other major central banks introduce accommodating measures such as rate cuts? We've said before that we believe the SNB would prefer to avoid cutting its policy rate further which, at -0.75%, is already the lowest in the world. The SNB will probably try to counter an excessive appreciation of the CHF against a basket of currencies, and not only just the euro, as much as possible by intervening on the foreign exchange market. However, should the pressure become too great, we believe that the central bank could be forced to lower its rate to -1%. After all, SNB members have said many times that the rate has not yet reached its lower limit.

This isn't our base scenario right now. But things could change if the economic situation gets worse and the ECB and the Fed take strong measures which would significantly weaken the euro and the dollar against the Swiss franc.

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more