Sweden: How the Riksbank has made the krona’s path to recovery even narrower

EUR/SEK is approaching the April highs, and this is not just a risk sentiment issue. The emergence of dissent within the Riksbank and lower-than-expected inflation figures are leaving the krona without a solid floor. Near-term vulnerabilities remain elevated, and our baseline scenario for a recovery in the second half of the year faces rising risks

Softer data has been helping the Riksbank doves’ case

Against a backdrop of persistent krona weakness, the assumption going into the April Riksbank meeting was that the bank would deliver both a 50bp rate hike and a resolutely hawkish message in a bid to support the currency.

While the bank delivered on the former, the overall messaging was more nuanced. The Riksbank’s closely-watched interest rate projection told us that we’re at or very close to the peak for rates, and the unexpected dissent of two board members (Deputy Governor Anna Breman and Deputy Governor Martin Floden) in favour of a smaller hike, added a dovish spin to what otherwise was a substantial interest rate hike.

The subsequently-released meeting minutes revealed that this dissent wasn’t ultra-dovish per se. Neither Breman nor Floden ruled out further hikes, but both saw signs of cooling inflationary pressure and lower inflation expectations. The data released since the April meeting has largely endorsed that view.

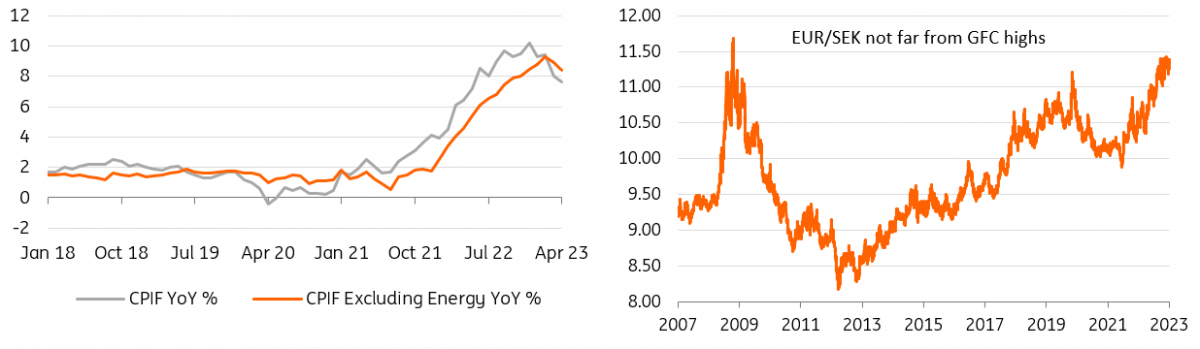

Both core and headline inflation came in below expectations last month, with the core measure (excluding energy) slowing from 8.9% to 8.4%. The highly-regarded Prospera survey of inflation expectations has continued to decline, with CPIF seen at 2.3% in two years and at 2.1% in five years, a 0.1pp decline in both gauges compared to a month earlier. Despite that, Floden (one of two dissenters) noted there’s “still some way to go before we are close to the inflation target”.

On housing – an area where Sweden stands out as being particularly vulnerable – we have seen tentative signs of price stabilisation. But expectations overwhelmingly point to further weakness, while the recent downgrade to junk status for SBB’s debt (one of Sweden’s largest landlords) and subsequent dividend pause was a reminder of the ongoing risks associated with the Swedish property sector given the rise in interest rates.

Sweden CPI and the krona both declining

The implications for SEK are negative

In spite of all that, we don’t think the Riksbank’s strategy has fundamentally changed. The April meeting minutes didn’t show any significant divergence in views on how to tackle inflation. And that means that another 25bp rate hike will likely be delivered as promised – we think probably in June – and that might be followed by more should the data argue for it.

What has changed, however, are the currency implications. New Governor Eric Thedeen has been resolutely hawkish and explicit about needing to support SEK, with some relative success when comparing the krona’s performance against other pro-cyclical peers.

But the April meeting was a turning point for the krona, as we argued at the time. The signals contained within the interest rate projection, the unexpected division within the board, and the subsequent dovish data have all made SEK more vulnerable in the near term.

Hawkish messaging was arguably the Riksbank's primary tool to support SEK, and it’s hard to see that narrative being rebuilt in June, especially if inflation continues to move in the right direction. As Floden himself admitted recently, the Riksbank may want a stronger currency, but there’s not a lot it can do about it.

More SEK weakness might push the Riksbank closer to considering FX intervention, but we have stressed multiple times how threatening intervention seems more likely to us than actually deploying this, given the relatively low ammunition in terms of reserves.

Ultimately, while the Riksbank has sought to stay out in front of the European Central Bank on rate hikes, the reality is that as the absolute level of interest rates grinds higher, the trade-offs involved for the housing market and broader economy are mounting. Policymakers will be hoping that the prospect of Federal Reserve rate cuts on the horizon, coupled with the end of the ECB’s hiking cycle over the next few months, can remove some of the pressure it's currently facing.

More troubles for SEK before a recovery

So where does this leave us with the SEK outlook? We think the krona will remain very highly vulnerable to external headwinds, and even with a recovery in risk sentiment, it may lag other pro-cyclical currencies. Heading into the 29 June meeting, there is now a non-negligible possibility that the Riksbank might pause and delay the promised 25bp hike till September. Much will depend on CPI figures for May, which will be released on 14 June, but our base case is that they will deliver the last hike in June and then pause.

On the back of those significant downside risks in the near term, EUR/SEK may well break through the 11.43 April highs and test the 11.50/11.60 area unless the FX market shifts more decisively in favour of high-beta currencies. Even in that scenario, we think EUR/SEK should still find support around 11.20/11.25 given the Riksbank’s unfavourable narrative for SEK.

In the longer run, we still think that a stabilisation in risk appetite, and a rotation from the dollar to favour European currencies in the second half of the year can help a gradual decline to the 11.00 area in EUR/SEK. But the Riksbank has likely made the path for the SEK recovery an even narrower one.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article