Strong US jobs rebound after winter strikes and storms

- 3 April

- United States

A strong rebound in employment suggests the US economy is in a decent position to weather the economic headwinds from the Middle East conflict. Nonetheless, job creation remains concentrated in a handful of sectors, and rising uncertainty and caution are likely to make employers hesitant to accelerate hiring plans

| 178,000 |

US jobs added in March |

Strong growth, but with a lack of breadth

The headlines from the March US jobs report are good. Non-farm payrolls were up 178,000, well ahead of the 65,000 consensus estimate after a weather and strike-related drop of 133,000 in February. Meanwhile, the unemployment rate unexpectedly dropped to 4.3% from 4.4%. So, as with most of the data from the start of the year, it is a positive surprise and suggests that the US is on a firm footing to take on the economic challenges posed by the Middle East conflict.

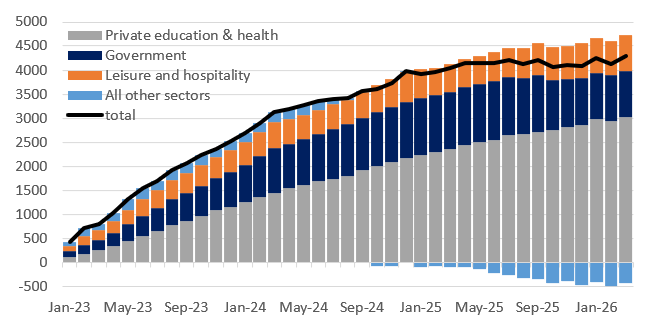

That said, we need to acknowledge that the details within the reports again show the high degree of industry concentration for where jobs are being created. Private education and healthcare posted a 91,000 increase, boosted by the return of Kaiser Permanente's 31,000 previously striking staff. This sector has accounted for 70% of all jobs added since the end of 2022. Then there were an additional 44,000 jobs in the leisure and hospitality sectors, which account for 18% of all the jobs added since the end of 2022. The federal government workforce shrank again, but government in total still accounts for 22% of the jobs added over the same period.

Contributions to cumulative employment gains since December 2022 (000s)

Now, these don’t add up to 100% because all other sectors combined have lost jobs since 2022, underscoring our point about the lack of breadth to job creation. Admittedly, we did see jobs added in retail, construction and manufacturing rise in March, but this may be more down to a rebound post the winter storm disruption that contributed to non-farm payrolls falling 133k in February (initially reported as a 92k drop), rather than a return to outright hiring.

Middle East conflict poses challenges for a stalled jobs market

Despite today’s better-than-expected outcome, there are only 260,000 more people in work today than 12 months ago, implying that the jobs market has effectively stalled during a period when the US growth story was healthy. Our concern is that with the Middle East conflict showing little sign of coming to an imminent conclusion, an overlay of heightened geopolitical, economic and market angst is not going to incentivise business to suddenly start hiring now. In fact, with cost pressures rising and consumer spending power being squeezed by higher gasoline prices, corporate profitability will face more challenges and runs the risk that employers will look to cost containment measures. This threatens weaker payrolls numbers in the coming months.

Next Friday’s March inflation print is likely to show headline inflation jumping back up to 3.4% from 2.4% in February, but with wage growth also slowing, we don’t see the demand impetus that will lead to broad, persistent inflation. Instead, the headwinds to growth and jobs mean that we still see interest rate cuts as more likely than interest rate hikes this year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more