Monitoring Turkey: Strengthening the higher for longer signal

In its first inflation report release of this year, the Central Bank of Turkey (CBT) kept its inflation forecasts unchanged. Newly appointed Governor Fatih Karahan repeated the pledge to maintain a tight monetary policy stance for longer and kept the door open for further rate hikes in case of a marked deterioration in the inflation outlook

Turkey at a glance

- The Central Bank of Turkey (CBT) kept its year-end and 2025 inflation forecasts (which function as intermediate targets in the disinflation process) unchanged at 36.0% and 14.0% respectively. This was the prevailing expectation following the bank’s assessment that, after inflation came in at 6.7% in January, the outcome was consistent with the forecast of the last Inflation Report of 2023.

- Acknowledging inflationary pressures and providing a detailed analysis about the drivers, Governor Fatih Karahan envisaged a transition heading towards a disinflation and stabilisation period. He expects inflation to peak at around 73% in the second quarter of 2024 and for it to adopt a declining trend thereafter.

- The central bank sees the seasonally adjusted monthly inflation rate hovering below 4% on average in the first half of this year (around 3% except for January), then declining to below 2.5% in the third quarter and around 1.5% in the last quarter of this year. This projection implies a strong disinflation path in the second half.

- It also reiterated the pledge for further macro prudential moves in case of any potential excess volatility in credit supply and deposit rates. Given the recent momentum gain in credit card spending due to seasonality at year-end and bringing forward of consumption due to wage hike expectations, the governor mentioned a need for a new regulation.

- Finally, the CBT seems confident about the success of the ongoing disinflation policy as monetary tightening has had a stronger-than-expected impact on pricing behaviour. A further improvement in the current account balance is expected, together with a rebalancing in domestic demand.

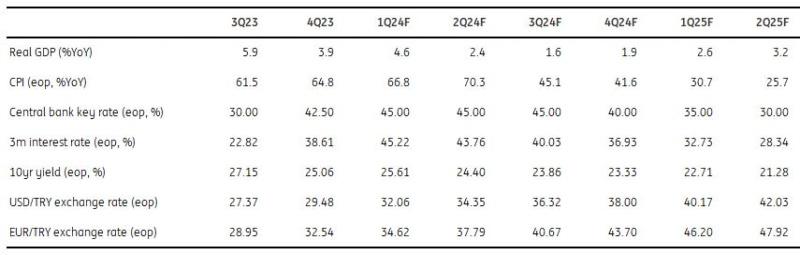

Quarterly forecasts

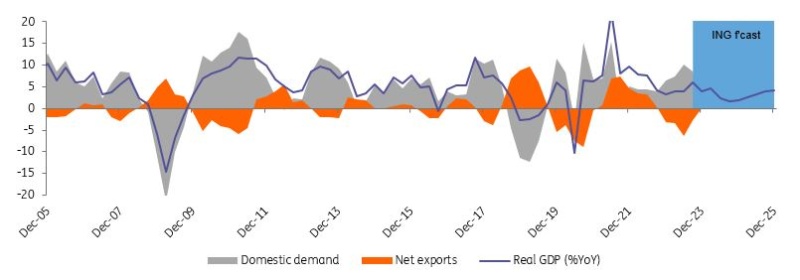

Still solid domestic demand

The recent data flow indicates that the gap between aggregate demand and supply that has led to significant pricing pressures has continued, given signals of weakness in production as indicated by slowing industrial production while domestic demand has remained relatively strong. Since early October, FX loans have adopted an upward trend with more than US$4bn lending as companies have shown an improving appetite for FX borrowing with rising Turkish lira borrowing costs. On the flipside, with high TL borrowing costs (floating in the 50-53% range since November), we see a momentum loss in non-SME TRY commercial lending, as this type of lending in annualised 13-week moving average terms moderated to the lowest level since last August. However, SME lending shows signals of acceleration during this period given i) restrictions on SME FX borrowing, and ii) less sensitivity to TRY borrowing costs due to a less diversified funding base in comparison to large corporates.

Real GDP (%YoY) and contributions (ppt)

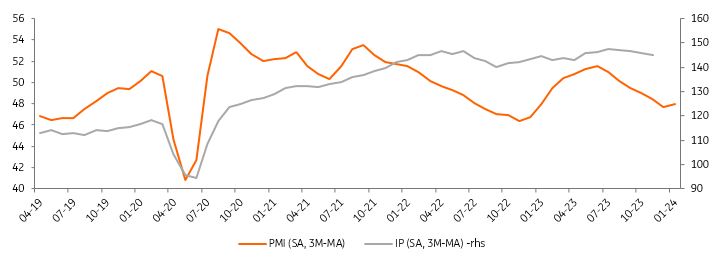

PMI recovered, though still below the 50 break-even threshold

The manufacturing sector PMI – which declined to 47.7 in the fourth quarter of 2023 from 49.5 in the third quarter and supported the view that economic activity is softening – showed a recovery in January to 49.2. However, it has remained in contraction territory since the middle of the last year and pointed out the challenging business conditions across the manufacturing sector.

In the breakdown, the data shows that rates of moderation in output, new orders and purchasing activity all eased in comparison to December, while employment remained unchanged despite a scaling back of purchasing activity and inventory holdings on the back of weaker new orders. Finally, the significant adjustment in the minimum wage contributed to a spike in the rate of input cost inflation in January, while output prices are rising at a faster pace in return.

IP vs PMI

Continuing strength in non-manufacturing activity

Leading indicators of the manufacturing industry reflected that the slowdown in the sector continued in January. Accordingly, capacity utilisation rate dropped by 1.3 percentage points over the previous month to 76.2% on an unadjusted basis, while recording a 0.9ppt fall to 76.4% in adjusted figures. On the other hand, real sector confidence on an adjusted basis recorded a 0.5ppt decline to 102.9, the lowest reading in a year.

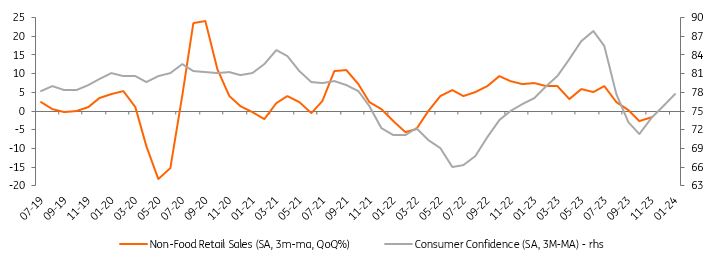

In the breakdown, the general business situation, total employment (next three months), production volume (next three months), and export orders (next three months) were the major drivers of the sequential fall in confidence. Additionally, leading indicators showed that the slowdown in non-manufacturing activity, which spread across sectors in the last quarter, did not deepen further in January. Services and construction confidence increased by 4.0% and 3.3% to 116.8 and 90.9 respectively, while retail trade confidence recorded a 1.0% drop to 115.6.

Retail sales vs consumer confidence

Rising pricing pressures in January

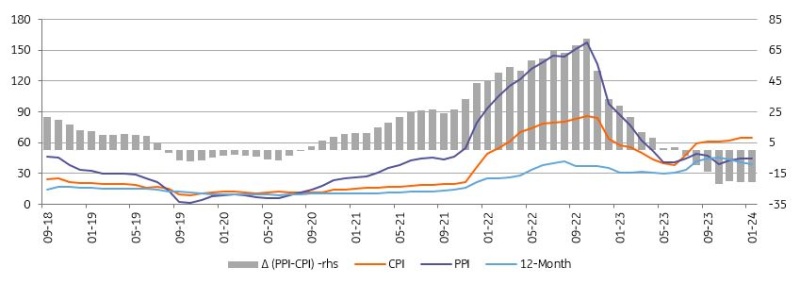

Inflation in January came in at 6.7% month-on-month on the back of non-food and energy prices. While the second-highest January figure in the current series was in line with the consensus, annual inflation inched up to 64.9%. A continued limited slowdown in domestic demand, implications of the minimum wage hike and the rigidity in services inflation were the main factors weighing on the inflation outlook in January. Core inflation (CPI-C) came in at 7.6% MoM, staying broadly unchanged at 70.5% on an annual basis on the back of a deterioration in pricing behaviour, exchange rate developments, adjustments in administered prices and inertia in services. On a seasonally adjusted basis, headline inflation also increased mainly due to services posting significant price hikes – especially in rent, catering and transportation services. Goods inflation was relatively stable.

Inflation outlook (%)

Plunge in January trade deficit

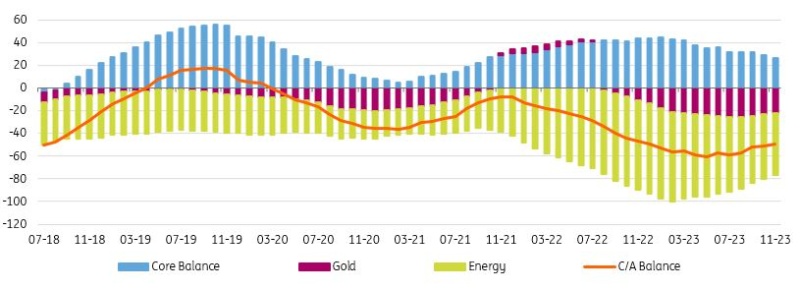

According to the provisional customs data released by the Ministry of Trade, the foreign trade deficit dropped by 56.8% to US$6.2bn in January from the record high level in the same month of the previous year. The breakdown showed i) more than an 87% drop in net gold trade deficit to a mere US$561m, ii) a moderation in net energy trade deficit by 33% to US$2.5bn, and iii) a plunge in the core (excluding gold and energy) trade deficit by 78% to US$474m were the factors that contributed to the improvement in the external balances.

The ratio of exports-to-imports decreased to 76.4% from 79.2% a month ago, while the coverage ratio excluding energy and gold stood at 97.4%. The data implies a likely recovery in the January current account given the large deficit in the same month of last year at US$10.5bn, while providing support to the suggestion that the impact of the current policy framework on the external balances is getting stronger.

Current account (12M rolling, US$bn)

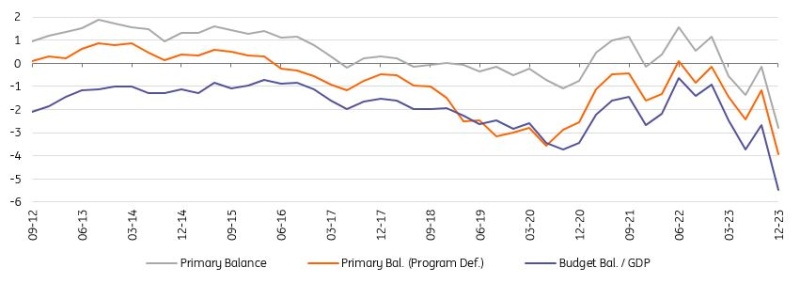

Budget deficit at the highest in more than a decade

The December budget results showed a significant deterioration in the budget surplus compared to the same month of 2022, due to the acceleration in non-interest expenditures attributable to transfers to SEEs and earthquake spending – despite the continued strength in increases for direct and indirect tax collections. Following the December figure, the deficit for 2023 rose to TRY1.38tn, approximately 5.4% of GDP, below the 6.4% projection in the last MTP. On the other hand, according to Treasury and Finance Minister Mehmet Simsek, the earthquake expenditures-to-GDP ratio was 3.7%. Excluding these expenditures, the ratio was 1.7%, below the Maastricht criterion. Minister Simsek pointed out that this relatively favourable outlook in the budget deficit was due to the higher-than-expected revenue collection.

Budget performance (% of GDP)

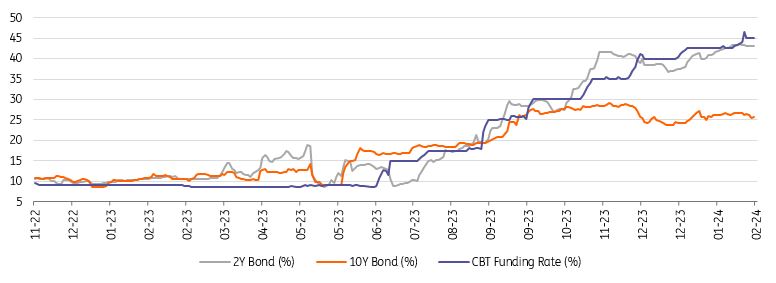

Central bank ends hiking cycle in January

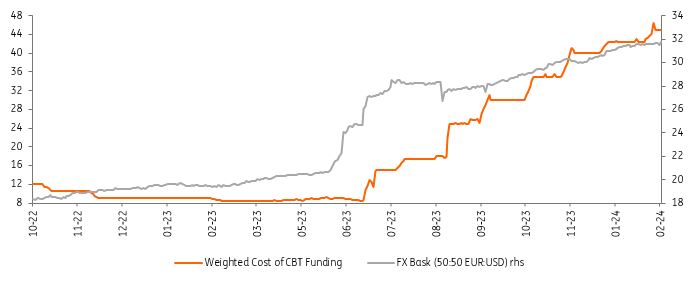

In line with its guidance last month and the market consensus, the CBT raised the policy rate by 250bp to 45% in its first rate-setting meeting of this year. With this move, the bank completed its tightening cycle and switched to a wait-and-see mode. It has, however, remained cautious and ready to act if "notable and persistent risks" to the inflation outlook emerge.

Continuing its hawkish stance, the central bank reiterated it would not start cutting earlier and to “ensure sustained price stability”, remained committed to keeping a tight stance until i) there is a significant decline in the underlying trend of monthly inflation, and ii) inflation expectations converge to the CBT’s forecast range. Finally, since the elections, the CBT has undertaken a number of measures aiming to simplify the macro-prudential policy framework, increase the functionality of the market mechanism and strengthen macrofinancial stability. In its statement, the CBT pledged further moves “in the face of any potential excess volatility in credit supply and deposit rates”.

CBT funding rate (%) vs FX basket

FX and rates outlook

As the central bank has maintained a hawkish stance with a determination to keep rates high and monetary conditions tight, the non-resident interest has improved in recent months. This is also supported by the high carry with the policy rate at 45%, up from 8.5% in May 2023. However, a decline in reserves in recent weeks attracts attention driven by an increase in residents’ appetite for FX on the back of a relatively high level of FX-protected deposits maturing in January. Accordingly, the CBT has come up with policy moves (i.e., adjustments in and remuneration of required reserves) aiming to support deposit rates. A gradual improvement in external balances continues.

While bond yields are high by historical standards following the adjustment after elections (driven by CBT tightening, an end to CBT purchase auctions and easing of security maintenance requirements), the rising inflation path until at least May this year is still a concern that is adversely impacting real returns. We saw US$3.8bn inflows between early November and mid-January, though there has been some weakness lately. Whether foreign inflows continue will be key for the bond market over the coming period.

Local bond yields vs CBT funding rate

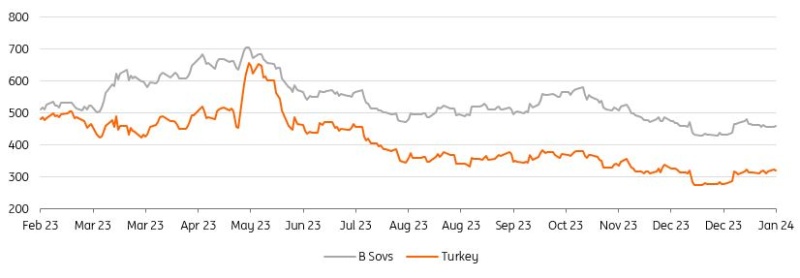

Sovereign credit: primary market action follows central bank change

Despite some uncertainty following the change in governor at Turkey's central bank at the start of February, investor sentiment has been stabilised and boosted by comments that affirmed a hawkish stance and commitment to orthodox policy. At the same time, two key themes we expected for this year – decent external bond supply and positive ratings movements – have started to come to light. Moody's outlook on their B3 rating shifted to positive in mid-January, with the next reviews to come from Fitch on 8 March and S&P on 3 May (with the outlook currently positive).

Last week saw a US$3bn, 10-year Eurobond issue from the Turkish sovereign, along with a debut deal for the Turkish Wealth Fund for US$500m. We expect more supply to come from Turkey, with US$10bn in sovereign issuance currently budgeted for the year. While some political uncertainty and headline risk remains due to upcoming local elections, investor demand should remain well supported by the ongoing positive reform momentum along with light investor positioning.

ICE US$ Bond Sub-Index Spreads vs USTs

Download

Download articleThis publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more