Stars align for eurozone wage growth rebound

A combination of labour shortages, high inflation, and increased minimum wages, means 2022 is set for a decent recovery in nominal wage growth

Everyone in Frankfurt and beyond is looking at the labour market to see whether second-round effects of the current inflation shock are already visible in the data. We, and the European Central Bank (ECB), don’t see evidence of that so far as the ECB’s index for negotiated wages actually reached its lowest wage growth figure in decades in 3Q21 (1.3% year-on-year). If the labour market is a lagging indicator, however, wage developments are the mother of all lagging indicators. Looking ahead, we expect wage growth to significantly accelerate in 2022 and 2023 to around 3.5%, as most important wage growth drivers point to a sharp increase.

Labour shortages continue to rise

The past few months have seen surprisingly rapid declines in unemployment and the economy has recovered quicker than expected, which has resulted in a stronger-than-anticipated labour market rebound. Furlough schemes – key for keeping unemployment relatively low in 2020 – saw a sharp decline in take-up in 2021, even though global supply chain frictions led to renewed demand for furlough schemes in the manufacturing sector. A significant increase in structural unemployment has fortunately not materialised and we now expect unemployment to continue its downward trend in the coming year as employers’ hiring expectations remain very strong for the beginning of 2022.

At the end of last year, we wrote in depth about labour shortages emerging, and since then new data shows that the labour market has tightened further. Vacancy rates are now higher than before the pandemic, while businesses have already indicated that worker availability has never been so problematic for their production as it is right now. In the eurozone, there are still fewer people active than before the crisis, which means that there is still some slack on the fringes of the labour market that could help cushion these problems to a degree – unless people drop out of the labour force for good. In any case, it looks as if labour shortages are set to remain a dominant economic theme of 2022.

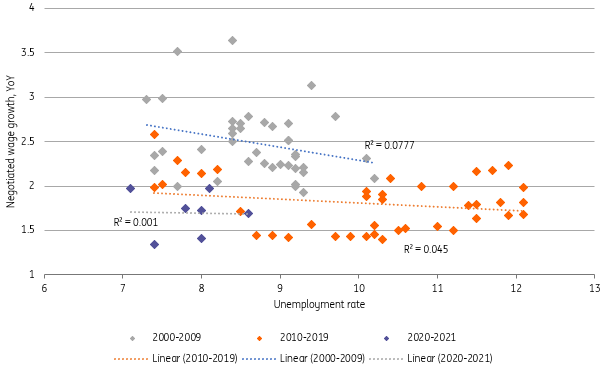

It takes longer for wage growth to emerge from low unemployment and it leads to less wage growth as well

The relationship between wage growth and unemployment has weakened over the past decade, fuelling the debate about whether the relationship between unemployment and inflation – the Phillips curve – is dead. It looks as if the relationship between unemployment and wage growth is still alive, at least, but with a year lag and flatter than seen before. In layman's terms: it takes longer for wage growth to emerge from low unemployment and it leads to less wage growth as well. It’s important to note that the past decade has seen lacklustre employment developments and mild shortages. Now that labour market tightness has become more pressing, it seems logical that this will have more impact on wage growth again. Look back at 2019, for example, when shortages also resulted in a modest run-up in wage growth, which was halted by the pandemic. It is possible that with labour shortages back to pre-pandemic levels, wage growth will pick up where it left off in 2019.

The Phillips curve has flattened over the past decade

Inflation empowers union demands

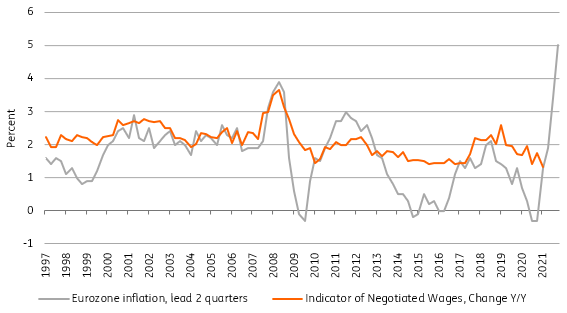

It’s not just labour shortages that point to higher wage growth though. Another key driver of wage growth in the eurozone is inflation, especially since wage-setting in the eurozone is predominantly done through collective bargaining agreements and inflation is an important input used in these negotiations. Purchasing power is currently being squeezed by inflation at its highest level since the 1980s, and negotiated wages in the eurozone have historically followed inflation developments closely.

In some countries, like Belgium and France for example, inflation has a direct impact on wage growth through indexation. Other countries see inflation passed through via higher union demands that, in turn, result in better negotiation outcomes for workers. In the past, unions have either used actual inflation rates or the ECB’s medium-term inflation target in the bargaining process. Both used to be very close to each other. In the current bargaining rounds, expectations are that current inflation rates and the loss of purchasing power will play a more important role than in the past. Labour market shortages are likely to add to the bargaining power of unions, which can prioritise higher wages over job security.

Overall, the relevance of wage settlements depends on how much of a country’s employment is covered by collective bargaining agreements, and in the eurozone, that’s a lot. Also, collective bargaining agreements, centralised or decentralised, have a strong signalling effect on private-sector wage agreements. This results in a strong relationship between overall wage growth and ‘negotiated’ wage growth.

For the eurozone, we find the correlation between negotiated wages and inflation to be the strongest with a two-quarter lead for inflation. This means that wage growth historically trails inflation by about half a year.

Inflation leads wage growth as it is an important driver of wage negotiations

Corporate profits have been strong, allowing for wage growth

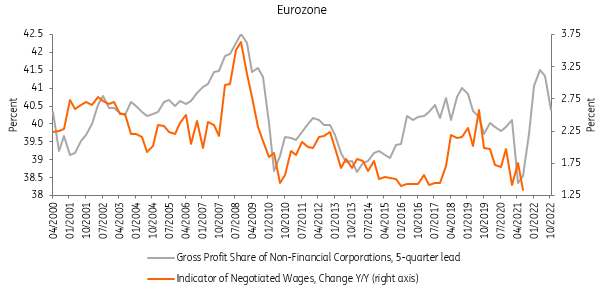

Besides factors such as labour shortages and purchasing power, another important driver of wage growth in the eurozone is whether businesses can afford any salary increases. If corporate profits have weakened, softer wage growth can be expected. However, healthy corporate profits should increase the likelihood of wage increases, sharing corporate profits with employees. The relationship historically shows a five-quarter lag. At the current juncture, corporate profits have shown a particularly strong rebound since the reopening of economies in mid-2020, suggesting ample room for higher labour compensation over the course of 2022.

A high corporate profit share brings room for compensation growth

Minimum wage increases have been generous this year

Another important factor contributing to higher wage growth in 2022 is the sizeable increase in minimum wages in several countries. Germany is the most notable of course, with an expected increase to €12 per hour promised by the new coalition (an almost 30% increase). Other countries have also seen minimum wages increase, such as Portugal with a rise of 6%, while France and Belgium will adjust for inflation, which will result in a sizable jump. The Netherlands has also agreed to increase the minimum wage by 7.5% but will do so in steps over the duration of the government's term. The impact of higher minimum wages works through to the average of course, also because it generally impacts wage categories above the minimum as well.

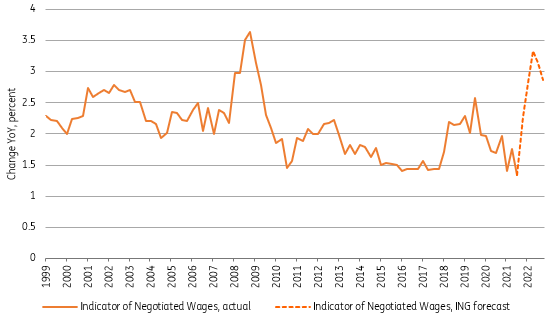

Expect wage growth to rebound to around 3% this year

A simple empirical model that has performed well historically would suggest nominal wage growth will recover to about 3-3.5% over the course of 2022, but relationships in economics are rarely mechanical. We have to keep in mind that Germany has relatively few wage negotiations coming up, which dampens the growth in negotiated wages. Also, a key question is whether unions – whose positions have weakened over recent decades – can convert the better negotiation positions into higher wage growth.

On the other hand, overall wage growth in sectors without collective bargaining already seems to be significantly outpacing negotiated wages in some eurozone markets, although data on this is severely distorted at the moment due to compositional effects in the labour cost index data. Overall, therefore, we think that wage growth of around 3% seems like a fair number for wage growth to rebound to, possibly over the next two years.

We expect wage growth to rise into the 3-3.5% range this year

So, is the Phillips curve alive and kicking then? It seems so, although it looks like it needed supply shock therapy to be revived. The current high inflation is, of course, hardly a result of low unemployment, but will in turn feed through to the wage growth channel which in turn boosts medium-term inflation estimates. It’s very early days, but it looks like the relationship between unemployment and inflation is becoming more significant again.

For the ECB, this will be an important argument for a rate hike in early 2023. For the current inflation spike, policy is not so relevant. The ECB can hardly fill gas reserves or add to the container shortage. What it can do is act on cyclical developments that look favourable, and with an economy recovering quicker-than-expected and wage growth which is set to rebound this year. With inflation expectations around 2%, ECB President Christine Lagarde will have the luxury that former President Mario Draghi never had: hiking interest rates.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

20 January 2022

Higher risks, higher costs, higher wages This bundle contains 6 Articles