Spain: Tourism to drive economic upturn, but the outlook is cloudy

- 12 July 2022

- Eurozone Quarterly Spain

High uncertainty related to the war in Ukraine and soaring inflation are expected to cool down the Spanish economy in the second half of the year. However, the negative impact might be cushioned by government measures and a strong revival of tourism in the third quarter

Things are starting to look worse for Spain

The ongoing war in Ukraine and the erosion of purchasing power due to high inflation are expected to adversely impact economic activity. Households are becoming more pessimistic as soaring inflation bites, with consumer confidence plunging again in June. This could contribute to a slowdown in the economy later this year. However, the latest consumption data for May show no weakening (yet). Business activity is also holding up for the time being. The purchasing manager indices show that both the manufacturing and services sector in Spain weakened in June, although they are still above the 50-mark indicating they have still grown compared to May. The fall in both PMIs was slightly more pronounced in Spain than in the eurozone.

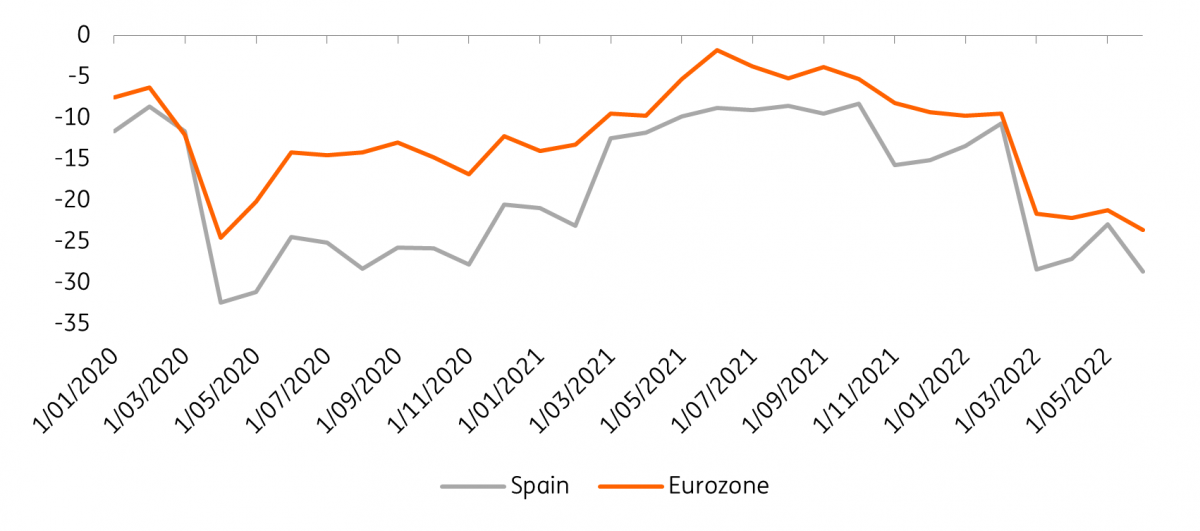

Consumer confidence plunged again in June

Inventory correction and a weakening in export demand are also worsening the outlook for Spain. As part of ongoing efforts to circumvent rising prices and supply chain problems, firms subsequently built up their stocks in the spring, but a weakening demand from autumn is likely to prompt companies to correct their inventories. On top of that, a slowdown or recession among Spain's main trading partners will reduce exports. On the other hand, a strong labour market, a government package to cushion the loss in purchasing power (adding five basis points to the growth figure in 2022 and 2023, according to the Spanish central bank), and a continued recovery of the tourism sector, will help ease the pain.

Since Spain is one of the eurozone members least directly affected by the war in Ukraine, we expect the country to stay just out of recession territory during the coming winter months.

Tourists to the rescue?

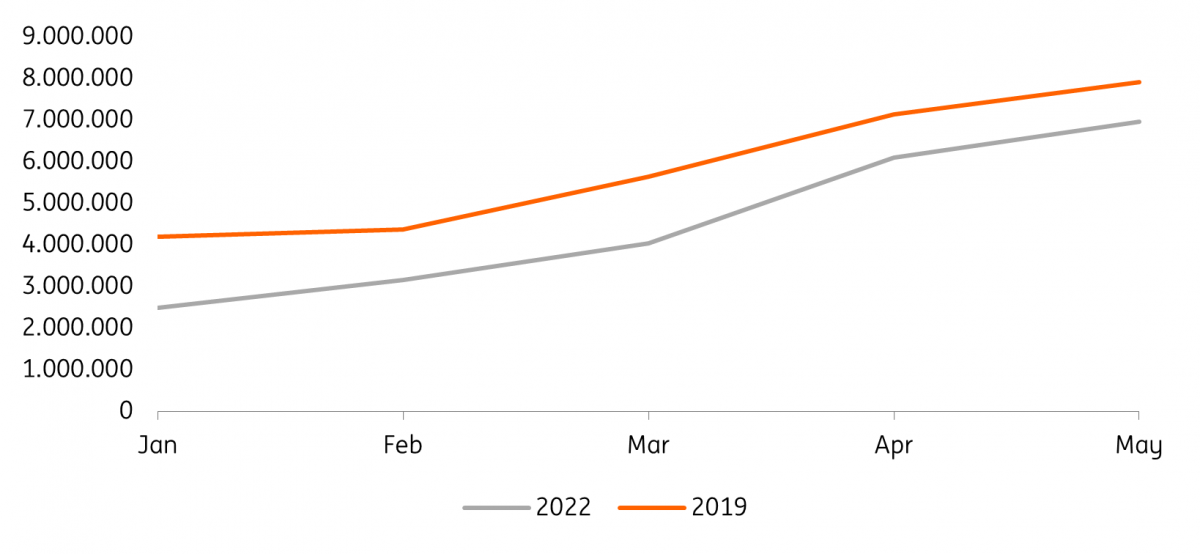

In May, Spain welcomed seven million international tourists, which means it recovered 90% of the international tourists recorded in 2019. Total tourist expenditures are also already at 90% of their pre-covid level in real terms. The elimination of Covid restrictions led to a strong acceleration of inbound tourist flows in the first half of the year, which were at the heart of the solid contribution of the exports of services to GDP growth. We expect that international tourism will continue to recover over the summer months, although soaring inflation might start to slow tourist activities down. As tourism is a key economic sector in Spain, contributing 14% of total GDP in 2019 according to the World Travel and Tourism Council, a continued recovery is a substantial factor underpinning economic growth.

International tourist arrivals

Higher inflation is hitting demand

In June, consumer prices rose by 10.2% year-on-year (HICP inflation 10%) from 8.7% in May, bringing inflation to its highest level since 1985. More worrying was that core inflation was also up again, from 4.9% in May to 5.5% last month. Looking ahead, the introduction of the Iberian mechanism to cap gas prices for electricity production, and a package of government measures including a VAT tax cut on electricity, are expected to cushion inflation in the second half of 2022. However, the impact will be reversed completely in 2023, which has led us to increase our inflation forecast for next year to 3.1%. Although business surveys indicate that inflationary pressures are easing somewhat, elevated price pressures are likely to persist in the near term at least. As total input costs rose again at an elevated level in June, this will lead to other rounds of price mark-ups in the months ahead. Until now, market demand was sufficiently resilient to absorb higher prices, but this now seems to be turning around as household budgets are increasingly under pressure. If these second-round effects materialise, this is expected to substantially slow down consumer spending over the next few months.

Spain’s job market improves, helped by labour market reform

There has been strong employment recovery in Spain. In June, registered unemployment stood at its lowest level since October 2008. June 2022 also recorded the largest increase in new jobs since 2005, albeit the start of the summer season traditionally prompts growth in temporary employment. The largest increase was recorded in the hospitality industry which is still benefitting from the elimination of Covid restrictions. A mix of domestic reopening tailwinds and a recovery of tourism will support employment growth in the second and third quarters of 2022. Employment expectations have also held relatively firm since the onset of the war. In June, jobs continued to be added with capacity constraints persisting and backlogs still elevated. However, we expect this trend to be reversed in 2023.

Current headwinds to economic growth are mounting and will adversely impact employment next year. Although the recent labour market reforms initiated in Madrid improved the proportion of permanent contracts relative to temporary ones, the swings in unemployment rates might be more pronounced than in other eurozone countries as the share of temporary contracts still exceeds the eurozone average. Nevertheless, we expect the impact on the labour market to be moderate unless the outlook deteriorates further.

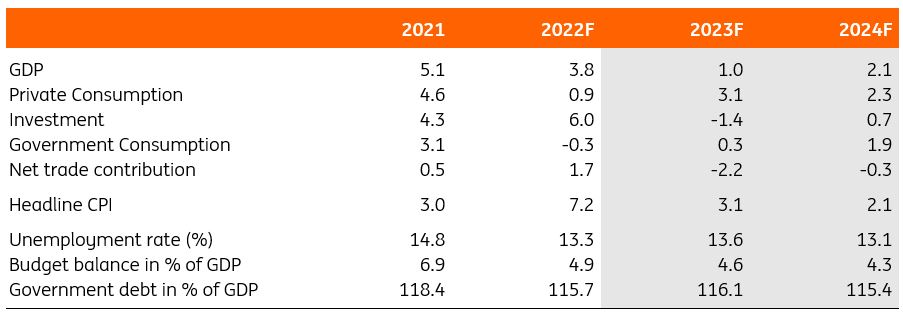

All in all, the reopening of the economy and recovery of tourism supported growth in the second quarter, but the outlook is cloudy for Spain. For 2022 and 2023, we expect 3.8% and 1% economic growth, respectively.

The Spanish economy in a nutshell (% YOY)

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Eurozone Quarterly: This is going to hurt

- This bundle contains 11 Articles