Spain: sustained growth amid shifting drivers

Post-Covid growth in Spain was fuelled by strong service exports, population growth, and government consumption, despite a challenging inflationary and restrictive monetary policy environment. Looking ahead, Spain's economic growth drivers are expected to shift to private consumption and investment as credit becomes more affordable

Spain has emerged as a key driver of economic growth in the eurozone since Covid-19. After experiencing one of the deepest downturns during the pandemic, with GDP plummeting 22% below pre-Covid (4Q 2019) levels in 2Q 2020, Spain has achieved one of the strongest recoveries in the eurozone. The Spanish economy now stands 6.7% above pre-Covid levels, compared to the 4.7% growth at the eurozone level. Moreover, Spain is on a globally aspirational growth trajectory, having expanded by 4.3% since January 2023, closely matching the US economic growth rate of 4.5%.

Post-crisis growth in Spain was fuelled by strong service exports, population growth, and government consumption, despite a challenging inflationary and restrictive monetary policy environment. Looking ahead, Spain's economic growth drivers are expected to shift to private consumption and investment as credit becomes more affordable. We forecast 2.2% growth for 2025 in a challenging eurozone environment, exceeding the expected growth for the region.

Strong service exports, population growth and government consumption fuelled post-Covid growth

It's no surprise that tourism is vital to the Spanish economy, contributing 12.3% to GDP in 2023. This growth continues, with a record of 88.5 million international tourists in the first 11 months of 2024, a 10.6% increase from 2023. Non-travel services like business services, transport, telecommunications and IT also grew significantly in 2021 and 2022, by 16.1% and 28.9%, respectively, reflecting a global shift towards a more service-oriented economy. Moreover, Spain still has room to grow in this area, as the share of non-travel services in GDP was 1.7 percentage points below the euro area average in 2021, according to the Bank of Spain.

Spain’s population dynamics also played a significant role in its economic recovery. Between October 2019 and July 2024, the population aged over 15 grew by 5.6%, compared to the eurozone’s growth of 2.61%. The non-EU foreign population in Spain grew significantly, increasing by 40.57%, driven by government policies that facilitated the regularisation of non-EU foreigners, eased student-to-work visa transitions, and introduced the digital nomad visa, attracting more foreign talent. As a result, the evolution of Spanish GDP per capita appears relatively less impressive than overall GDP, having grown 3.5% since the third quarter of 2019, slightly above the eurozone's growth rate of 2.9%.

Meanwhile, government expenditure increased to support the economy during the Covid crisis and has since continued to grow above its pre-Covid trend, rising to 45.5% of GDP in 2024 from 42% in 2019. The debt-to-GDP ratio remains around 102.8% in 2024 and is decreasing thanks to strong GDP growth and increased tax revenue collection, partly due to fiscal drag. However, caution is needed to ensure this fiscal drag does not become a true drag on the economy in the future. Total government revenue increased from 39% of GDP in 2019 to 42.5% by the end of 2024.

Monetary policy easing will benefit Spanish households

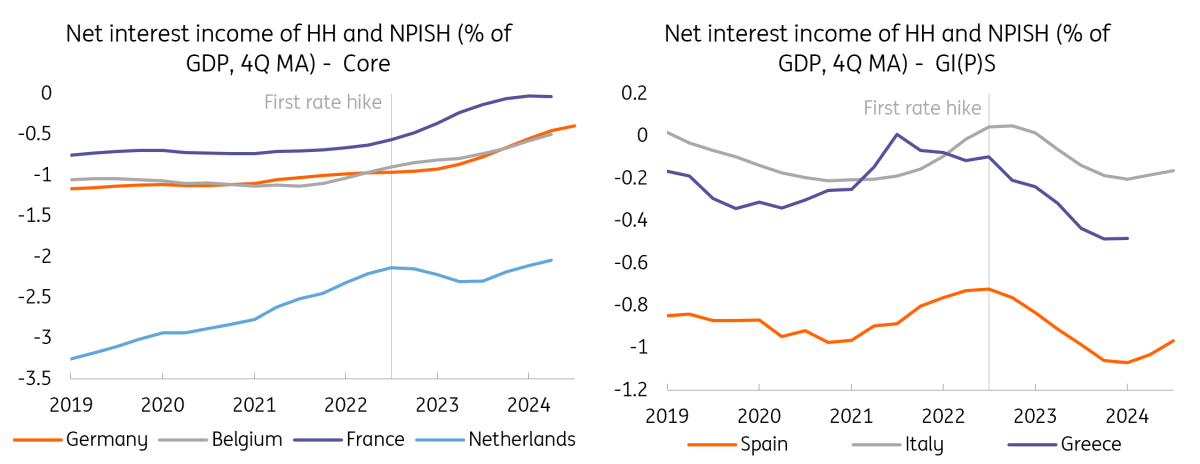

Spain's strong growth is remarkable given the challenging inflationary environment and restrictive monetary policy. This policy has disproportionately impacted households in southern European countries like Spain (see figure below). Compared to households in core European economies, Spanish households experienced a decline in net interest income – the difference between interest received on assets (such as deposits) and interest paid on liabilities (such as home loans) – while it increased in core economies.

Spanish households were, for instance, relatively more exposed to interest payment increases on mortgages due to a high share of variable-rate mortgage loans compared to fixed-rate ones. With the European Central Bank's continued monetary policy easing, we expect this trend in net interest income to reverse, which will benefit Spanish households.

Monetary policy easing will affect households differently within the eurozone

Private consumption and investment will push growth going forward

The impact of monetary policy easing, a high savings rate and a robust labour market are all expected to push up household consumption in 2025, a trend that started in the last quarters of 2024. Household consumption smoothing after recent rises in real disposable income pushed the household savings rate to 13.1%, five percentage points above its pre-Covid level. Meanwhile, the unemployment rate reached 11.2% in 2024 and is expected to decrease to 10.7% in 2025.

More affordable credit along with the allocation of EU recovery funds will also benefit private investment, especially in the construction sector. Spain is set to disperse the majority of the EU’s recovery funds over 2025 and 2026, where infrastructure investment will benefit the construction sector. The Spanish construction industry, which contracted by 25% between 2019 and 2022, has begun to recover and is expected to continue growing in the coming years. The issuance of residential and non-residential permits is on the rise, and Spanish builders are optimistic about their order intakes.

Headline inflation continues to ease

Despite higher headline inflation readings at the end of 2024, underlying inflationary pressures are easing, setting the stage for more subdued inflation moving forward. We expect headline inflation to decrease and stabilise around 2.2% in 2025. Upward risks include rising energy prices and the potential inflationary impacts of US economic policy under the new Trump administration.

For Spain, however, this impact is likely to be small due to its lower exposure to the US compared to the EU. In 2023, Spain's exports to the US were equivalent to 1.26% of its GDP, and imports were 1.64%, whereas the overall EU exposure was 2.9% for exports and 2% for imports.

The Spanish economy in a nutshell (%YoY)

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

EurozoneDownload

Download article

23 January 2025

Eurozone Countries Outlook 2025: Europe’s running out of road This bundle contains 12 Articles