South Korea: Corporate debt is a concern for the economy

A series of recent credit events in Korea is a major concern for the economy. We don’t see a credit crisis as the base case scenario, but as market jitters continue, some losses are inevitable and project financing is the area of greatest concern

Recently, the corporate bond market has experienced a crunch triggered by the default of a municipality-guaranteed asset-backed commercial paper (ABCP). As the global economy faces headwinds and liquidity conditions are expected to become tighter, difficulties in corporate bonds and credit markets are expected to increase. The key is how quickly the authorities and industries can calm the market’s unnecessary unrest. Credit spreads are expected to widen further and small losses in specific sectors are foreseeable, but it is unlikely this will lead to large-scale insolvency of the corporate bond market.

Recent market development in the credit market

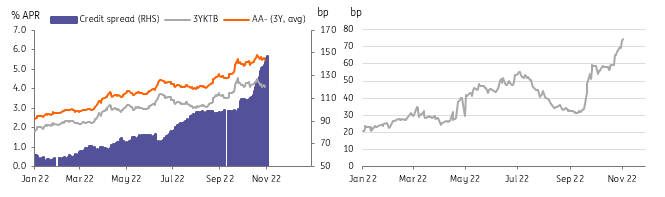

The credit market has been struggling quite a bit over the past few weeks. The 5Y Credit Default Swap had remained low through the year but has almost doubled since mid-September (74.3 as of 4 November vs 31.4 as of 9 September). In addition, credit spreads between 3Y Korean treasury bonds (KTB) and AA-credit widened quite sharply from 96.9bp on 1 September to 147 on 4 November. Global monetary tightening has had a negative impact on the Korean credit market since the beginning of the year, but the recent volatility is due to specific domestic issues.

The credit spread has widened quite sharply since October

What’s going on in Gangwon-do?

The province of Gangwon-do (GWD) announced last month that it would withdraw payment guarantees for a project financing (PF) ABCP worth 205 billion won. Since then, there have been signs of a liquidity crunch across the bond market. So what happened in GWD?

GWD established a real-estate developer called GJC in 2012 for the region's Legoland construction project. The GJC’s special purpose company (SPC) issued an ABCP for which the payment was ultimately guaranteed by the GWD municipality. But when the principal payment was not made as scheduled by the end of September, the municipality decided to file a rehabilitation application for the GJC with the court instead of making the payment.

Why did it do this?

The market has interpreted this move as the municipality acting according to the policy change following the change of local government, rather than because it was unable to make the payment.

Consequently, credit rating agencies took immediate action. The ABCP’s rating of A1 was downgraded to D within five days. It literally went bankrupt. Creditors demanded GWD repay the loan through the issuance of municipal bonds. In the end, the governor of GWD announced that it would repay the loan of 205 trillion won through a special budget by next January, but as market jitters continued, it brought forward the payment plan to December.

The case is almost resolved, but the effects are longer lasting

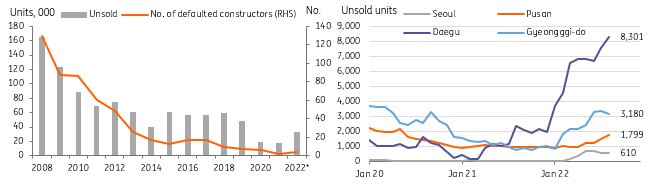

To make a long story short, the municipality will ultimately make the payment as promised. However, this issue was strong enough to shake the entire credit market. Developers are experiencing difficulties due to a deterioration in profitability in the aftermath of the global interest rate hike and rising construction costs due to surging raw material prices. As the number of unsold residential units increases rapidly, overall investor sentiment has frozen. The bankruptcy of ABCP caused by a local government has expanded the possibility of a chain stoppage of the PF loan market and the possibility of a contraction in the financial market.

Recent debt increase was driven by electricity/gas and construction industries

The average debt ratio of Korean companies has been continuously decreasing since 2015. The debt ratio of all-industry fell from 105.6% in the first quarter of 2015 to 91.2% in the second quarter of 2022. Yet, the debt of the electricity/gas industry increased sharply to 228.7% this year in response to their operating losses. Their bonds get AA-grade (Fitch rating) with government guarantees, so a sudden increase in debt itself is not considered risky but it is blamed for crowding out the entire credit market. We expect new issuance of those companies to decline next year thus the crowding out effect is expected to reduce.

On the other hand, the debt ratio of the construction sector showed an upward trend in 2022 but fell sharply from 210.5% in 2015 to 135.6%. As such, even if we foresee some defaults in construction, the estimated damage should be smaller than in the past.

Electricity/gas industry debt rose sharply in 2022

Cloudy outlook for the construction industry

The construction industry's debt level has been managed relatively well, but we have caught signs of insolvency coming to the surface. First, the number of defaulted construction companies has picked up this year. In the first half of the year, four local companies went bankrupt. This is a relatively small number, but we expect it to increase based on a strong forward-looking indicator – the number of unsold units outside of Seoul, which is rapidly rising. We are not concerned about large builders as they have a relatively strong financial structure and sufficient cash reserves. However, we believe small and medium-sized local builders will experience a capital crunch if market liquidity continues to shrink.

Cloudy outlook in residential construction

Project financing is still the concern

Korea has already suffered from PF insolvency once between 2011 and 2013. Project financing has more than quadrupled compared to 2013 as investors have sought higher returns amid the continued low interest rate environment. Although the scale has grown, the composition of funding sources has changed. According to a report by the Bank of Korea, the PF loan balance stood at 112.2 trillion won as of 2Q22, which is higher than 76.5 trillion won in 2008 and 35.2 trillion won in 2013. Most notably, while PF exposures of banks declined in 2022 compared to 2008, the exposures of insurances, and capital/credit increased sharply. Banks have applied stricter conditions on PF, and most of the funds have been invested in large residential construction projects – considered high-quality assets. As the exposure of insurances has risen sharply, it is a worrying fact, but fortunately, their PF projects are also concentrated in high-quality assets. The biggest concern is that investments of capital/credit, savings banks, and securities are small-sized, non-residential, and risky assets. But the total size is relatively small, thus the expected damage should be contained.

Insurances have the largest exposure to project financing

How have government authorities responded to this credit event?

With market volatility growing fast and credit conditions tightening sharply, authorities have announced a series of policy measures including a special liquidity supply package of more than 50 trillion won. Measures include:

- The government will double the ceiling of its corporate bond-buying facility operated by special state-owned banks to 16 trillion won (vs 11 trillion).

- Commercial paper issued by securities firms will be included in the facility’s purchase list.

- The Korea Securities Finance Corp will supply an additional 3 trillion won of liquidity for securities firms experiencing liquidity shortages. In addition, the government reiterated that all municipalities would fulfil their payment guarantee obligations. GWD announced that it would complete its debt obligations by 15 December, earlier than the originally proposed date of January 2023.

How did the Bank of Korea respond to this credit event?

The Bank of Korea (BoK) has also eased some of its micro-policy measures:

- The central bank will temporarily (for three months starting on 1 November) accept bonds issued by banks and nine state-owned companies such as KEPCO and KOGAS, as eligible collateral for banks borrowing money from the bank. Currently, the BoK only takes KTBs, monetary stabilisation bonds (MSB), and government-guaranteed bonds as collaterals.

- The plan to raise the liquidity coverage ratio (LCR) from 70% to 80% will be postponed by three months to May 2023.

- The BoK will carry out a temporary repo (until the end of January 2023) with an estimated amount of 6 trillion won.

As long as the current situation does not shake the entire credit market, we believe that the Bank of Korea will not inject liquidity directly into the market as it would go against the current tightening policy stance. Thus, options like reactivating special purpose vehicles (SPV) to purchase corporate bonds and commercial paper and unlimited repo are not going to be delivered any time soon.

The Bank of Korea’s monetary policy outlook

In the short term, the BoK is expected to raise its policy rate by 25bp in November as inflation is still above 5% and upside risks remain. By doing so, the BoK’s commitment to price stability can continue to be communicated to the market, while the BoK also needs to calm the market’s anxiety about the recent credit market squeeze. That’s why we see a low probability of a 50bp hike in November.

For next year, taking into account ING’s recent house view that the Federal Reserve’s hike will be extended to the first quarter of next year with an additional 50bp hike, we have changed our view about the Bank of Korea's next steps, and now believe it will make an additional 25bp hike in the first quarter of next year. We have also advanced our rate cut call from 4Q23 to 3Q23. Given the tight liquidity conditions with a minimum of 50bp more hikes, a meaningful negative impact for households and businesses is inevitable. Beyond the first quarter, inflation is expected to fall below 4%, then the BoK will shift its policy priority from inflation to growth and financial sustainability. With a bleak growth outlook for 1H23, we believe that the BoK will begin its easing cycle in the second half of next year.

GDP outlook

We have already forecasted that consumer spending will turn negative this quarter as the debt service burden weighs on private consumption and consumer sentiment deteriorates further. Now, we foresee investment contracting over the new few quarters. We don’t see a credit crisis as the base case scenario yet, but as market jitters will persist for a while, business sentiment and market conditions will certainly have a negative impact on the economy. Corporate bond yields and bank lending rates are good forward-looking indicators for investment, and the recent tight credit conditions will likely lead to a slowdown in future investment.

The economic slowdowns in the US, EU, and China are also expected to be longer and more severe, and external conditions will be unfavourable for Korea’s exports during the first half of next year. As a result, we expect three consecutive quarters of contraction from the current quarter, and the anticipated rebound in 3Q23 will be smaller than we had expected. Thus, we are downgrading our 2023 GDP forecast to 0.6% year-on-year from 0.7%, already lower than the market consensus of 1.9%.

Investment is expected to contract in the coming quarters

We expect GDP growth to contract for the next three quarters

Expect a recession, not a crisis

With authorities’ swift responses, expectations of a crisis in the market are expected to subside. Regarding the redemption issue of insurers, we believe that insurers can manage and mitigate risks. While insurance companies will pay high costs for funding, solvency and the ability to raise capital are not at risk. In addition, authorities have already begun consultations with insurance companies and, if necessary, are seeking policy help to alleviate the short-term money market tightness.

However, even after this, the soundness of companies is in question for the next couple of quarters. As always, a crisis always begins with a crack in the economy’s weakest point. Looking at corporate debt, it is judged that the overall debt level of Korean companies is still good, but the status of some selective parts, such as project financing and construction, is worrisome.

Authorities have provided a series of relief measures and expect additional mitigation measures to be introduced. These efforts will likely allow time for businesses and authorities to manage the risks in the hope of more orderly restructuring and a soft landing. We don’t think the credit crunch will pose a systemic risk to the financial system because corporate’s debt condition has improved on average compared to 2015 and most of them are already in risk management mode. But, this will hurt near-term growth and drag the economy into recession next year.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article