Short-term SEK upside possible on Riksbank meeting this Thursday

We believe the Riksbank is likely to push back the date of its next rate hike on Thursday, but fundamentally we don't think the central bank will do away with its hawkish bias completely. That could be a short-term SEK positive, although in the longer term we remain bearish on the currency

The Riksbank meets this Thursday, and the key question is whether policymakers continue to signal a rate hike later this year or early next.

The deterioration in the domestic dataflow suggests the timing of the next rate hike will get pushed back again. But equally, we expect the central bank to retain its hawkish bias - particularly given the ongoing weakness in the Swedish Krona (SEK).

Policymakers may still signal a rate hike over the next six months or so, although given the downside to domestic data and wage growth, we aren't convinced this will ultimately materialise. We expect interest rates to remain on hold in Sweden for the foreseeable future.

Here's an update on the economic outlook and what this week's meeting might mean for the currency.

The labour market is weakening - or is it?

At face value, the Swedish jobs market appears to be deteriorating rapidly. The unemployment rate has surged to 7.4% in seasonally-adjusted terms, while there are early signs that the total number of people in employment is falling.

However, since the last jobs report, the Swedish stats office has suggested that the most recent numbers may be misleading. The agency said recently that "unemployment for September is overestimated and employment is slightly underestimated". That probably means policymakers will take this data with a pinch of salt.

On a more structural level, unemployment rates are much more elevated among workers born outside of Sweden (17.7% vs 4.4%). This follows higher immigration flows in recent years, and Riksbank policymaker Ohlsson has argued would be best helped by labour market policy as opposed to interest rates.

Global central banks dovishness unlikely to faze Riksbank

There has been a noticeable dovish shift in global central bank policy, and in times gone by the Riksbank may have followed suit. But this time looks a little different.

Governor Ingves has argued that the inflation situation is different in Sweden compared to the Eurozone. More importantly, SEK has continued to weaken, and this is causing a little unease among some policymakers. Deputy Governor Martin Flodén has argued ‘’a further depreciation of the krona would lead to unnecessary volatility and uncertainty over the development of the exchange rate and, ultimately, the entire Swedish economy’’.

If nothing else, this suggests that policymakers are more relaxed about the prospect of currency strength, which tells us that ongoing global central bank dovishness is unlikely to be a trigger for rate cuts in Sweden just yet.

Wage negotiations pose risk for inflation outlook

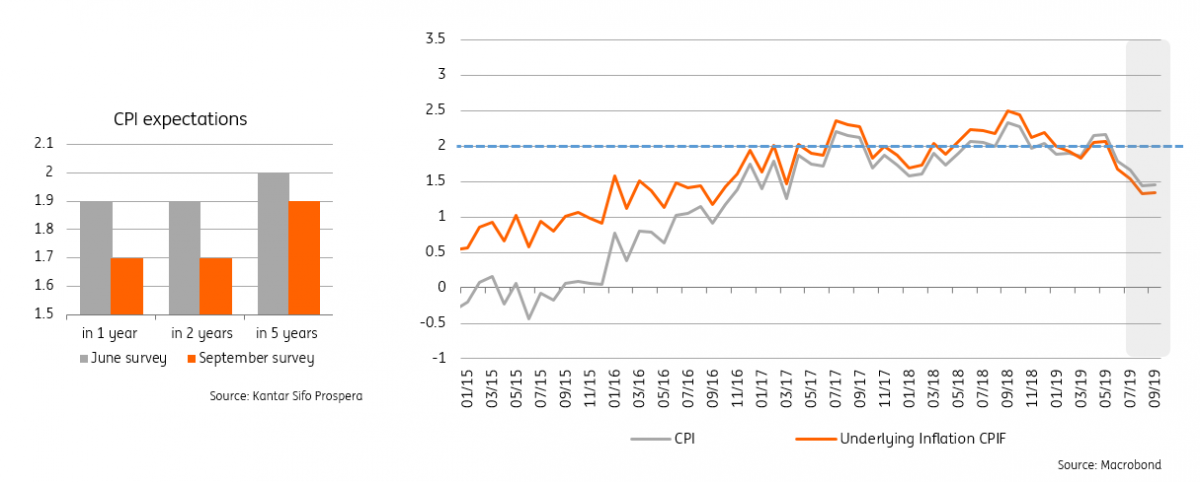

Inflation has been a tad below the Riksbank's most recent projections, although energy base effects are a key factor. Electricity prices were elevated at the same last year because of warm weather and the resulting lower reservoir levels.

That won't faze the Riksbank, but what might are declining inflation expectations - both at the short- and long-term horizons.

In particular, we'd highlight that price expectations have also slipped among employees' and employers' organisations. That could mean that the crucial wage negotiations over the next few months could provide a more lacklustre outcome.

This could add downside risks to the Riksbank's inflation projections, given that the most recent monetary policy report pointed to higher wage growth on the back of higher productivity growth.

Abysmal leading indicators

The most significant development since the last meeting is arguably that both the services and manufacturing PMI have broken below the key 50 level.

The service PMI highlighted a significant fall in the new orders component, along with a tightening in delivery time and a fall in order backlogs in both the manufacturing and service sectors.

None of this bodes well for production, and other survey indicators also point to further weakness ahead. The latest NIER survey was entitled “consumers expecting increased unemployment”, which also saw the service-sector indicator slip back during September. The closely-monitored consumer confidence indicator is at its lowest since December 2012.

FX: Short term upside to SEK assuming the Riksbank doesn't turn dovish

The quality issues issue with the labour market data suggests that the Riksbank is unlikely to meaningfully change its cautiously-hawkish bias this week. Policymakers are still likely to pencil in a rate hike over the next six months, albeit the timing will likely be pushed back from the turn of the year and further into 1Q/2Q20.

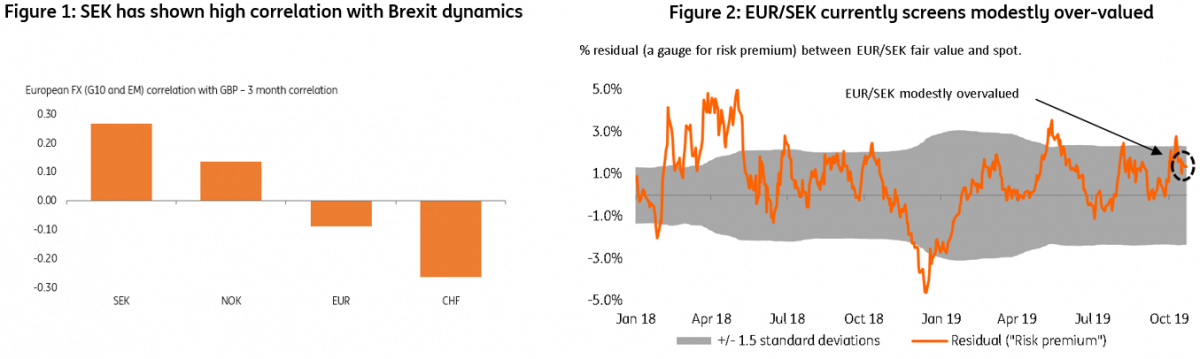

This suggests there's limited downside to SEK, particularly when the global environment shows some tentative signs of improvement (the decreasing probability of a 'no deal' Brexit and the falling odds of an imminent escalation in the US-China trade war). As Figure 1 shows, EUR/SEK currently exerts the highest correlation with GBP within the European G10 FX space, which in turn means it can benefit from the pound's rally.

With EUR/SEK showing some modest signs of over-valuation on a short-term basis (as shown by the cross’ deviation from its short term financial fair value – Figure 2), the krona downside from the upcoming Riksbank meeting is fairly limited. If anything, risks are skewed to some modest appreciation should the Riksbank stick to its hawkish forward guidance – albeit investors are unlikely to fully buy-in to the rate hike signals.

However, beyond the potential support for SEK this week, we continue to reiterate our bearish view on the currency and look for EUR/SEK to reach 11.00. Global economic and trade growth is likely to remain soft, and the uncertainty about the US-China trade conflict will remain in place.

The expected growth divergence in 2020 (slowing major DM economies but a rebound in battered EM economies – Figure 3) also doesn’t point to a positive SEK outlook. From the point of view of cyclical currencies such as SEK, the slowing in developed economies and the recovery in stressed EM countries (from low levels) is not the best recipe for a risk rally. It is usually a rebound in DM growth that positively spills over into the EM growth (and thus lifts overall global growth), rather than the other way around.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article