Services lead Hungary’s economic recovery

Hungary’s Statistical Office confirmed the quarterly GDP growth in the first quarter of the year, with growth driven by services-related consumption. We believe the economy is back on a sustainable recovery path after several quarters of zigzagging

| 0.8% |

GDP growth in Q1ING forecast 0.7% / Previous 0.8% |

| Better than expected | |

Growth structure points to a more sustainable recovery

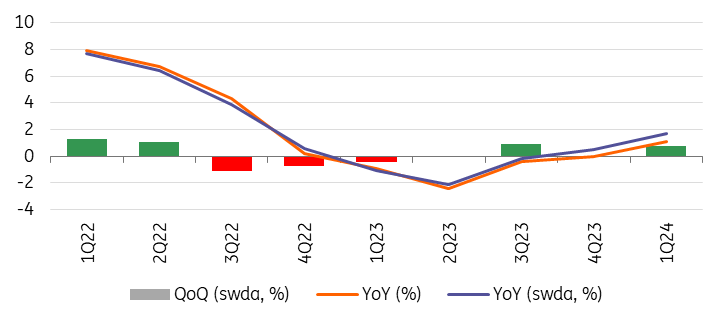

The Hungarian Central Statistical Office (HCSO) didn’t make any revisions to the flash release and confirmed that the Hungarian economy grew by 0.8% in the first quarter of 2024 on a quarterly basis; the year-on-year index remained at 1.7% according to the seasonally and calendar-adjusted data. So, the economy has once again emerged from stagnation, and we believe that this time, it will be more prolonged as its growth structure suggests the current recovery may be more sustainable.

Hungarian GDP growth

Services sector is the main driver, while industry still struggles

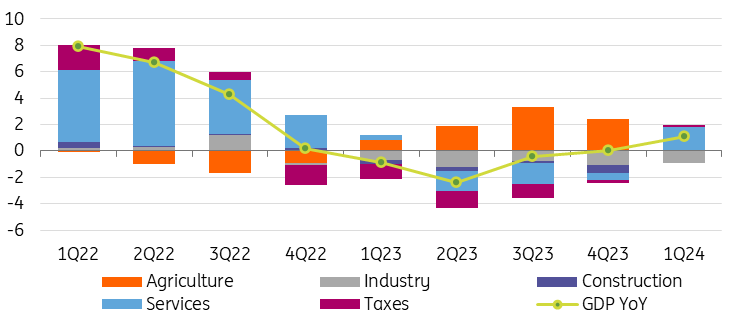

On the production side, the agricultural sector was the main drag on economic performance, as expected. It posted a double-digit decline on a quarterly basis (QoQ). Somewhat surprisingly, the industrial sector recorded a decline of only 0.1%, probably due to the exceptionally low base in the fourth quarter, from which the value-added share didn’t decline any further.

In contrast, the 1.1% growth in value added in construction was a notable surprise, as it wasn't clear at first glance whether the rather technical growth in the production data would be reflected in the value-added data for GDP. In the services sector, the growth of 1.7% QoQ was mainly driven by consumption-related areas such as wholesale and retail trade, accommodation and food service activities, and leisure/recreation-related services. The volume of value added in logistics declined, in line with the difficulties in the industrial sector.

Overall, the growth in real wages and purchasing power and the gradual improvement in consumer confidence have boosted the services sector for two consecutive quarters. It is also evident that households are allocating a greater share of their spending to ‘experiences’ (purchases of services) than to products which, in turn, explains the weakness in demand for industrial goods. In fact, the share of household spending on durable goods was only 6.7% in the first quarter of 2024. A lower first-quarter share was last seen in 2017. It is important to note that the import content is highest for durable goods. Therefore, low demand in this segment partly explains the subdued import performance.

Contributions to GDP growth

Production side (% YoY)

Agriculture showed modest growth in the first quarter compared to last year's extremely high base in terms of year-on-year performance. Industry, including manufacturing, contracted by almost 5%, while construction made a positive contribution on the back of last year’s low base. Services grew strongly, with both business and government-related services and household services showing positive changes. In the former, information, communication and education were the main drivers. The significant growth in education services is likely to have been driven by wage settlements.

Meanwhile, the value-added of accommodation and recreation services may have increased in the context of higher household consumption. Wholesale and retail trade, on the other hand, still contracted by 3% on an annual basis, suggesting that improving consumer confidence is not a panacea.

Household consumption on a recovery path

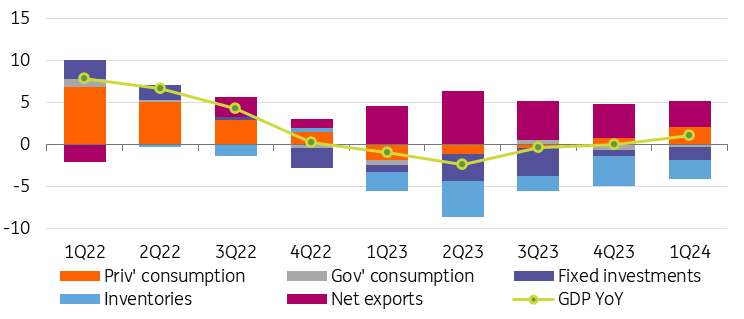

On the expenditure side, it is not surprising that household final consumption grew by 0.6% on a quarterly basis, mainly driven by the increase in social transfers in kind. Government consumption grew significantly in the first quarter of this year as the budget was tightly controlled in the fourth quarter of last year, resulting in a lower base.

The slump in investment was a noticeable drag on economic performance in the first quarter, but this should come as no surprise given the detailed investment report released earlier by the HCSO. Inventories are likely to have fallen on a quarterly basis, which could explain the only minimal decline in goods exports despite the weak industrial performance.

As households tend to buy experiences rather than products, imports of economic services increased, likely partly related to tourism, while weak demand for industrial goods significantly curbed goods imports. In addition, declining energy consumption probably allowed for a moderation in goods imports. Altogether, this has resulted in a higher net export contribution compared to our baseline forecast.

Contributions to GDP growth

Expenditure side (% YoY)

Again, turning to the year-on-year indicators on the expenditure side, domestic demand fell by almost 3% in the first quarter, mainly due to a sharp decline in government consumption and investment activity. These dynamics can be explained by the current fiscal situation coupled with low business confidence resulting from declining order books. At the same time, the higher-than-expected 3.1ppt contribution to growth from net exports was mainly the result of a double-digit decline in imports.

We keep our GDP forecast, but there are some risks

We maintain our full-year GDP forecast for 2024 at 2.2% but do flag upside risks. Future growth will likely be driven by the continued improvement of consumption dynamics. Approaching the topic from the expenditure side, if this growth continues to be driven primarily by the services sector, it may have a smaller-than-expected impact on the economy's demand for imports. This, in turn, could result in a more favourable net export balance, even though there are currently no signs of an imminent recovery in goods exports.

Overall, we anticipate a slightly changing growth structure in the coming quarters, where domestic demand, and especially consumption, will become more prominent, while the contribution of net exports may decline compared to the current level. If, however, the improving external economic conditions in the second half of the year can provide a positive impulse for the industrial sector, we see an opportunity for a positive surprise through a resurgence in net exports. For the time being, we maintain our previous forecast of a 2.2% GDP growth for the current year, with significant upside risks.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article