Second quarter contraction in Hungary confirmed

The Statistical Office confirmed the quarterly decline in real GDP in 2Q24, with agriculture and industry the main drags. The economy is still healing, but a full recovery won’t happen without an improvement in business and consumer confidence

| -0.2% |

GDP growth in 2Q (QoQ, swda)ING forecast -0.2% / Previous 0.7% |

Economic momentum lost again

The Hungarian Central Statistical Office (HCSO) did not make any significant changes to the preliminary 2Q GDP data. On a quarterly basis, the Hungarian economy contracted by 0.2% in the April-June period. At the same time, the seasonally and calendar-adjusted year-on-year index remained at 1.3%, as indicated in the first release. The data thus confirmed that the Hungarian economy has continued to zigzag, alternating between stagnation and growth in recent quarters. We first analyse the quarterly growth situation, which we consider to be the most important as it provides a more accurate picture of the current state of the economy, which is hardly reassuring.

Services stagnate, industry falls sharply

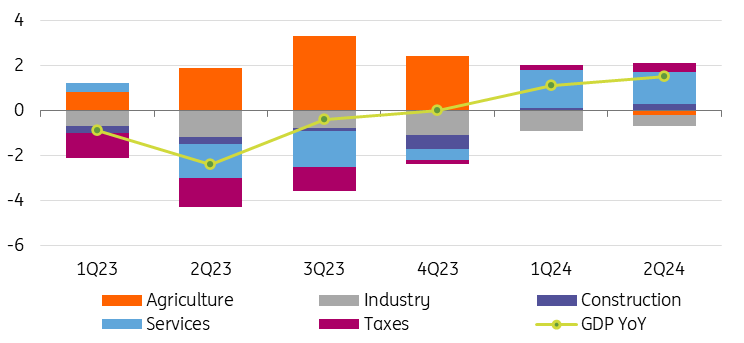

On the production side, as expected, the main drag on economic activity came from agriculture, which contracted by 5% on a quarterly basis. The performance of industry is also unsurprising given the weak high-frequency production data, with a decline of 1.5% according to the HCSO.

In contrast, the construction sector was a significant source of growth in the second quarter. However, it is more likely that a single major project completion had a significant impact here rather than a general recovery across all construction subsegments. Finally, the reason for the renewed decline in the overall performance of the Hungarian economy is the services sector. The volume of value added in services remained unchanged on a quarterly basis. In other words, the dynamic growth of the first quarter did not continue. In any case, looking at the individual sub-sectors, it is worrying that, after three quarters of dynamic growth, consumption-related activities such as trade, accommodation and food service activities have fallen back on a quarterly basis.

However, it is a positive surprise that, despite the poor performance of industry, the transportation and storage sector managed to expand slightly. Financial and insurance activities were the fastest-growing sectors. This was probably due to the exceptional home insurance policy campaign, which may have carried over (statistically) into the second quarter, and led to a significant recovery. On the other hand, there was a significant decline in professional, scientific and technical activities, which mainly cover areas that support business activities (e.g. legal and accounting services, advertising, market research, research and development, etc.). It therefore appears that companies are trying to compensate for rising labour costs (and possible labour hoarding) and a weak revenue base by cutting back on some complementary business services.

Contributions to GDP growth - production side (% YoY)

Overall, therefore, the combination of rising real wages and purchasing power, and the stalling of improving consumer and business confidence, has brought stagnation to services, which had previously been buoyant for two quarters. It is also interesting to note that, at the same time, the share of household expenditure on services fell significantly in the second quarter compared with the previous quarter. However, the share of demand for non-durable and semi-durable goods increased. This may be explained by the last big shopping spree before the end of the mandatory in-store sales and the phasing out of price caps.

Meanwhile, the share of household expenditure on durable goods was only 6.4% in the second quarter of 2024. The last time a lower share was recorded in the second quarter was in 2017. Meanwhile, it is also important to note that it is durable goods that have the highest import share, meaning that low demand in this segment partly explains the subdued import performance.

In terms of year-on-year growth indicators, agriculture showed a substantial decline in the second quarter, compared to last year's extremely high base. Industry, including manufacturing, declined by almost 4%, while construction made a positive contribution to the year-on-year GDP index, due to last year's low base. Services showed a substantial increase on a yearly basis, and both business and personal services show a positive change from a one-year perspective.

In the former, information, communication and education were the main drivers. The significant increase in education services is likely to be driven by wage settlements in the sector. Meanwhile, the value added of accommodation and food service activities may have increased significantly in the context of private consumption. The year-on-year index for retail trade also returned to positive territory, but this was mainly due to the low base.

Consumption provides some silver lining, but investment is in free fall

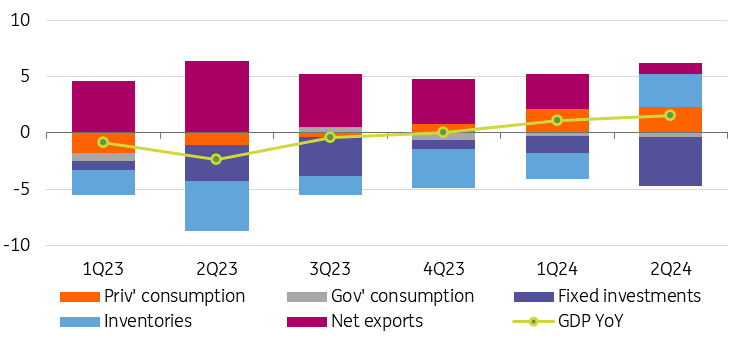

On the expenditure side, it is therefore not at all surprising that actual household consumption grew by 1.1% on a quarterly basis. At first glance, this would seem to be a reason for optimism, but in light of the above developments, it is more a case of demand picking up in one segment from quarter to quarter, driven by some kind of impulse rather than an all-around recovery.

Government consumption contracted in the second quarter, as previously expected, due to the tightly controlled fiscal budget. The continued slump in investment (6.7% quarter-on-quarter drop) has noticeably dampened economic performance in the second quarter, but this should hardly come as a surprise in light of the detailed investment report released earlier by HCSO. Business confidence and sustained growth in demand are lacking. In its absence, we can hardly expect a turnaround in the near future.

The volume of inventories has risen slightly on a quarterly basis, which would explain the expansion in the logistics sector despite weak industrial performance and the lacklustre consumption of durable goods. Exports and imports also rose marginally on a quarterly basis. The latter is mainly driven by imports of services - in conjunction with a pick-up in Hungarian outbound travel. Meanwhile, after four quarters, merchandise exports expanded again, albeit marginally.

Contributions to GDP growth - expenditure side (% YoY)

Again, turning to the year-on-year indicators on the expenditure side, domestic demand grew by only 0.7% in the second quarter. This is mainly due to a sharp decline in government consumption and investment activity, in line with the fiscal situation and low business confidence caused by falling order books. The contribution of net exports to growth of 1.0ppt was broadly in line with expectations, but it remains rather favourable for the wrong reasons: weak domestic demand is restraining the country's import demand, while exports are also weak, just not as much.

We maintain our full-year GDP forecast for 2024 at 1.5%

Looking ahead, the main hope is that consumption momentum will continue to improve. However, this would require a more sustained and stronger recovery in consumer confidence, which is unlikely to be helped by inflation creeping above 5% by the end of the year. In the services sector, the new housing programme (Home Renovation Program) could provide some stimulus to the finance and insurance sectors and, later, to construction. And new fiscal adjustment measures could boost demand for business services (mainly through increased use of legal and tax advisory services).

The turnaround in investment may still be some way off (based on lack of demand and fragile business confidence) so we do not expect a major rebound in imports, which means that net exports could continue to make a positive contribution to growth. Meanwhile, the severe drought and the hot summer will take a big toll on agriculture, dampening not only this year's agricultural performance but also the potential of food exports. Overall, in light of today's detailed data, we maintain our previous forecast of 1.5% GDP growth this year. Hardly a sudden recovery but at least a sign that the economy is in the process of healing.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article