Russia: Near-zero current account calls for caution on RUB

The Russian current account surplus of US$0.6bn in 2Q20 underperformed our expectations of US$8bn, mainly due to services imports. OPEC+ commitments, potential recovery in imports of goods and delayed dividends may keep the current account near zero in 2H20 despite the improved oil price environment

| $0.6bn |

Russian current account surplus for 2Q20$22.3bn for 1H20 |

| Worse than expected | |

2Q20 current account underperforms on above expected imports of services

The Russian current account was preliminarily estimated at US$0.6bn in 2Q20, much lower than the US$7.1bn surplus reported for April-May (suggesting either a highly negative number for June or a downward revision of the entire monthly set) and our US$8.0bn expectations.

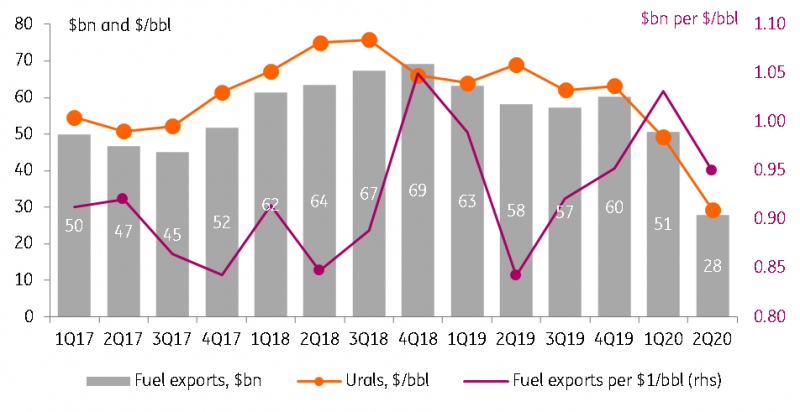

- The largely expected drop of fuel exports to US$28bn in 2Q20 from US$51bn in 1Q20 was the primary reason for the contraction in the overall current account. Interestingly, however, this drop almost fully reflects the US$20/bbl drop in average quarterly Urals to US$29/bbl in 2Q20, meaning that Russia does not seem to have suffered materially from the OPEC+ agreement, which mandated a 17-18% cut in production since May. Russia's quarterly fuel exports per US$1/bbl Urals declined by 8% from US$1.03bn to US$0.95bn in 2Q20 (Figure 1), which is a historical high for 2Q and is higher than the 2Q19 level, when the export volumes took a hit from the Druzhba pipeline. The recent extension of the OPEC+ agreement suggests that Russia's fuel exports in 3Q20 may still come under pressure despite the apparent recovery in the oil prices in the US$40-50/bbl range.

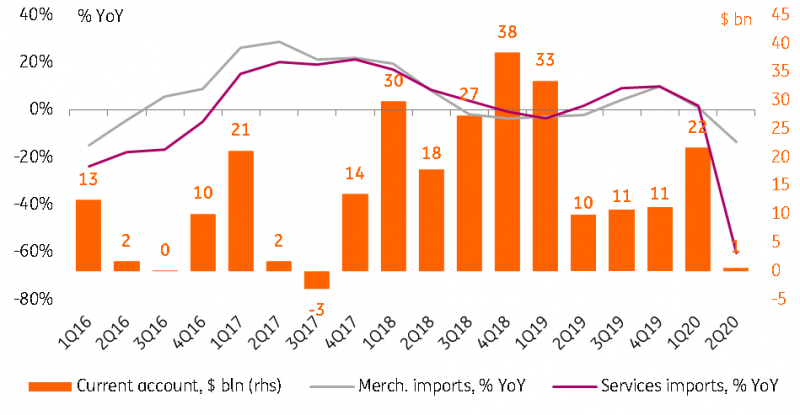

- Surprisingly, the primary source of deviation from our expectation was imports of services. While the transport services and foreign travel indeed shrank to a mininiscule US$1.7bn in 2Q20 (vs. US$13.4bn in 2Q19), imports of other, less transparent services remained significant at US$8.1bn (vs. US$11.4bn in 2Q19). As a result, imports of services dropped only 60% YoY despite the widespread ban on international travel throughout 2Q20 (Figure 2). Currently, foreign travel outside Russia remains unavailable in most directions, but the government is considering reopening flights to 15 countries soon, however 1) it remains unclear whether the destination countries are ready to reciprocate and 2) the list of 15 countries seems to focus on primarily business travel and does not include popular and more affordable tourist destinations such as Egypt, Turkey or Greece. This suggests that while the overall contraction of imports of services should moderate, it is likely to remain in the 40-50% range in 2H20.

- Merchandise imports dropped 14% year-on-year in 2Q20 after 1% YoY growth in 1Q20 (Figure 2), in line with our expectations and with what was guided by the non-CIS import dynamics for April-May. In 2Q20, a deeper drop in imports was prevented by the increased deliveries of pharmaceuticals, textiles, and aircraft, all of which appears temporary, however the gradual recovery in consumption allows us to expect a more modest 5-10% contraction in imports of goods in 2H20.

- Net investment and secondary income ouflow (driven mainly by dividend flows) shrank to US$12bn in 2Q20 from US$20bn in 2Q19, in line with expectations. Unsurprisingly, the pandemic has altered the corporate AGM and BoD plans. Moreover, Bank of Russia recomended postponing the 2019 dividend decisions of banks and financial companies from 2Q20 till 2H20 and asked them to consider recapitalisation instead of payouts. The two largest Russian banks with expected dividends of around US$7.5bn (out of which around US$3.0-3.5bn could be attributable to non-residents) have indeed postponed the decision to a later date this year. Meanwhile, the dividend flows create uncertainty for the 2H20 current account. On the one hand, the deterioration in the economic conditions may cause some corporates to cancel or reduce the dividend payout (potentially in the sectors most hit by Covid-19 and lockdown), however, so far none of the largest dividend payers in Russia's oil&gas, banking, and metals has guided for cancellation of annual dividends for the successful FY19. As a result, 2H20 may see a catch-up on the dividend payout, exceeding the 2H19 level of US$33bn, and putting delayed pressure on the current account in 2H20.

Overall, looking into 2H20, we expect the current account balance to remain close to zero, as the positive effect of improvement in the oil price environment and persisting travel restrictions will be offset by a recovery in merchandise imports, and catching up on the dividend outflow in favour of non-resident shareholders.

Figure 1: Fuel exports dropped in 2Q20 in line with oil price, Russia has yet to see the effect of output contraction

Figure 2: Imports of services dropped by only 60% YoY in 2Q20 despite travel ban, imports of goods dropped modestly

FX interventions compensate for lost fuel revenues but unable to boost private confidence

Looking at other components of the balance of payments, it appears that the contraction in the current account surplus has been compensated by the CBR FX interventions, however the capital account showed weakness both on the private and the government side.

- To a large extent, the negative effect of contraction in the current account has been offset by the FX sales, which according to the daily CBR data totaled US$10.7bn in 2Q20 (the overall decline in reserve assets as per quarterly BoP data was US$12.9bn). As we discussed earlier, the cut in the oil production has de-facto temporarily increased the intervention cut-off Urals price from US$42.4/bbl to around US$50/bbl, meaning that the fiscal rule will likely dictate continued FX sales of around US$3bn per quarter if Urals stabilises around US$45/bbl. Meanwhile, the uncertainty regarding market FX sales remains high. First, the CBR's sales in March-April exceeded the Minfin's guidance by US$2.9bn and so far have not been unwound. Second, the sales obligations as per the Sberbank handover minus the earlier mentioned front-run sales total US$23-24bn, nearly matching the US$22bn FX purchase backlog retained since August-December 2018. This suggests that the actual CBR's involvement on the FX market remains at its own discretion, however, we assume that given the free-floating FX regime the regulator will be looking to minimize its presence.

- Net private capital outflow of US$12.1bn in 2Q20 turned out smaller than the US$16.8bn seen in 1Q20, but still the figure differs materially from the US$0.7bn net inflow seen in 2Q19 and may suggest decline in local confidence. Looking at the structure of the capital outflow, around 60% of it in 2Q20 was attributable to banks (mainly reduction in foreign liabilities), while the rest is other sectors (driven by accumulation of foreign assets). In this regard, the structure does not differ materially from 1Q20 and suggests that the Russia's attractiveness to local capital at least did not increase, remaining a risk factor for 2H20 despite a relatively light foreign debt redemption schedule (gross redemptions are US$35bn vs. US$60 in 2H19).

- Portfolio investments into the state debt were modest in 2Q20. Based on the monthly and daily data, net non-resident inflows into OFZ increased from US$1.3bn in 1Q20 to US$2.1bn in 2Q20, including zero inflow in June. This is significantly below the US$4bn average quarterly inflow seen in 2019 and suggests that following some recovery from the US$3.7bn panic sell-off in March, the portfolio investors are in search of new drivers. Unless there are signs of reduction of the foreign policy risks, of material downside to the Russian key rate (currently the market is expecting up to a 50bp cut from the current 4.5% level), and of new drivers for EM risk-on, the portfolio inflows into Russia are unlikely to repeat the 2019 success story.

Figure 3: USDRUB to depend more on private and portfolio capital flows, as well as CBR's FX policy

Cautious view on RUB maintained

The 2Q20 balance of payments points that the quarterly current account in 3Q20 and 4Q20 is likely to stay around zero, as the positive effect of oil price recovery may be offset by imports and delayed dividend payout. This leaves the FX market open to uncertainties related to other components of the balance of payments, such as 1) the CBR's FX sales, which tend to decline as per fiscal rule but to some extent remain at the CBR's discretion; 2) private capital outflow, which remains strong; and 3) portfolio inflows into the local state debt, which so far has been sluggish.

Based on that, we continue to expect USDRUB to trade in the 70-75 range, with a year-end target of 72.0 even in case of improvement in the global risk sentiment and recovery in the oil price.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article