Russia: Commitment to macro stability tested by weaker activity

- 27 January 2019

- Russia

Both consumer and producer activity weakened in December 2018, confirming our expectations of declining support of local demand to GDP growth at least at the beginning of 2019. This year will be a test to Russia's conservative approach to fiscal and monetary policy

| +2.3% YoY |

December retail trade2.6% YoY in 2018 |

| Worse than expected | |

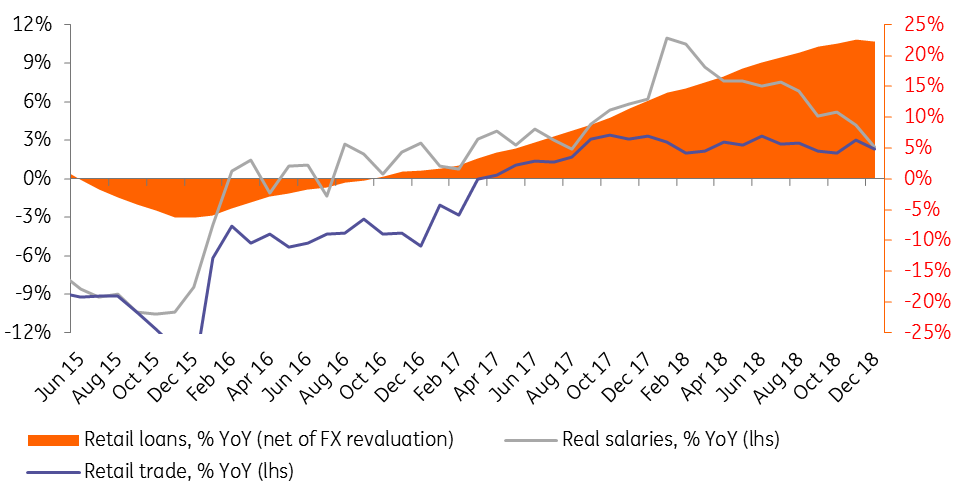

Consumption no longer supported by income or leverage

With the exception of the unemployment rate, which remained at a low level of 4.8%, the household activity data for December 2018 was a disappointment. While we expected a pre-VAT hike spending splurge to keep the retail trade figures close to 3.0% YoY, the actual result was only 2.3% YoY, putting the full-year result at 2.6%. Admittedly, this number may underestimate the consumption volumes due to the growing share of cross-border internet trade (eg, AliExpress), which may not be fully accounted for in the flash statistics, however, we are more concerned with other indicators of deterioration of the income and consumption trend coming from various sources:

- The real salary growth decelerated to 2.5% YoY in December 2018 (vs 4.4% YoY consensus) from 4.2% YoY in November, which is a result of both acceleration in the CPI growth from 3.8% to 4.3% YoY and the slowdown in nominal salary growth to 6.9% YoY from 8-10% YoY in the previous months.

- Weaker income trend is confirmed by the slowdown in retail deposit growth (adjusted for FX revaluation effect) to a mere 5.5% in December 2018 vs 6-8% YoY in the previous months, as reported by the Bank of Russia (CBR).

- The retail lending growth, also reported by CBR, slowed down (for the first time in 3 years) to 22% YoY in December 2018, which might indicate declining confidence in the higher-income households.

- Consumer confidence indicator reported by inFOM pollster dropped to 89 points in December from the 91-93 range seen throughout most of 2H18 and 106 at the beginning of last year.

We expect consumption trend to further deteriorate in 2019 for the following reasons:

- VAT has been increased from 18% to 20%, excise on a number of products, including gasoline, have also been increased, and the ability of retailers to sacrifice margins in favour of consumers is under question.

- The amount of duty-free imports for individual consumption has been halved to EUR500 per month, making bargain non-food purchases from cross-border e-shops (eg, AliExpress) more expensive.

- Real salary growth is unlikely to repeat this year's good result of 6.8% YoY in real terms due to the end of the electoral cycle and the likely acceleration of the average inflation of 2.9% in 2018 to 5%+ in 2019F.

- The increase in the retirement age effective this year should boost Russia's officially employed population by 2 million people (+3%), but as according to official statistics around 9 million Russians above the current retirement age had remained employed, the effect on total household income (official and unofficial) should not be large.

- The support to consumption from retail lending growth should decline due to CBR's further tightening in risk requirements starting 1 April.

Key indicators of the Russian consumer trend

| +2.0% YoY |

December industrial output+2.9% in 2019 |

| Worse than expected | |

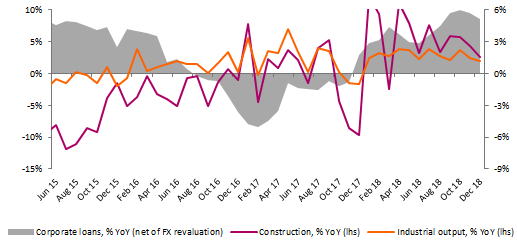

State investments fail to translate into broad-based corporate activity

Corporate activity also disappointed in December.

- Industrial output showed surprising deceleration to 2.0% YoY in December, down from 2.4% YoY in November and below the 2.5% YoY consensus. As we had predicted, industrial production managed to receive support from commodity extraction and energy distribution sectors, however, this was offset by stagnation in the manufacturing sector.

- Construction growth, which is an indirect indicator of investment activity (which is now reported only on a quarterly basis), was reported at 2.6% YoY in December, down from 4.3% YoY in the previous month and below 3.3% YoY consensus forecast.

- We note that the State Statistics Service (Rosstat) has significantly upgraded the previous 2018 dataset for construction, resulting in +5.3% growth in 2018 vs just 0.5% YoY reported earlier for 11M18. Given the 5.5% share of the construction sector in the Russian GDP, such an upgrade may statistically add up to 0.3 pp to the 2018 GDP growth, likely resulting in outperformance of our 1.6% forecast for 2018. However, the upgrade seems to reflect the completion of large state-sponsored infrastructure projects at the beginning of last year, which does not improve the 2019 expectations, if not worsening it due to the higher base effect.

- The weakening of corporate activity at the year-end is also confirmed by the slowdown in corporate lending growth (adjusted for FX revaluation effect) to 5.1% YoY in December from ~6% in the preceding months.

Overall modest performance of industrial and construction at the year-end, as well as weak corporate lending growth, suggest that large investment projects in 2018, including construction of infrastructure for the Football World Cup 2018, construction of the Kerch Bridge and Power of Siberia pipeline fail to translate in a broader-based recovery. For 2019, we expect producer activity to remain restrained by higher taxation in the oil and non-oil industry, extension of the OPEC+ agreement prescribing further cuts in oil production, worsening in the global growth outlook, persistent sanction risks and tightening in the monetary policy.

Key indicators of the Russian producer trend

GDP growth to decelerate to 1.0% in 2019F, testing Russia's commitment to conservative fiscal and monetary policy

Disappointing activity data makes us more comfortable with our below-consensus expectations of just 1.0% GDP growth for 2019F, implying just a 1.0% increase in private consumption and 1.5% increase in investments and industrial output. With economic data likely posting deceleration vs official expectations and declining popular support, the key focus of 2019 will be the economic policy response. We expect the choice to be between putting forward structural supply-side measures and to ease the approach to fiscal and/or monetary policy. The former is more difficult and time-consuming to implement but would be more likely to have a long-term positive effect on local activity and investor sentiment. The latter may provide a short-term bump to local demand at the expense of macro stability achieved of the past years.

Russian budget policy may ease in 2019 https://think.ing.com/articles/russian-budget-policy-may-ease-in-2019/

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more